What is a travel credit card?

Travel credit cards have built-in features that make them better suited to domestic or international travel. They help travellers save money on holiday expenses and get more back in rewards.

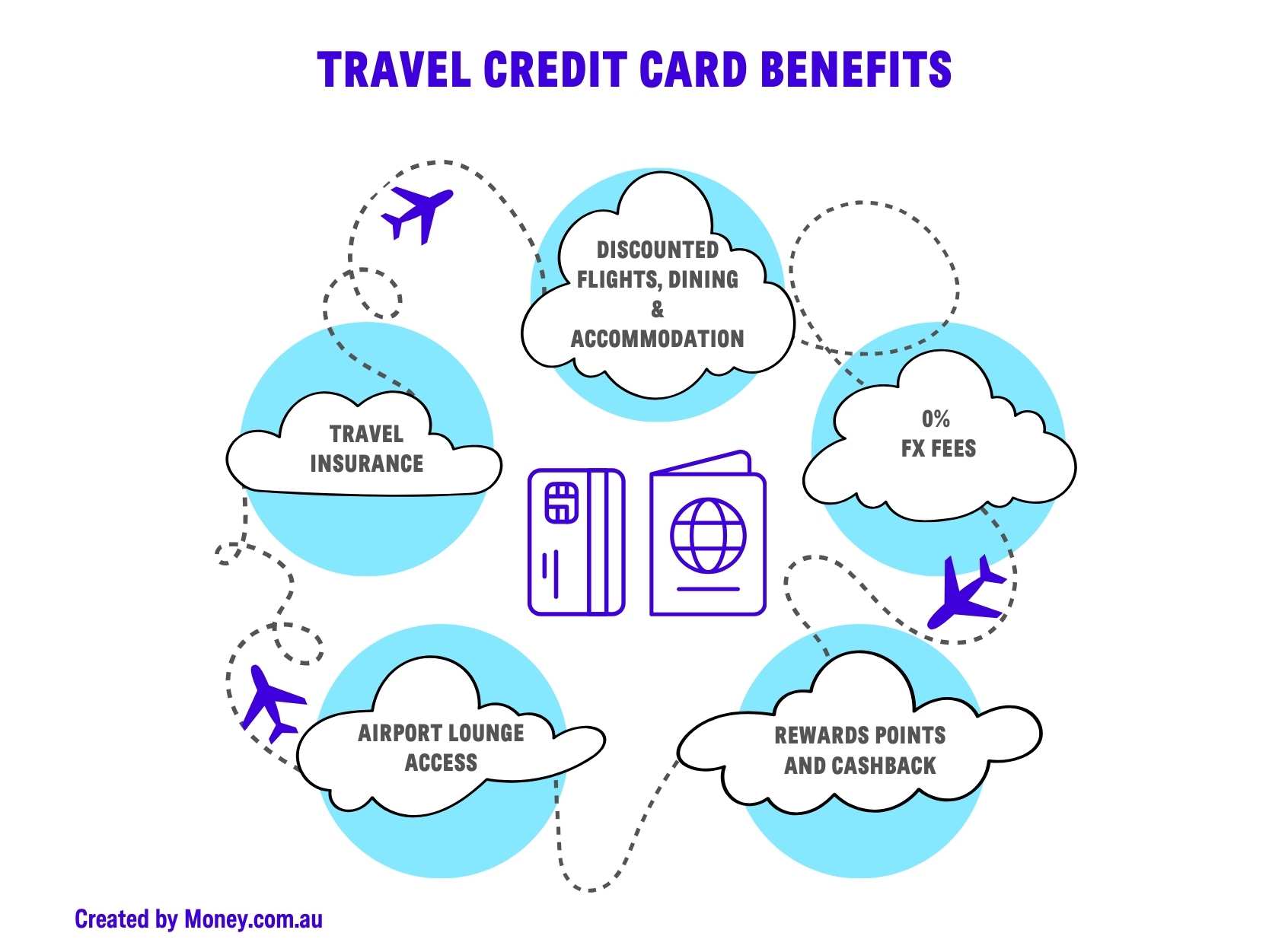

Common travel credit card features include complimentary travel insurance, 0% foreign transaction fees and reward points that are linked to airline frequent flyer programs.

How does a travel credit card differ from an everyday credit card?

Travel credit cards prioritise providing benefits and lowering expenses for overseas holidays. Most everyday credit cards can be used internationally, and travel cards can function as a regular credit card within Australia, but travel cards offer more perks that regular travellers will value.

For example, according to the latest Money.com.au data:

- Two in five credit cardholders used a card with no foreign transaction fees during their most recent overseas trip.

- Australians who redeemed frequent flyer points over the past year saved an average of $1,140 on travel and accommodation costs.

6 key questions to ask when comparing travel credit cards

What’s the foreign transaction fee?

It will be somewhere between 0% and 3% of the transaction value depending on the card. If you regularly travel abroad or shop online from overseas retailers, it’s worth minimising this fee as much as possible.

Will the card be accepted where I’m travelling?

Mastercard and Visa are accepted almost everywhere. Amex is a bit more limited but still widely accepted in the countries Australians travel to in numbers. If you regularly travel off the beaten track, your choice of card network matters.

What’s the purchase rate?

The purchase rate is the interest charged on new purchases if you don’t pay your balance in full. Ideally you’ll be clearing the balance of the card within the interest-free period, but if not, a lower interest rate will help you minimise your travel costs.

What’s the annual card fee?

There are some credit cards with no annual fee that offer benefits for travellers, but most do come with a fee. If there is a fee, look carefully at what you’re getting in return.

Is travel insurance included?

A credit card that comes with travel insurance included could save you hundreds of dollars if it means you don’t need to purchase a separate travel insurance policy. Pay attention to what is covered by the policy and if it’s suitable for you.

Are there any other travel benefits thrown in?

Some travel credit cards offer lounge access (usually a limited number of passes per year), plus travel discounts and credits you can put towards flights, accommodation and dining. These can be a nice ‘cherry on top’ if the rest of the card fits the bill.

Why planning your overseas spending matters

Brad Kelly, Credit Card Expert

“You've got to be a bit strategic about how you’ll spend money overseas. So plan ahead. The truth is, if you don’t, the potential for getting walloped with fees or being massively inconvenienced is far greater than it is when you’re using your credit card in Australia.”

Brad Kelly, Credit Card Expert

Expert credit card tips for travelling smarter

Cover as many of your costs as you can before you travel

As soon as you leave Australia (or buy from an overseas retailer) you become a much more profitable customer for your bank because of the fees they charge. Avoid foreign exchange fees by prepaying for as many expenses as you can (e.g. your accommodation) assuming you can do so in AUD.

Get clear on fees

If you’re going to be spending overseas regularly, it’s worth seriously considering a credit card with 0% foreign transaction fees. This could save you up to 3.65% on every transaction. This fee is often overlooked when people apply for a credit card. Also be clear on what you’ll be charged for using an ATM. Chances are it will be a lot. Research from Money.com.au reveals a third of Australians (33%) have experienced at least one card payment issue on their most recent overseas trip. The most common issue was unexpected foreign transaction fees or unknown charges when using a card (15%).

Don’t accept the “Do you want to pay in Australian Dollars” option

When you’re making a card payment overseas, a lot of the time you’ll get the option to pay in the local currency or have the amount converted to Australian dollars. Paying the AUD amount shown would seem like the sensible choice here, but trust me, it’s almost always a rip off. That option involves what’s called dynamic currency conversion which means the conversion rate is determined by the merchant and it’s usually a much worse rate than what your credit card provider will give you if you pay in the local currency.

Don’t withdraw cash overseas using your credit card

Using a credit card to withdraw cash at an overseas ATM is going to be very expensive. You’ll be stung with a fee from the local ATM operator (unless it happens to be a Westpac card and the ATM is part of the Global ATM alliance), a foreign transaction fee, plus a cash advance fee. You won’t get any interest-free days, meaning you’ll immediately be paying a high rate of interest on the funds you withdrew. Basically unless it’s an emergency, don’t go near an ATM with your credit card.

Make sure you ‘trigger’ your card’s travel insurance

Even if your credit card comes with travel insurance, there’s a good chance it won’t cover your trip automatically. You usually need to trigger the cover, in many cases by booking the travel/accommodation using the card itself. If you pay in full with card points (e.g. with Qantas credit card points), that mightn’t be enough to trigger the insurance – you usually need to make an actual card purchase.

Have at least one backup payment option

When it comes to travel in particular, one card does not fit all. You might like the idea of using a single card for all your spending, but there are situations when a debit card will be better. Having a card from a different financial institution can also be a life-saver if your primary bank has an outage while you’re away.

Bonus tip: Bring the physical card with you

Brad Kelly, Credit Card Expert

"In Australia we’re very used to paying through a phone or watch using the likes of Apple Pay and Google Pay. But that kind of payment is not as widely accepted overseas.

You’ll need to use the physical card and, for a dose of nostalgia, you may even need to insert it into a card chip reader and enter a PIN. You will also likely need to have the physical card if you’re using your card for pre-authorisation when checking into a hotel or renting a car."

Brad Kelly, Credit Card Expert

Research from Money.com.au reveals that flights were the most common way Australians redeemed their frequent flyer points, with half (50%) using points for airfares during the last twelve months. Almost one in three Aussies (31%) used points for a mix of flights and accommodation, while a further 19% redeemed points for accommodation only.

The survey found that only 60% of Australians used frequent flyer or credit card points for travel in the past 12 months. The remaining 40% either didn't earn travel points or didn’t redeem any points during the period.

Pros and cons of travel credit cards

Pros

- Some travel credit cards feature cost-effective travel perks like zero international transaction fees.

- The opportunity to earn rewards points from frequent flyer programs and use them towards future travel expenses.

- Having access to complimentary travel insurance, airport lounges and discounted flights and accommodation.

Cons

- Fees (e.g. annual card fee, cash advance fees) are typically higher than those on everyday credit cards.

- High interest rates on purchases and cash advances.

- The possibility of overspending on the credit card when on holiday and having debt to clear long after the trip has been and gone.