SPECIAL OFFERS

Credit card cashback offers

By Isabella Visser

The top credit card sign-up deals in Australia right now offer up to 200,000 points or $450 in account credits. Check out the best offers and their eligibility criteria.

Top credit card offers compiled by Sean Callery and fact checked by Isabella Visser. Updated 1 Jul 2026.

Sponsored

Our Top Offer For

Rewards

American Express® Platinum Card

200,000 Bonus Membership Rewards® Points.

View Terms

Our Top Offer For

Balance Transfers

Latitude Low Rate Mastercard

0% interest for 24 months on a balance transfer.

View Terms

Our Top Offer For

Frequent Flyer

American Express® Qantas Ultimate Card

Earn 50,000 bonus Qantas Points.

View Terms

These are the top 10 credit card offers for bonus rewards points from Money.com.au's database at the time of writing.

Card | |

|---|---|

Bonus sign-up offer | 200,000 Membership Rewards® Points |

Offer conditions | To qualify, you must apply online through the link on this page by 25 August 2026, are approved and spend $5,000 on eligible purchases on your new American Express® Platinum Card within the first 3 months. T&Cs apply. New American Express Card Members only. |

Annual card fee | $1,450 |

Card | BankSA/Bank of Melbourne/St.George Amplify Rewards Signature |

Bonus sign-up offer | Up to 200,000 Amplify Points |

Offer conditions | Get 100k bonus points if you spend at least $12k on eligible purchases in the first 12 months, and another 100k bonus points if you spend at least $12k on eligible purchases in year two. |

Annual card fee | $199 in first year, then $295 |

Card | Westpac Altitude Rewards Black Credit Card |

Bonus sign-up offer | Up to 200,000 Altitude Points |

Offer conditions | Get 100k bonus points if you spend at least $12k on eligible purchases in the first 12 months, and another 100k bonus points if you spend at least $12k on eligible purchases in year two. |

Annual card fee | $200 in first year, then $295 |

Card | ANZ Rewards Black Credit Card |

Bonus sign-up offer | Up to 180,000 ANZ Reward Points, plus $100 cash back |

Offer conditions | Get 130k extra ANZ Reward Points and $100 back when you spend $5k on eligible purchases in the first 3 months, and another 50k points when you keep the card for over 15 months. |

Annual card fee | $375 |

Card | MyCard Premier - Reward Points Offer |

Bonus sign-up offer | Up to 150,000 MyCard Reward Points |

Offer conditions | Get 120k bonus MyCard Reward Points when you spend $7k on eligible purchases within 90 days from approval and another 30,000 bonus points when you keep your card open for over 12 months. |

Annual card fee | $300 |

Card | BankSA/Bank of Melbourne/St.George Amplify Qantas Signature |

Bonus sign-up offer | Up to 150,000 Qantas Points |

Offer conditions | Get 90,000 bonus points if you spend $6k or more on eligible purchases in the first 90 days, and an extra 60k points if you spend at least $6k on eligible purchases within the first 90 days of year two with the card. |

Annual card fee | $295 plus $75 Annual Qantas Rewards Program fee |

Card | Westpac Altitude Qantas/Velocity Black Credit Card |

Bonus sign-up offer | Up to 150,000 Qantas/Velocity Points |

Offer conditions | Get 90,000 bonus points if you spend $6k or more on eligible purchases in the first 90 days, and an extra 60k points if you spend at least $6k on eligible purchases within the first 90 days of year two with the card. |

Annual card fee | $295 plus $75 Annual Rewards Program fee |

Card | Qantas Money Titanium Credit Card |

Bonus sign-up offer | 150,000 Qantas Points |

Offer conditions | Spending at least $5k within 90 days from card approval. |

Annual card fee | $1,200 |

Card | NAB Qantas Rewards Signature Credit Card |

Bonus sign-up offer | Up to 130,000 Qantas Points |

Offer conditions | Receive 100,000 bonus points when you spend $5,000 on everyday purchases within the first 90 days of opening the account. Plus, an additional 30,000 bonus points when you keep your card for over 12 months. |

Annual card fee | $420 |

Card | ANZ Rewards Platinum Credit Card |

Bonus sign-up offer | 125,000 ANZ Rewards Points, plus $50 cash back |

Offer conditions | Earn 85,000 ANZ Rewards Points and $50 cash back when you spend $3,500 on eligible purchases in the first 3 months from approval. Then receive an extra 40,000 for keeping the card for over 15 months from activation. |

Annual card fee | $149 |

| Card | Bonus sign-up offer | Offer conditions | Annual card fee |

|---|---|---|---|

200,000 Membership Rewards® Points | To qualify, you must apply online through the link on this page by 25 August 2026, are approved and spend $5,000 on eligible purchases on your new American Express® Platinum Card within the first 3 months. T&Cs apply. New American Express Card Members only. | $1,450 | |

BankSA/Bank of Melbourne/St.George Amplify Rewards Signature | Up to 200,000 Amplify Points | Get 100k bonus points if you spend at least $12k on eligible purchases in the first 12 months, and another 100k bonus points if you spend at least $12k on eligible purchases in year two. | $199 in first year, then $295 |

Westpac Altitude Rewards Black Credit Card | Up to 200,000 Altitude Points | Get 100k bonus points if you spend at least $12k on eligible purchases in the first 12 months, and another 100k bonus points if you spend at least $12k on eligible purchases in year two. | $200 in first year, then $295 |

ANZ Rewards Black Credit Card | Up to 180,000 ANZ Reward Points, plus $100 cash back | Get 130k extra ANZ Reward Points and $100 back when you spend $5k on eligible purchases in the first 3 months, and another 50k points when you keep the card for over 15 months. | $375 |

MyCard Premier - Reward Points Offer | Up to 150,000 MyCard Reward Points | Get 120k bonus MyCard Reward Points when you spend $7k on eligible purchases within 90 days from approval and another 30,000 bonus points when you keep your card open for over 12 months. | $300 |

BankSA/Bank of Melbourne/St.George Amplify Qantas Signature | Up to 150,000 Qantas Points | Get 90,000 bonus points if you spend $6k or more on eligible purchases in the first 90 days, and an extra 60k points if you spend at least $6k on eligible purchases within the first 90 days of year two with the card. | $295 plus $75 Annual Qantas Rewards Program fee |

Westpac Altitude Qantas/Velocity Black Credit Card | Up to 150,000 Qantas/Velocity Points | Get 90,000 bonus points if you spend $6k or more on eligible purchases in the first 90 days, and an extra 60k points if you spend at least $6k on eligible purchases within the first 90 days of year two with the card. | $295 plus $75 Annual Rewards Program fee |

Qantas Money Titanium Credit Card | 150,000 Qantas Points | Spending at least $5k within 90 days from card approval. | $1,200 |

NAB Qantas Rewards Signature Credit Card | Up to 130,000 Qantas Points | Receive 100,000 bonus points when you spend $5,000 on everyday purchases within the first 90 days of opening the account. Plus, an additional 30,000 bonus points when you keep your card for over 12 months. | $420 |

ANZ Rewards Platinum Credit Card | 125,000 ANZ Rewards Points, plus $50 cash back | Earn 85,000 ANZ Rewards Points and $50 cash back when you spend $3,500 on eligible purchases in the first 3 months from approval. Then receive an extra 40,000 for keeping the card for over 15 months from activation. | $149 |

These are the top 10 credit card cashback offers Money.com.au's database at the time of writing.

Card | BankSA/Bank of Melbourne/St.George Vertigo Card |

|---|---|

Bonus sign-up offer | Up to $450 cashback |

Offer conditions | Get $75 cashback for each month you spend $1k or more on eligible purchases in the first 6 months from card approval. |

Annual card fee | $0 in first year, then $84 (charged as $7 per month) |

Card | ANZ Platinum credit card |

Bonus sign-up offer | $450 cashback |

Offer conditions | Earn $450 back to your new card when you spend $4,500 on eligible purchases in the first four months. |

Annual card fee | $0 in first year, then $87 |

Card | Westpac Low Rate Credit Card - Cashback Offer |

Bonus sign-up offer | Up to $450 cashback |

Offer conditions | Get $75 cashback for each month you spend $1k or more on eligible purchases in the first six months with the card. |

Annual card fee | $0 in first year, then $84 (charged as $7 per month) |

Card | Commbank Low Rate Credit Card |

Bonus sign-up offer | Up to $420 cashback |

Offer conditions | Earn $75 each month when you spend $500 or more per month for the first 12 months. |

Annual card fee | $72 (charged as $6 per month) |

Card | ANZ Low Rate credit card |

Bonus sign-up offer | $400 cashback |

Offer conditions | When you spend $5k on eligible purchases in the first six months. |

Annual card fee | $58 |

Card | NAB Low Rate Credit Card |

Bonus sign-up offer | $400 cashback |

Offer conditions | When you spend $5,000 on purchases within 150 days from account opening. |

Annual card fee | $99 |

Card | NAB Low Fee Credit Card |

Bonus sign-up offer | $250 cashback |

Offer conditions | When you spend $1,500 on purchases within 90 days from account opening. |

Annual card fee | $49 |

Card | CommBank Low Fee Credit Card |

Bonus sign-up offer | Up to $240 cashback |

Offer conditions | Earn $40 each month when you spend $500 or more per month for the first six months, |

Annual card fee | $36 (charged as $3 per month but waived if you spend at least $300 per month) |

Card | ANZ First Credit Card |

Bonus sign-up offer | $220 cashback |

Offer conditions | When you spend $1,500 on eligible purchases in the first 3 months. |

Annual card fee | $30 |

Card | ANZ Frequent Flyer Black Credit Card |

Bonus sign-up offer | $200 cashback (plus 90,000 bonus Qantas Points) |

Offer conditions | When you spend $5k on eligible purchases in the first three. months from approval. |

Annual card fee | $425 |

| Card | Bonus sign-up offer | Offer conditions | Annual card fee |

|---|---|---|---|

BankSA/Bank of Melbourne/St.George Vertigo Card | Up to $450 cashback | Get $75 cashback for each month you spend $1k or more on eligible purchases in the first 6 months from card approval. | $0 in first year, then $84 (charged as $7 per month) |

ANZ Platinum credit card | $450 cashback | Earn $450 back to your new card when you spend $4,500 on eligible purchases in the first four months. | $0 in first year, then $87 |

Westpac Low Rate Credit Card - Cashback Offer | Up to $450 cashback | Get $75 cashback for each month you spend $1k or more on eligible purchases in the first six months with the card. | $0 in first year, then $84 (charged as $7 per month) |

Commbank Low Rate Credit Card | Up to $420 cashback | Earn $75 each month when you spend $500 or more per month for the first 12 months. | $72 (charged as $6 per month) |

ANZ Low Rate credit card | $400 cashback | When you spend $5k on eligible purchases in the first six months. | $58 |

NAB Low Rate Credit Card | $400 cashback | When you spend $5,000 on purchases within 150 days from account opening. | $99 |

NAB Low Fee Credit Card | $250 cashback | When you spend $1,500 on purchases within 90 days from account opening. | $49 |

CommBank Low Fee Credit Card | Up to $240 cashback | Earn $40 each month when you spend $500 or more per month for the first six months, | $36 (charged as $3 per month but waived if you spend at least $300 per month) |

ANZ First Credit Card | $220 cashback | When you spend $1,500 on eligible purchases in the first 3 months. | $30 |

ANZ Frequent Flyer Black Credit Card | $200 cashback (plus 90,000 bonus Qantas Points) | When you spend $5k on eligible purchases in the first three. months from approval. | $425 |

These are the top 10 credit card offers based on the greatest discount to the annual fee during the first year (i.e. greatest $ difference between annual fee in year one versus the standard card fee).

Card | HSBC Star Alliance Credit Card |

|---|---|

First-year annual card fee | $0 |

Standard annual card fee | $499 |

First-year saving | $499 |

Card | HSBC Premier World Mastercard - Qantas Rewards |

First-year annual card fee | $0 |

Standard annual card fee | $399 |

First-year saving | $399 |

Card | HSBC Platinum Qantas Credit Card |

First-year annual card fee | $0 |

Standard annual card fee | $399 |

First-year saving | $399 |

Card | David Jones Prestige Credit Card |

First-year annual card fee | $0 |

Standard annual card fee | $295 |

First-year saving | $295 |

Card | HSBC Premier World Mastercard |

First-year annual card fee | $0 |

Standard annual card fee | $199 |

First-year saving | $199 |

Card | HSBC Platinum Credit Card |

First-year annual card fee | $0 |

Standard annual card fee | $199 |

First-year saving | $199 |

Card | American Express Platinum Edge Credit Card |

First-year annual card fee | $0 |

Standard annual card fee | $195 |

First-year saving | $195 |

Card | NAB Qantas Rewards Signature Credit Card |

First-year annual card fee | $320 |

Standard annual card fee | $420 |

First-year saving | $100 |

Card | NAB Qantas Rewards Premium Credit Card |

First-year annual card fee | $195 |

Standard annual card fee | $295 |

First-year saving | $100 |

Card | David Jones Premiere Credit Card |

First-year annual card fee | $0 |

Standard annual card fee | $99 |

First-year saving | $99 |

| Card | First-year annual card fee | Standard annual card fee | First-year saving |

|---|---|---|---|

HSBC Star Alliance Credit Card | $0 | $499 | $499 |

HSBC Premier World Mastercard - Qantas Rewards | $0 | $399 | $399 |

HSBC Platinum Qantas Credit Card | $0 | $399 | $399 |

David Jones Prestige Credit Card | $0 | $295 | $295 |

HSBC Premier World Mastercard | $0 | $199 | $199 |

HSBC Platinum Credit Card | $0 | $199 | $199 |

American Express Platinum Edge Credit Card | $0 | $195 | $195 |

NAB Qantas Rewards Signature Credit Card | $320 | $420 | $100 |

NAB Qantas Rewards Premium Credit Card | $195 | $295 | $100 |

David Jones Premiere Credit Card | $0 | $99 | $99 |

These are the top credit card offers for 0% interest on purchases from our database at the time of writing.

Card | |

|---|---|

Interest-free offer | 0% for 15 months, then 22.49% p.a. |

Annual card fee | $199 |

Card | Bankwest Zero Classic Mastercard |

Interest-free offer | 0% for 6 months, then 18.99% p.a. |

Annual card fee | $0 |

Card | Bankwest Zero Platinum Mastercard |

Interest-free offer | 0% for 6 months, then 18.99% p.a. |

Annual card fee | $0 |

Card | |

Interest-free offer | 0% for 6 months, then 22.49% p.a. |

Annual card fee | $0 |

Card | Virgin Money No Annual Fee Credit Card |

Interest-free offer | 0% for 6 months, then 19.99% p.a. |

Annual card fee | $0 |

| Card | Interest-free offer | Annual card fee |

|---|---|---|

0% for 15 months, then 22.49% p.a. | $199 | |

Bankwest Zero Classic Mastercard | 0% for 6 months, then 18.99% p.a. | $0 |

Bankwest Zero Platinum Mastercard | 0% for 6 months, then 18.99% p.a. | $0 |

0% for 6 months, then 22.49% p.a. | $0 | |

Virgin Money No Annual Fee Credit Card | 0% for 6 months, then 19.99% p.a. | $0 |

These are the top 0% balance transfer credit card offers on our database at the time of writing, based on the duration of the offer.

Card | ANZ Low Rate Credit Card - Balance Transfer Offer |

|---|---|

Balance transfer offer | 0% for 26 months, then 21.99% p.a. |

Balance transfer fee | 3% |

Annual card fee | $0 for first year, then $58 |

Card | Bankwest Breeze Classic Mastercard® |

Balance transfer offer | 0% for 24 months, then 12.99% p.a. |

Balance transfer fee | 3% |

Annual card fee | $49 |

Card | Bankwest Breeze Platinum Mastercard |

Balance transfer offer | 0% for 24 months, then 12.99% p.a. |

Balance transfer fee | 3% |

Annual card fee | $59 |

Card | Latitude Low Rate Mastercard |

Balance transfer offer | 0% for 24 months, then 29.99% p.a. |

Balance transfer fee | 3% |

Annual card fee | $69 |

Card | MyCard Clear - Balance Transfer Offer 24 Months |

Balance transfer offer | 0% for 24 months, then 22.24% p.a. |

Balance transfer fee | 3% |

Annual card fee | $149 |

Card | Westpac Low Rate Credit Card |

Balance transfer offer | 0% for 20 months, then 21.99% p.a. |

Balance transfer fee | 3% |

Annual card fee | $84 |

Card | Bank of Melbourne, BankSA and St.George Vertigo Card - Balance Transfer Offer |

Balance transfer offer | 0% for 20 months then 21.99% p.a. |

Balance transfer fee | 2% |

Annual card fee | $0 for first year, then $84 (charges as $7 per month) |

Card | MyCard Clear - Balance transfer offer |

Balance transfer offer | 0% for 20 months then 22.24% p.a. |

Balance transfer fee | 2% |

Annual card fee | $149 |

Card | MyCard Rewards - Balance Transfer Offer |

Balance transfer offer | 0% for 15 months, then 22.99% p.a. |

Balance transfer fee | 2% |

Annual card fee | $199 |

Card | Heritage Bank Gold Low Rate |

Balance transfer offer | 0% for 12 months, then 11.80% p.a. |

Balance transfer fee | |

Annual card fee | $0 |

Card | Coles No Annual Fee Mastercard |

Balance transfer offer | 0% for 12 months, then 20.74% p.a. |

Balance transfer fee | 5% |

Annual card fee | $0 |

Card | NAB Low Fee Credit Card |

Balance transfer offer | 0% for 12 months, then 21.74% p.a. |

Balance transfer fee | 3% |

Annual card fee | $49 |

| Card | Balance transfer offer | Balance transfer fee | Annual card fee |

|---|---|---|---|

ANZ Low Rate Credit Card - Balance Transfer Offer | 0% for 26 months, then 21.99% p.a. | 3% | $0 for first year, then $58 |

Bankwest Breeze Classic Mastercard® | 0% for 24 months, then 12.99% p.a. | 3% | $49 |

Bankwest Breeze Platinum Mastercard | 0% for 24 months, then 12.99% p.a. | 3% | $59 |

Latitude Low Rate Mastercard | 0% for 24 months, then 29.99% p.a. | 3% | $69 |

MyCard Clear - Balance Transfer Offer 24 Months | 0% for 24 months, then 22.24% p.a. | 3% | $149 |

Westpac Low Rate Credit Card | 0% for 20 months, then 21.99% p.a. | 3% | $84 |

Bank of Melbourne, BankSA and St.George Vertigo Card - Balance Transfer Offer | 0% for 20 months then 21.99% p.a. | 2% | $0 for first year, then $84 (charges as $7 per month) |

MyCard Clear - Balance transfer offer | 0% for 20 months then 22.24% p.a. | 2% | $149 |

MyCard Rewards - Balance Transfer Offer | 0% for 15 months, then 22.99% p.a. | 2% | $199 |

Heritage Bank Gold Low Rate | 0% for 12 months, then 11.80% p.a. | $0 | |

Coles No Annual Fee Mastercard | 0% for 12 months, then 20.74% p.a. | 5% | $0 |

NAB Low Fee Credit Card | 0% for 12 months, then 21.74% p.a. | 3% | $49 |

Most credit cards in Australia come with some form of intro offer to incentivise customers to sign up. It’s something consumers have come to expect, particularly on rewards credit cards and frequent flyer credit cards.

In fact, Money.com.au’s database shows only around 15% of cards don’t have any sign-up offer at all, whether it’s bonus points, cashback, a 0% balance transfer offer or a fee waiver.

Some cards even offer a few different intro offers to choose from when you sign up. But just like the cards themselves, deciding which kind of sign-up offer will be best for you is not necessarily straightforward.

Below we breakdown the different kinds of offers and how they work.

How it works: Bonus points for signing up is what probably comes to mind for most people when they think of a credit card special offer. What usually happens is new customers must spend a certain amount using the card within the first few months, and in return they get a lump sum of rewards points credited to their account.

The reason for the minimum spend is credit card companies typically get a small cut when you use your credit card for a purchase. Making the bonus points conditional on you spending, say, $5,000 in the first three months with the card means the card issuer is earning revenue. This offsets the cost of the bonus points they’re ‘giving away’. It also gets you into the habit of spending with the card early on. The minimum spend is usually pretty achievable.

Typical offer amounts: Sign-up offers usually range from 20,000 to 250,000 bonus points. Providers usually offer a higher number of bonus points on their own rewards program, with lower bonuses available on Qantas credit cards and for Velocity point offers.

What’s the catch? As an added eligibility hurdle, it’s becoming more common for bonus sign-up point offers to be spread across the first two years. So you get the first batch of points in year one if you meet the minimum spend, and then another batch after 12 months with the card. There may even be a further minimum spend requirement for the year-two points to make things even more complicated.

Spreading the bonus over two years means the cardholder will need to pay two years’ worth of annual card fees. It also makes it less appealing for customers to ‘churn’ credit cards, which means repeatedly taking out new credit cards to get the bonus points and then cancelling when the points are spent.

How it works: This is much less common, but some credit cards (the HSBC Platinum Qantas Credit Card is an example) offer a higher points earn rate in the first year as a sign-up bonus of sorts. The incentive is ultimately the same – more rewards points at the start to get you on board.

Typical offer amounts: As an example, you might earn 1.5 points per $1 spent in the first year with the card and then 1 point per $1 you spent after that.

What’s the catch? In most cases, a lump sum at the start is going to deliver more impact for your points balance. Unless of course, you happen to be a phenomenally big spender in which case earning more per dollar you spend may be a better initial deal.

Ultimately, you’ll probably be better off with a card offering a high ongoing earn rate and bonus points for signing up.

How it works: Sometimes offered instead of or in addition to bonus points, cashback on a credit card usually comes in the form of a credit to your account. You can then use that credit for a purchase, or just use it to reduce your existing balance.

Getting cashback as a sign-up bonus is arguably more valuable than points as the value is guaranteed. Rewards points, on the other hand, vary in value from one program to the next and also in terms of how they’re spent. It’s not easy to objectively put a value on 100,000 bonus points, but $500 cashback is worth $500.

Typical offer amounts: The amounts on offer usually range from $250-$500 and are generally also conditional on the cardholder meeting a minimum spend in the first few months with the card.

What’s the catch? These offers are much less common compared to bonus point offers. If you have your heart set on cashback, you’ll have much fewer cards to choose from.

How it works: There are a lot of credit cards with no annual fee in the first year, or a discounted fee for the first 12 months. This is probably the simplest of all the credit card promotional offers to get your head around, with a clear unambiguous benefit.

Everything else about the card will be the same in that first year, you just don’t need to pay an annual fee.

In some rare cases, the fee is charged initially but then refunded if you meet certain conditions, like spending a minimum amount with the card. But usually that’s not the case and it’s a simple free kick.

Typical savings: The savings in the first year can range from around $500 all the way up to $500.

What’s the catch? When the party’s over you’ll need to pay the full annual fee in the second year with the card. This kind of offer might encourage you to get a more expensive card than you otherwise would if you were paying full wack from day one.

How it works: Interest-free credit card offers are becoming less and less common, but some cards do still offer this as a sign-up deal to entice new customers. So let’s say you have a card offering 0% on purchases for six months – you won’t be charged interest on any purchases made using the card for the first six months. Pretty simple.

It can be a very useful type of bonus offer if you have a large expense to cover and want to repay it over a few months with no interest.

Typical offer durations: Offer durations generally range from 6-12 months, with 15 months being about as good as it gets.

What’s the catch? If you haven’t cleared the balance during the offer period, the ongoing purchase rate will kick in. That rate may be quite high.

How it works: 0% balance transfer credit card offers are very common in Australia. In a nutshell, what that means is you can transfer a balance from another credit card to the new one and you won’t pay any interest on that balance on the new card during the offer period.

It makes it easier to pay down debt and can save you a lot of money if you have a big balance that’s racking up interest.

Typical offer durations: Offer durations usually ranging from 6-26 months, with 12 months being the average.

A trend we’re seeing more of at Money.com.au is cards offering a reduced interest rate (but not 0%) on balance transfers for a longer period of time. So instead of the offer being 0% on a balance transfer for 12 months, you pay 5.99% p.a. for 36 months. This may suit if it’s going to take you a long time to pay off the balance completely.

What’s the catch? After the offer period, a much higher interest rate will apply. It’s also generally very expensive to make new purchases using the card during the offer period.

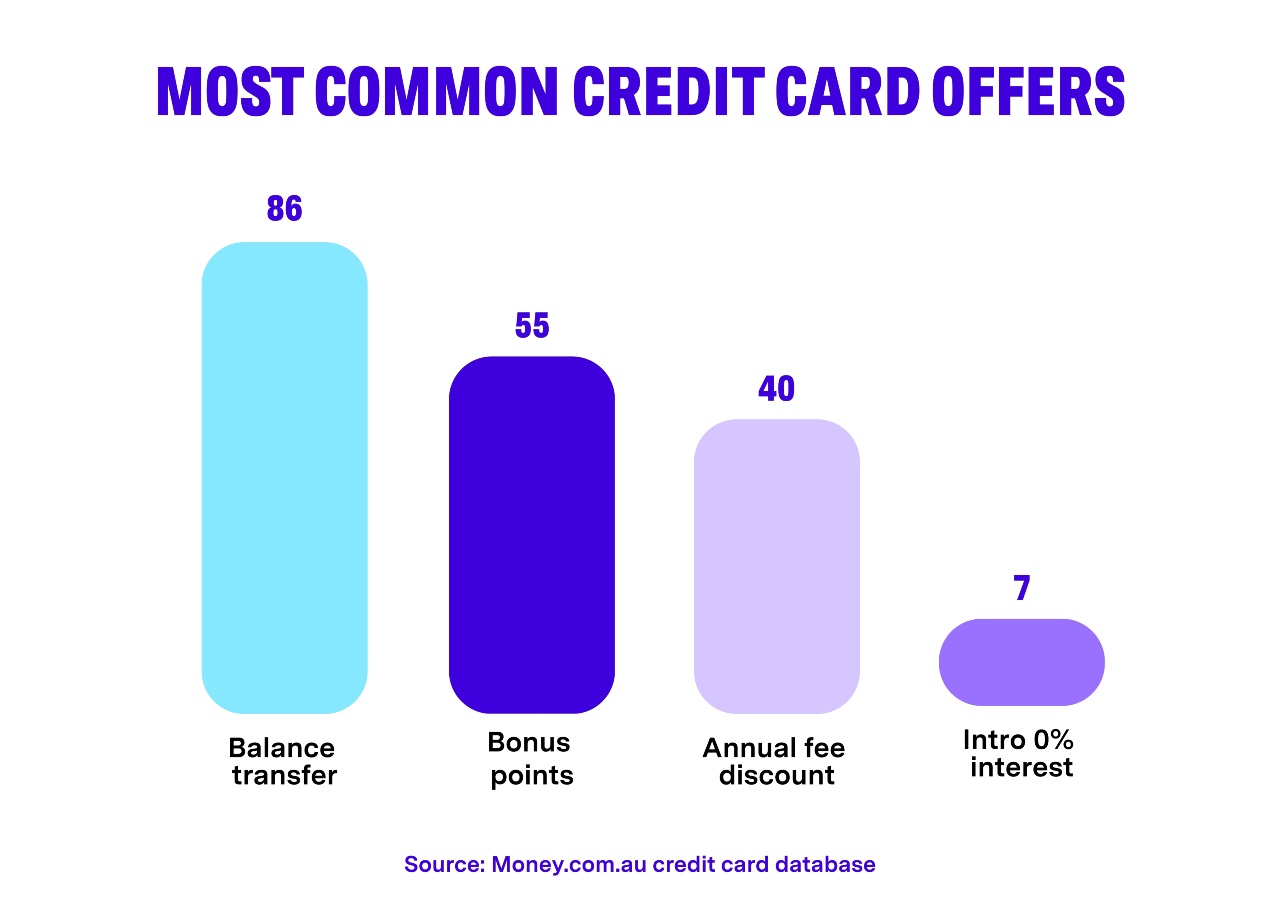

According to Money.com.au's credit card database, a balance transfer is the most commonly offered credit card promotion (86 different cards offer this), followed by bonus points (55), annual fee waiver/discount (40) and 0% interest offer (7).

An absolute bagful of bonus rewards points linked to an obscure rewards program may be very valuable, or they could be worth a lot less than a lower number of points linked to a better program. If you can’t easily work out what the points are worth, it may be best to keep looking for a more tangible benefit.

Even if the bonus is valuable on the face of it, is it valuable to you based on how you shop and spend? For example, if you can’t redeem the bonus points for the things you want, the value will be heavily reduced in reality. Flexibility is arguably just as important as the raw number of points.

Avoid bonus credit card offers that require big minimum spends or other restrictive eligibility criteria. You don't want to end up jumping through potentially expensive hoops. In other words, the juice needs to be worth the squeeze. Timing matters too. All other things being equal, you’re better off with an offer where you actually get the benefit sooner rather than later.

Signing up for an expensive credit card or one with limited ongoing benefits is rarely a good idea, even if you get a sweetener for signing up and you only plan to keep the card long enough to cash in on the bonus offer. There are enough offers available that you should be able to find one on a card that’s a good fit for you and competitive overall.

How you use your credit card initially is likely to dictate how you use it over the longer term. At least to some extent. Avoid offers that are conditional on you spending big at the start. There’s always the risk that this spending pattern might stay with long after the bonus offer’s been and gone.

Nearly half of Australians with a credit card (49%) are ‘churners’ and admit to signing up for new cards only to collect bonus rewards points, Money.com.au research shows.

Among them, 30% say they’ve done it once or twice to boost their points balance, while 19% regularly sign up for new credit cards specifically to collect bonus rewards points.

Sean Callery, Editor

Let’s break this down into the two main categories of credit cardholders: those looking to earn rewards and those looking to keep costs down.

If you’re looking to maximise rewards, the nature of how rewards credit cards work mean bonus offers are a big part of the overall value you get over the life of the card.

Bonus points or cashback (assuming you don’t have to change your good spending habits to qualify) will help offset the cost of the card, so the ongoing benefits the card offers cost less.

And there are enough offers in the market to make it possible for most people to find a credit card that suits their needs with an offer attached.

If, on the other hand, you really just want to keep costs down, bonus offers should be much less of a priority. Unless, of course, it’s a first-year annual fee waiver or interest-free offer on an already-cheap card. Then why not!

Sean Callery, Editor

Now might be as good a time as any to take advantage of a credit card sign up offer. Upcoming changes to Australia's payments system (being introduced on 1 October 2026) will mean credit card companies will make less money from customers using their cards for spending. This will likely lead to less generous benefits and sign-up offers in future as card providers look to reduce costs.

This page features the top credit card offers on Money.com.au’s database of more than 200 consumer credit cards (we compare business credit cards separately). We’ve broken down the cards into offer categories, with the top cards in each category shown in our comparison.

Our inclusion and sort criteria are pretty simple:

There are generally higher-value credit card offers available if you want rewards points. When converted to gift cards, some of the top bonus points offers re worth the equivalent of $1,000+, whereas cashback offers generally cap out at around $500.

But cards offering cashback tend to have lower annual fees, so you need to factor that into the equation.

There’s no set limit on how often you can switch credit cards to jump between offers, but in reality, switching too often is not a great idea. In order to get the full value from most credit card sign-up offers, you’ll need to keep the card for at least two years. If you switch before that, you’ll only get part of the offer.

Making a lot of credit card applications also shows on your credit report and hurts your credit score. Card providers do a credit check when you submit an application and if they can see a lot of recent card applications, you may not be approved.

A smart approach is to find the best credit card for your needs and take it as a bonus if there’s an offer attached. It shouldn’t be the only reason you get a credit card. Switching every few years is okay, assuming you continue to use your card sensibly and don’t change your good spending habits in order to chase bonus deals.

Right now, the top credit card sign-up offer is 250,000 rewards points with the MyCard Prestige credit card. To qualify, you’ll need to spend $10,000 on eligible purchases within the first 90 days from approval.

Those points are likely to be worth around $1,000 when converted to gift cards. The card has a $700 annual fee.

Credit card debt is a genuine problem for a large number of people in Australia and around 30% of those with a credit card do not pay off their balance in full each month according to Money.com.au research.

Credit card sign-up offers certainly encourage people to get a credit card (that’s the whole point) and some of them encourage spending as there is often a minimum spend requirement to get the bonus.

But the minimum spends are usually fairly modest and broadly in line with the average credit card spend among Australians. In addition, credit card companies are legally required to lend responsibly, and offer limits that people can afford. So it’s hard to argue that credit card special offers directly encourage people to get into debt, but in pushing people towards credit products, these offers may mean some people consider getting a credit card when they might be better off without one.

The key is understanding why you need a credit card and finding a product that will be a good fit based on that need. If you don’t actually need a credit card, don’t get one, even if it means missing out on special offers. Simple.

Generally credit card companies offer their best top sign-up offers and deals towards the end of the year (September - December). They do this to capture the increased demand for credit cards during the busiest shopping months and those looking for a travel credit card during the peak holiday season.

Sean Callery is the Editor of Money.com.au. He has over 15 years of international experience. He is qualified with a Certificate IV in Finance and Mortgage Broking (FNS40821) and is compliant to provide general advice in Tier 1 General Insurance (RG 146) products.

Isabella Visser is a Finance Writer with Money.com.au. With her experience in journalism and writing content across multiple platforms she makes finance simpler for readers by creating insightful and engaging content.

General information only

The information on this page is general in nature and has been prepared without considering your objectives, financial situation or needs. You should consider whether the information provided and the nature of the credit card product is suitable for you and seek independent financial advice if necessary.

We are not providing you with a recommendation or suggestion about a particular credit product. You should read the relevant disclosure statements or other offer documents before deciding whether to apply for or continue to hold a particular credit card.

What products, features and information are shown

While we make every effort to ensure all credit cards available in Australia are shown in our comparison tables, we cannot guarantee that all products are included. Where we become aware of a card that is missing from our tables, we commit to adding it within one business day.

Our product comparisons may not compare all card features and attributes relevant to you.

Product information, such as interest rates, fees and charges, is subject to change without notice. Before acting on any information, you should confirm the relevant product information with the card issuer. While we do our best to ensure the information provided on this website is accurate, all information on this website is provided without any representation or warranty, either express or implied, being given as to the accuracy, completeness, timeliness, reliability or otherwise of its content. No responsibility is accepted by us for any errors, omissions or any inaccurate information on this website.

How cards are sorted and filtered by default

Users can easily change the sort order and apply product filters to our product comparison tables. However, when you arrive on a page initially or select a particular card type via the ‘card features’, a default sort order is applied as follows:

We may earn a commission from product providers if you are issued with a credit card via a link from this page. Cards marked as ‘sponsored’ are not selected or positioned on the page solely based on their product attributes. In our comparison tables, products are displayed based on the relevant default sort order and filters applied for that card type, or the sort order and filters selected by a user. We may earn a commission if you are issued with a card via a link from our comparison tables.