What is a bridging loan?

A bridging loan is a short-term home loan designed to help borrowers purchase a new home while they wait for their existing property to sell. The loan ‘bridges’ the finance gap between buying and selling.

“With a bridging loan, you’re basically buying a new property by borrowing against the equity in your current property to facilitate the purchase,” explains Money.com.au’s home loan expert, Michael Burgess.

Most bridging loans are only designed to be held for a maximum of 6-12 months. But even within this short period, bridging loans can be an expensive form of finance, with higher rates than standard loans typically applying.

Some lenders charge in excess of 10% p.a., Money.com.au’s analysis found.

If you get a bridging loan, the amount borrowed will be on top of your existing mortgage, so be prepared for high repayments during the bridging loan term. Most lenders offer options to minimise the repayments burden during this time (more on that to come).

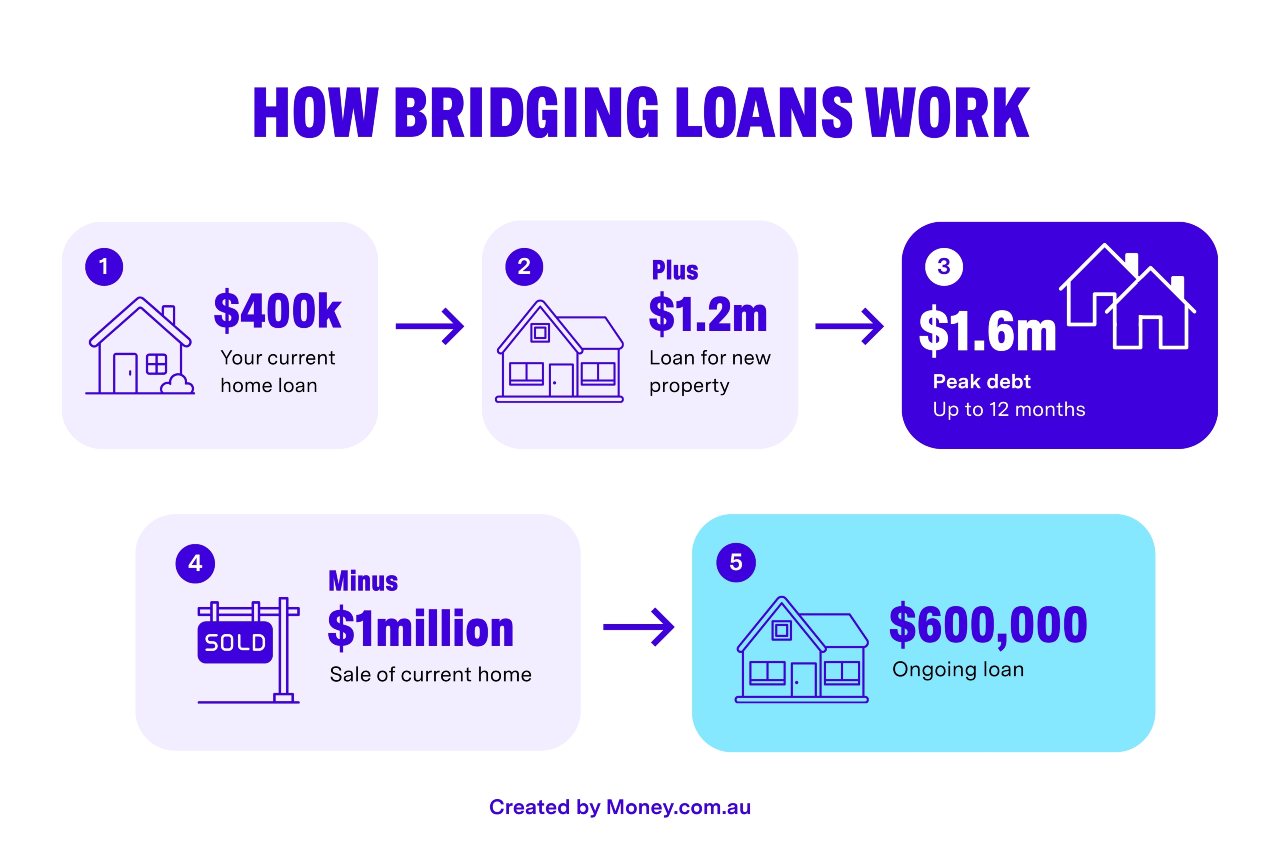

How does a bridging loan work?

Requires a full credit application

You apply for a new loan either with your current lender or a new provider to purchase a new property. This can either be a full loan application based on a property you have found, or a pre-approval application allowing you to go house hunting with a budget in mind.

You use the equity in your current property

A bridging loan typically involves releasing equity in your current home to use as security for borrowing the deposit and purchase amount for a new property.

Old loan + new loan = 'peak debt'

You will then typically be holding two loans until you sell your current home: your existing loan if you have one, plus the new bridging loan. This combination of loans is known as your ‘peak debt’.

Limited term duration

You typically have up to 6-12 months to sell your current home. If you can't sell your home during this time, you can apply for an extension, or your lender may intervene to ensure the property is sold as soon as possible.

Options to lower repayments

During the bridging loan term, you usually have the option of making interest-only repayments so your repayments are lower. Some bridging loans don’t require you to pay anything until the end of the term. Instead, you repay the full amount, plus interest (which would have been compounding during the bridging loan term) using the proceeds of the property sale.

Bridging loan repaid when your home is sold

When you sell your property, the funds are used to pay out your bridging loan. The outstanding finance becomes your ‘ongoing loan’ or ‘end debt’. Repayments usually revert to principal and interest at this stage.

A ‘closed’ bridging loan must be repaid by a specific date (e.g. you have already agreed a sale on your home and are waiting for it to settle). An ‘open’ bridging loan has a maximum term of 6-12 months but is not tied to an already-agreed settlement date.

What’s a good bridging loan interest rate?

Bridging loan interest rates currently start from around the mid 6% mark, though most lenders charge higher rates than that depending on the borrower’s profile. Bridging loan rates are generally higher than standard home loan rates.

Use our comparison service or speak with one of our mortgage brokers to find out which rates you may be eligible for.

Keep in mind that lenders usually advertise their most competitive bridging finance rates, which are often reserved for borrowers with strong equity positions and well-prepared applications. The actual rate you receive may be higher, depending on your financial circumstances and risk profile.

Best bridging loan rates right now

| Loan | Interest rate | Comparison rate^ | Max LVR |

|---|---|---|---|

| BankVic Home Buyer or Upgrade Variable Rate | 6.10% variable | 6.10% | 80% |

| Well Money Bridging Home Loan | 6.31% variable | 6.35% | 80% |

| Border Bank Bridging Home Loan | 7.09% variable | 6.33% | 80% |

| Well Money Bridging Home Loan | 7.37% variable | 7.74% | 80% |

| Police Credit Union Standard Variable Home Loan Owner Occupier 90% LVR | 7.49% variable | 7.56% | 90% |

| Loans.com.au Bridging Loan | 8.19% fixed 1 year | 6.49% | 80% |

| Loans.com.au Bridging Loan | 8.19% variable | 6.49% | 80% |

| BCU Bank Bridging Loan | 9.76% variable | 9.79% | 80% |

| Arab Bank Australia Bridging Loan | 10.65% variable | 10.72% | 80% |

Shane's smooth bridging finance experience with Money.com.au

Shane, WA

"We had an outstanding experience working with Michael Burgess at Money.com.au. From start to finish, he was professional, responsive, and genuinely invested in helping us achieve the best outcome.

Michael secured us a great mortgage and, more importantly, put together a clear and well thought out plan for transitioning into our next home. We were navigating a bridging loan, and he made the entire process feel smooth and straightforward.

Nothing was ever too much trouble, and he explained everything in a way that gave us real confidence at every step. It honestly could not have been easier.

Highly recommend Michael to anyone looking for expert guidance and a seamless experience."

Shane, WA

Bridging loan pros and cons

Pros

- Convenient short-term option if you find a property to buy before you have sold your current one

- Can save you money by meaning you don’t need to rent a property or pay storage fees while you find a new home (after selling your existing one)

- Flexible options to keep repayments manageable while you have a high ‘peak debt’ (e.g. interest-only payments)

- Maximum terms of up to 12 months with most lenders gives you a decent window of time to sell your home

- You generally have the flexibility to close out the loan quickly if you sell your home faster than expected (saving you interest)

Cons

- More expensive compared to standard home loan rates, although some lenders (e.g. ANZ and RAMS) offer the same rates as standard loans

- You will have a high level of debt during the bridging loan term, with high interest costs building up

- If you can’t sell your home within the bridging loan term, some lenders technically count this as a ‘default’ and may need to step in to ensure the property is sold

- If your existing property sells for less than expected and it's not enough to pay off the bridging loan (including interest) you will have higher ongoing debt and repayments than you may have budgeted for

Michael Burgess, Senior Mortgage Broker at Money.com.au

“Always check with your lender to make sure they're going to give you adequate time for you to sell your home. Some bridging lenders might give you a really good rate, but then say ‘we want our money back in three or six months’. Even if you have 12 months, don't wait till the nine month mark to start selling your home.”

Michael Burgess, Senior Mortgage Broker at Money.com.au

Bridging loans vs standard home loans

Purpose | |

Bridging loan | Purchase a new home secured by equity in an existing property you intend to sell within 12 months. |

Standard home loan | Purchase a new home supported with either a deposit or equity from another property. |

Maximum loan-to-value ratio (LVR) allowed | |

Bridging loan | Usually up to 85% but varies by lender. |

Standard home loan | Usually 95% with lender’s mortgage insurance. |

Interest rates | |

Bridging loan | Depends on the application and lender but generally higher than standard loans. |

Standard home loan | Lower than bridging loan rates but vary based on the LVR and other factors. |

Repayments | |

Bridging loan | Usually interest-only. Some lenders don’t even require the borrower to pay off the interest until they have sold their original property. |

Standard home loan | Option of interest-only for a set period but most borrowers pay off the principal and interest throughout the loan term. |

Availability | |

Bridging loan | Not all lenders offer bridging loans, but some niche lenders specialise in bridging loans. |

Standard home loan | Wider selection of options and rates. |

| Bridging loan | Standard home loan | |

|---|---|---|

Purpose | Purchase a new home secured by equity in an existing property you intend to sell within 12 months. | Purchase a new home supported with either a deposit or equity from another property. |

Maximum loan-to-value ratio (LVR) allowed | Usually up to 85% but varies by lender. | Usually 95% with lender’s mortgage insurance. |

Interest rates | Depends on the application and lender but generally higher than standard loans. | Lower than bridging loan rates but vary based on the LVR and other factors. |

Repayments | Usually interest-only. Some lenders don’t even require the borrower to pay off the interest until they have sold their original property. | Option of interest-only for a set period but most borrowers pay off the principal and interest throughout the loan term. |

Availability | Not all lenders offer bridging loans, but some niche lenders specialise in bridging loans. | Wider selection of options and rates. |

Eligibility requirements for a bridging loan

Here are some of the main requirements for lenders for when assessing eligibility for bridging finance:

- High level of equity in your current home.

- High likelihood that your current property will be sold during the bridging loan term (some lenders won’t lend against properties in rural areas for this reason).

- Some lenders (e.g. Commbank) only offer bridging finance to customers with an existing home loan.

- You will need to demonstrate you have capacity to at least cover interest-only payments on your peak debt (current mortgage plus bridging finance) until your current home is sold.

- Some lenders may require you to have an amount equivalent to how much interest you will be charged in cash savings when you apply.

There are some specialist private lenders with more lenient eligibility criteria and faster approvals, but there are risks to using these lenders.

Alternatives to bridging loans

Here are some potential alternatives to using bridging finance. Before deciding one way or another, ensure you have consulted with relevant experts (mortgage broker, financial advisor, solicitor) so you know what you’re signing up for.

Take out a second standard home loan

If you can afford the repayments on two loans, you could apply for a second, separate home loan to finance the purchase of your new home. You would generally then use the sale funds from your existing home to pay out your original loan and any leftover money could go towards lowering the balance of the new loan.

This is similar in theory to how a bridging loan works, but it may be more difficult to get approval and you likely won’t have the same flexibility to lower your repayments while you have two loans to repay.

Buy a property and ask for a longer settlement

Another option is to ask the seller of your new home to agree to a longer settlement period (e.g. 90 days instead of 30), giving you more time to sell your current property. This could allow you to sell your current property before the sale of the new one is finalised and money needs to change hands.

You could also ask (with the help of your solicitor) to make the contract for you to purchase your new home subject to you selling your current property.

Not all sellers will agree to this, however. Even if they do, there is still no guarantee you will be able to sell your property by the time the settlement date on the new property arrives.

Deposit bond

If you just need cash for a deposit to secure your new property (usually 10% of the value), you could consider a deposit bond. This is a product offered by some lenders and insurance companies and is a promise to the property seller that the deposit will be paid in full by the due date. You, as the buyer, pay a non-refundable fee usually ranging from 1-2% of the amount, to the issuer of the deposit bond.

If you use a deposit bond, this will only cover the initial deposit required to secure the home. You will still need to cover the remainder of the sale price when the sale settles. For this reason, deposit bonds are generally used if you have agreed a sale on your current property and are waiting on the sale funds to come through – but you have found a new property to buy in the meantime.

Wait until you’ve sold your current home

If you don’t want to take out additional finance to buy a new home, you could always wait until you have sold your current property. This means you will have a clear idea of the budget for the new property, and depending on the situation (e.g. if you are downsizing), you may not need finance at all.

While you find your new property, many borrowers keep the sale funds from the old home in a high interest savings account, or even a term deposit if you know you won’t need to access the money for a certain amount of time.

The downside is you may need to rent for a period of time after you have sold your old home and are looking for a new one. If property values are rising quickly, this strategy could also mean you end up needing to pay more than you would have had you purchased the new property first.

Expert tips on buying and selling at the same time from a buyer's agent

Michelle May, Buyers Agent

"In a downward trending market, I highly recommend selling first, ideally with a longer settlement so you have more time to look for your next home. This significantly reduces financial and emotional pressure and allows for more thoughtful purchasing. In an upward trending market, selling first is risky as you may not be able to find your next property in an adequate time frame, whilst the market continues to go up and up, so here my advice would be to buy first."

Michelle May, Buyers Agent

More tips from buyers agent, Michelle

Bridging loan tips

"Bridging loans can be a solution for this specific scenario, especially when there's confidence in a quick sale of the current property, once you have bought your new home.

"Juggling two transactions at the same time ultimately depends on what kind of properties you are working with, and what your financial situation is, so make sure to get good advice on this. The interest rate landscape of recent and the length of your pre approval are again things to seriously consider before going down this path.

"The reality of simultaneous transactions is that they can be risky. The last thing you want is to end up buying something that doesn’t suit you just because of fear of missing out underpinned by the fact that your affordability is fast diminishing due to prices rising or interest rates increasing. It's important to take a step back and not let urgency overshadow the importance of making the right choice. There is nothing worse than unpacking your belongings in your new home and realising you've made a terrible mistake.

"Finally, potentially consider moving in with family or friends or even AirBnB for the short term, rather than taking on a 6 or 12 month lease, if there are any gaps between selling and buying. "

Home loan types

Borrower types

How it works