Business overdraft interest rates

Business overdraft interest rates in 2026 start from around 14.55% to 25.00% p.a. according to Money’s lender database. Some banks advertise lower rates than these, but these rates tend to only be available for established businesses with a near-perfect credit history, with lower credit limits available.

To give you an idea of the current rates on unsecured business overdrafts, we have rounded up the offers from a selection of prominent lenders.

Lender | AMP |

|---|---|

Business overdraft rates from | 15.45% p.a. |

Overdraft limits | $2,000 - 50,000 |

Fees | Establishment fee $200 or 1% of limit (whichever is greater), plus 1.00% p.a. service fee (charged monthly) |

Lender | ANZ Go Biz |

Business overdraft rates from | 15.70% p.a. |

Overdraft limits | $2,000 - $200,000 |

Fees | Yearly fee ranging from $250 - 1.7% of limit depending on limit |

Lender | Australian Mutual Bank |

Business overdraft rates from | 14.51% p.a. |

Overdraft limits | From $500 |

Fees | $100 annual fee |

Lender | Beyond Bank |

Business overdraft rates from | 12.99% p.a. |

Overdraft limits | From $10,000 |

Fees | $295 approval/variation fee (no monthly fee) |

Lender | CommBank |

Business overdraft rates from | 14.30% p.a. |

Overdraft limits | Up to $250,000 |

Fees | Establishment fee quoted on approval, plus 1.70% p.a. line fee |

Lender | Community First Bank |

Business overdraft rates from | 14.45% p.a. |

Overdraft limits | Up to $15,000 |

Fees | $750 application fee, plus $10 monthly fee |

Lender | Dynamoney |

Business overdraft rates from | 14.55% p.a. |

Overdraft limits | $5,000 - $500,000 |

Fees | 1.5% annual service fee |

Lender | Great Southern Bank |

Business overdraft rates from | 11.20% - 21.20% p.a |

Overdraft limits | $10,000 - $50,000 |

Fees | $495 establishment fee, plus $30 monthly overdraft fee ($360 p.a.) |

Lender | NAB |

Business overdraft rates from | 15.75% p.a. |

Overdraft limits | $5,000 - $50,000 |

Fees | 1.75% p.a. service fee (charged monthly) |

Lender | Shift |

Business overdraft rates from | 14.95% - 24.95% |

Overdraft limits | $25,000 - $1 million |

Fees | $495 - $795 annual fee |

Lender | Suncorp |

Business overdraft rates from | 15.24% p.a. |

Overdraft limits | Up to $50,000 |

Fees | $250 establishment fee, plus $75 quarterly service fee ($300 p.a.) |

Lender | Westpac |

Business overdraft rates from | 13.21% p.a. |

Overdraft limits | $5,000 - $250,000 |

Fees | $250 establishment fee, plus 1.50% p.a. service fee (charged monthly) |

| Lender | Business overdraft rates from | Overdraft limits | Fees |

|---|---|---|---|

AMP | 15.45% p.a. | $2,000 - 50,000 | Establishment fee $200 or 1% of limit (whichever is greater), plus 1.00% p.a. service fee (charged monthly) |

ANZ Go Biz | 15.70% p.a. | $2,000 - $200,000 | Yearly fee ranging from $250 - 1.7% of limit depending on limit |

Australian Mutual Bank | 14.51% p.a. | From $500 | $100 annual fee |

Beyond Bank | 12.99% p.a. | From $10,000 | $295 approval/variation fee (no monthly fee) |

CommBank | 14.30% p.a. | Up to $250,000 | Establishment fee quoted on approval, plus 1.70% p.a. line fee |

Community First Bank | 14.45% p.a. | Up to $15,000 | $750 application fee, plus $10 monthly fee |

Dynamoney | 14.55% p.a. | $5,000 - $500,000 | 1.5% annual service fee |

Great Southern Bank | 11.20% - 21.20% p.a | $10,000 - $50,000 | $495 establishment fee, plus $30 monthly overdraft fee ($360 p.a.) |

NAB | 15.75% p.a. | $5,000 - $50,000 | 1.75% p.a. service fee (charged monthly) |

Shift | 14.95% - 24.95% | $25,000 - $1 million | $495 - $795 annual fee |

Suncorp | 15.24% p.a. | Up to $50,000 | $250 establishment fee, plus $75 quarterly service fee ($300 p.a.) |

Westpac | 13.21% p.a. | $5,000 - $250,000 | $250 establishment fee, plus 1.50% p.a. service fee (charged monthly) |

Why businesses use an overdraft

Seasonal cashflow

For industries that experience seasonality or cyclical business, unsecured finance helps smooth out those bumpy roads in cash flow throughout the course of a trading year.

Always-on credit

A business overdraft can become an embedded part of your business’ day-to-day cashflow, always available to cover costs and ensure operational continuity.

Rainy day buffer

While there is a cost to maintaining a business overdraft, the benefit of having funds available to draw on instantly, whatever happens, is worth it for many businesses.

Simple and cost effective

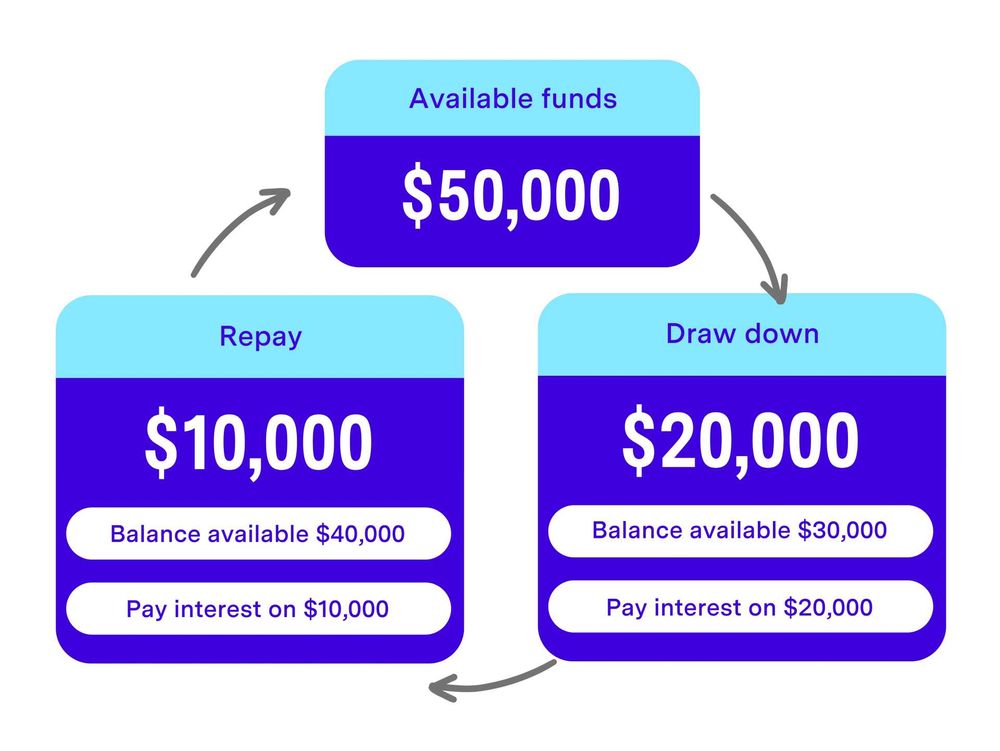

With a business overdraft you make one application and then have ongoing access to funds which you can draw on repeatedly. You only pay interest on funds you use.

Using an overdraft for ongoing growth

Phil Collard, Money.com.au Business Finance Broker

"Let’s say we have a business owner planning on going on a six-month growth journey, with marketing, new staff and expanding to another location. An overdraft could be a great option, because you've got the flexibility to take out what you need when you need it. You could set up a $150,000 overdraft today, but only draw down some of the funds up-front, then another tranche in a month's time, and so forth. There's no point in that customer paying interest on that whole $150K when they don't need all of it upfront. With an overdraft, there’s also no need to reapply for finance when the next injection of capital is required."

Phil Collard, Money.com.au Business Finance Broker

Business overdraft versus term loan: Which will be best?

Compared to an unsecured business loan, a business overdraft offers more flexibility and longevity. The finance available is constantly refreshing. Instead of needing to reapply for funds every time, you can dip in and out. By contrast, term loans are often there to fix a one-off problem, or capitalise on a one-off opportunity.

If your business has a high turnover and needs fast access to funds on an irregular basis, an overdraft may be suitable as it offers quick and reliable access to funds. That could be for paying invoices, paying staff, doing fit outs or just having some extra working capital.

In our experience working with Australian businesses, industries commonly using a business overdraft include retail, wholesale, manufacturing, professional services, food and beverage, technology and automotive.

A business overdraft is generally not as well suited to long-term capital investment, like purchasing an asset. In that scenario, equipment finance, a business car loan or chattel mortgage may be a better fit.

Example: Business overdraft vs term loan

Let’s look at a hypothetical example created by our business finance team to illustrate the difference between a business overdraft and a term loan.

A plumbing business needs up to $100,000 in working capital to cover wages, fuel and materials while waiting for customer invoices to be paid. The owner is deciding between a business overdraft and a 12-month business term loan.

As the cost comparison below shows, even though the overdraft has a higher interest rate, it ends up cheaper in this scenario because the business only uses half of the available limit on average. Whereas with a term loan, the business would be charged interest on the full balance from day one.

However, if the business expected to have most of the $100,000 overdraft limit outstanding for long periods, the term loan would likely work out cheaper.

Credit limit | |

Business overdraft | $100,000 |

Business term loan | $100,000 |

Average balance used | |

Business overdraft | $50,000 |

Business term loan | $100,000 |

Interest paid | |

Business overdraft | $7,500 |

Business term loan | $11,800 |

Fees | |

Business overdraft | 1.5% p.a. service fee on limit ($1,500) |

Business term loan | $750 establishment fee |

Total cost over 12 months (interest & fees) | |

Business overdraft | $9,000 |

Business term loan | $12,550 |

| Business overdraft | Business term loan | |

|---|---|---|

Credit limit | $100,000 | $100,000 |

Average balance used | $50,000 | $100,000 |

Interest paid | $7,500 | $11,800 |

Fees | 1.5% p.a. service fee on limit ($1,500) | $750 establishment fee |

Total cost over 12 months (interest & fees) | $9,000 | $12,550 |

Interest rates on business overdrafts vs business loans

Business overdraft interest rates are typically higher than those available on unsecured business term loans. Business overdraft rates start from 14.55% p.a., compared with 12.85% for an unsecured loan, according to Money.com.au’s database of lenders. Across the market, Reserve Bank of Australia data also indicates a 1.76% gap between overdraft rates and term loans for small businesses.

7 steps to getting a low-cost business overdraft

Compare options beyond your existing bank

If you decide to get a business overdraft set up, applying with the bank you already have a transaction account with might seem like the most obvious first step. But you should compare your options first.

Like any kind of business finance, the interest rates, fees and other terms on business overdrafts can vary a lot depending which provider you go with.

Look for the lowest fees possible

With a business overdraft, expect to pay an application fee as well as a line fee, which will likely be quarterly or annually. The lender charges a line fee for keeping the overdraft facility open and it applies whether you use the overdraft or not. Line fees are either a flat amount or can be a percentage of the credit limit.

There can also be hefty fees if you draw down funds beyond your overdraft limit.

In our experience, not all lenders advertise the actual fees they charge. Instead, fees are "determined upon application" or something similarly vague. This is where we come in. We'll help you understand the business overdraft fees charged by multiple lenders, without you needing to apply first.

Shop for the lowest interest rate you qualify for

There’s a massive difference between the highest and lowest business overdraft rates. Particularly if you will have funds overdrawn on a regular basis, it’s important to look for the lowest interest rate possible (even though you’ll only be charged interest on funds withdrawn).

Your interest rate will be tailored to your business depending on factors like annual turnover and how long it’s been operating. Your personal credit rating may also be a factor.

Consider whether a secured or unsecured overdraft is best

You generally have the choice of a secured or unsecured business overdraft. A secured overdraft will be backed by an asset you or your business owns (usually residential or commercial property).

Interest rates and fees are usually lower on secured overdrafts. But if you need a quick approval, an unsecured overdraft is usually more straightforward to apply for.

Pick a suitable overdraft term

Terms on a business overdraft range from 3 months to 5 years, or some involve a ‘revolving’ business line of credit with no set term. Even if you agree to a set term with a lender, they may be able to review the overdraft facility at any time.

Importantly, if you only need help with cash flow for a short period of time or one-off project, avoid signing up for an overdraft with a long or open-ended term. You'll likely be charged overdraft fees long after the overdraft has served its purpose.

Pay attention to the repayment requirements

A traditional bank overdraft typically won't have set repayment requirements. You essentially repay it as and when funds are deposited into your account. This is obviously a very flexible option. It can also be very expensive as interest charges are added until the overdraft is cleared in full.

Most of the specialist lenders we work with set a minimum principal repayment amount on business overdraft facilities. This means there will be a limit on how much interest you will pay over time on the amount overdrawn.

Choose your overdraft limit carefully

There are two ways you could arrive at a suitable overdraft limit for your business: What the lender is willing to offer you as a maximum credit facility, or the amount you actually need.

Business overdraft fees are often charged as a percentage of your limit. In other cases, there are fee bands. A higher overdraft limit could move you into a higher fee band. Either way, a higher overdraft limit than your business needs will cost you more.

Business owner case study

Catherine Cervasio, Founder of Australian natural skincare brand Aromababy

“We took out an overdraft to fund inventory which meant we have stock available in order to take advantage of growth opportunities - especially critical for export where we wouldn't carry adequate stock levels otherwise. We decided on an overdraft (low doc, easy application) vs a loan due to ease and interest rates.”

Catherine Cervasio, Founder of Australian natural skincare brand Aromababy

How to apply for a business overdraft

You can apply for a business overdraft online with most lenders. Many borrowers prefer non-bank and specialist lenders due to the fast approval time and access to funds offered by these companies.

The difference can be as significant as approval within 24 hours with a specialist lender, versus four to six weeks with a major bank.

If you are looking for a business overdraft limit below $150,000, some lenders will only require business bank statements, plus a personal guarantee from a director, to grant approval. You could apply online and have the funds available the next day.

Secured versus unsecured business overdraft

Secured business overdraft

With a secured overdraft, an asset owned by you or your business serves as collateral for the finance. If you default on the overdraft repayments, the lender can recoup its money by making a claim on the asset. Interest rates on a secured overdraft are typically lower as there is less risk for the lender.

Unsecured business overdraft

With an unsecured overdraft, there is no specific asset serving as collateral. But it’s important to remember that even unsecured finance contracts often include clauses allowing the lender to make a claim on assets in your name in the event of a default. Interest rates on an unsecured overdraft are typically higher.

An unsecured overdraft is not dissimilar to a business credit card or charge card, but with a larger limit and potentially lower fees. For example, some overdraft facilities don't have monthly account keeping fees and there's generally no early payment fees.

What fees are there on a business overdraft?

A business overdraft typically comes with up-front and ongoing fees, including:

- Establishment or setup fee A one-off fee charged when the overdraft facility is first approved. This covers the lender’s cost for assessing and setting up the credit limit.

- Line or facility fee An ongoing fee (monthly, quarterly, or annually) charged for having the overdraft available, regardless of whether you use it. It’s usually a percentage of the approved limit (e.g. 1%–2%).

- Drawdown fees There may be a fee each time you make a withdrawal from your overdraft facility. This may be a fixed amount or a percentage of the withdrawal.

- Over-limit fee If you exceed your approved overdraft limit, you may be charged an over-limit or unauthorised overdraft fee, and a higher interest rate may apply to the excess amount.

- Account-keeping or service fees Some lenders charge a regular account maintenance fee in addition to the facility fee, to cover administration costs.

- Renewal, review or cancellation fees Lenders may charge a fee to review or renew the facility at the end of the current term (if there is a fixed term), or indeed to cancel the overdraft.