Banking research & insights

Money.com.au conducts ongoing consumer surveys and data analysis to uncover trends in how Australians use and manage their savings accounts, term deposits and everyday banking.

Research is compiled by our experienced PR & Editorial team. Updated 24 Jun 2026.

Below you’ll find the latest Money.com.au consumer research relating to banking and deposits, ordered from most recent to least.

All surveys are independently conducted by a third-party research agency and are nationally representative by age, gender and location.

Featured across major news outlets, our research helps Australians decide how and where to keep their money and provides insights into how they prefer to transact. It also offers journalists and policymakers clear, data-driven insights.

If you use this information, please include a link to the page you’re currently on: https://www.money.com.au/banking/research-insights.

Want to see more Money.com.au research and insights? Add us as a preferred source in Google Search.

Banking research & insights

Savings tax sting: Aussies to hand more than $500 of their interest earnings to the ATO

Millions of Australians are earning more interest on their savings after three cash rate hikes this year boosted savings rates, but a significant share of those returns will end up in the tax office's coffers.

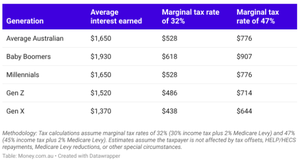

New research from Money.com.au reveals Australians earned an average of $1,650 in savings interest over the past 12 months. While higher savings rates have boosted returns, they've also increased the amount of tax many savers owe.

Assuming a marginal tax rate of 32% paid by the average earner, a saver could face a tax bill of $528 on their interest earnings, which would reduce their average after-tax savings return to $1,122. For someone on the top marginal tax rate of 47%, the tax bill rises to $776, meaning almost half of their interest earnings could end up with the ATO, leaving them with just $874 to keep.

On a national level, this means Australians could collectively hand almost $11.2 billion to the ATO in tax on savings interest this financial year.

Money.com.au’s Finance Expert, Sean Callery, says Australians naturally focus on the interest they're earning without considering how much of it may ultimately be lost to tax.

“It's somewhat disheartening to see how much of the interest you've earned through disciplined saving can be lost to tax. Many Australians are doing everything right — setting money aside and jumping through hoops to meet bonus interest conditions — only to find that a sizeable chunk of those earnings ends up with the ATO when they file their tax return,” he says.

"The more cash you have sitting in a high-interest savings account or term deposit, the more important it is to factor tax into your expected return. For example, a savings account advertising a 5% interest rate might effectively deliver closer to 3.4% after tax for an average income earner."

"This can come as a shock for people with larger savings balances, particularly those saving for a house deposit or retirees relying on interest income to supplement their cash flow. Many are counting on those interest earnings to help grow their savings or support their lifestyle, but may not realise the tax bill on that income can run into the thousands of dollars when they lodge their tax return."

"If you're a homeowner with a mortgage, you may be better off parking your savings in an offset account rather than a traditional savings account. Any interest you save on your mortgage through an offset account naturally isn't treated as taxable income, so you get to keep the full benefit."

Baby Boomers face the biggest tax bills on savings interest

The research found that Baby Boomers earned the most savings interest over the past 12 months, averaging $1,930. Assuming a 32% marginal tax rate, that would translate to a tax bill of $618. For those on the top marginal tax rate of 47%, the tax bill rises to $907, meaning almost half of their interest earnings will be lost to tax.

Millennials earned an average of $1,650 in savings interest over the same period, followed by Gen Z ($1,520) and Gen X ($1,370). At a 32% marginal tax rate, this would equate to tax bills of $528, $486 and $438 respectively. At the top marginal tax rate of 47%, the tax bill would rise to $776 for Millennials, $714 for Gen Z and $644 for Gen X.

H&R Block Director of Tax Communications, Mark Chapman, says savings interest is added to your other assessable income and taxed at your marginal tax rate.

“Many Australians don't think of bank interest as taxable income, but from the ATO's perspective it's no different to salary, rent or dividends,” he says.

"Many people mistakenly believe they're only taxed on savings interest when they withdraw the money. In reality, interest is generally assessable for tax purposes as soon as it's credited to your account, regardless of whether you spend it or leave it there.”

“After several years of elevated savings rates, many Australians are earning substantially more bank interest than they did previously. Some taxpayers who have never paid much attention to savings interest may find the amount is now significant enough to noticeably affect their tax bill.”

-- ENDS --

Survey: 45% of Aussie retirees don’t know if their savings are keeping up with inflation

Many Australians in or approaching retirement rely on cash savings to supplement their income — but new research shows many may be unknowingly falling behind the rising cost of living.

A new survey by Money.com.au reveals almost half of Australians in their 60s (45%) don’t know whether the interest rate on their savings account is keeping pace with inflation.

Among those who do track their savings rate, 26% say it’s below inflation, meaning their money is losing value in real terms. Meanwhile, 14% say it’s roughly keeping pace with the cost of living.

Just 16% of Baby Boomers say their savings are outperforming inflation.

To preserve the value of savings, interest needs to at least match inflation. With annual inflation currently at 3.8%, any savings account earning less than this may see balances rise on paper, but buy less in real terms over time.

Money.com.au’s Finance Expert, Sean Callery, says many older Australians still underestimate how quickly inflation can erode cash, even when they rely on savings for day-to-day living.

“Inflation is a silent tax on cash savings. If prices are rising faster than the interest you’re earning, your money buys less over time. Currently, just under a third of savings accounts in the market offer an interest rate above inflation, which means the odds aren’t in your favour unless you’re actively seeking out a competitive rate,” he says.

“When almost half of older Australians have no clue whether their savings are going forwards or backwards, it makes it much harder to make informed decisions about where to park their cash.” Sean says savings accounts remain an important and appropriate option for seniors, especially retirees and pensioners who value stability and access to their money. “In uncertain economic times, you may naturally keep more money in savings because it feels safe and that makes sense. But some savers are actually paying for that safety in lost purchasing power. If you haven’t reviewed your savings rate in a while, it may no longer be keeping up with rising living costs,” he says.

How inflation can strip more than $600 a year from savers Someone with $50,000 in savings earning a relatively low rate of 3% p.a., and adding $1,000 a month, would finish the year with $63,687 in their account. Once the 3.8% annual inflation rate is taken into account, that balance would be worth around $61,355 in today’s dollars. Despite regular saving and interest earnings, their purchasing power has fallen by about $645 before tax.

By contrast, a saver earning a top ongoing rate of 4.75% p.a. would finish the year with around $64,692. Adjusted for inflation, that’s worth about $62,320. They would be roughly $320 better off in real terms before tax.

Note: Modelling assumes an initial savings balance of $50,000 held for 12 months, with $1,000 added monthly and interest calculated and paid monthly. Savings rates of 3% p.a. (average deposit rate) and 4.75% p.a. (top ongoing savings rate) are quoted before tax. Headline inflation is 3.8% for the 12 months to December 2025. ‘Real’ gains or losses reflect the change in purchasing power after adjusting the savings balance for inflation over the same period.

5 ways older Australians can protect their savings

-

Check your savings rate regularly Many older Aussies use their savings to supplement income rather than build wealth. Many savings accounts start with competitive introductory or promotional rates that drop after a few months, and banks also adjust rates when the cash rate changes. Check your base or ongoing rate regularly to ensure your savings continue to support day-to-day living costs.

-

Check the bonus conditions on your savings account If you rely on savings for income, missing out on bonus interest can make a real difference over time. In many cases, earning the highest interest rate requires that you meet certain conditions each month, like making regular deposits or growing your balance. Our research shows most Australians fail to earn the bonus interest on their savings account each month, often because they’re unsure what those conditions are.

-

Compare your interest rate against inflation, not just last year’s balance If you're living on a fixed or semi-fixed income, preserving purchasing power is key. Even if your balance is growing, it may still be losing value if inflation is higher than the interest you’re earning. Ideally, your savings rate should at least match inflation to maintain its real value, but ideally sit above it.

-

Review whether you need multiple savings accounts Some banks cap their highest savings rates at a set balance (for example, $30,000). If you have larger cash balances set aside for emergencies or living expenses, spreading funds across more than one account may help maximise interest, provided the benefits outweigh the extra admin.

-

Don’t assume loyalty equals a better rate Many savers stay with the same bank for decades. However, banks rarely move long-standing customers onto their best savings rates. If you’ve had the same account for several years, it may be worth checking whether newer accounts offer better ongoing rates, or comparing your options elsewhere.

-- ENDS --

46% of Australians include travel among their top savings goals for 2026

New research from Money.com.au reveals Australians are again putting travel at the top of their savings priorities heading into the new year, ahead of buying a home, investing or saving for retirement.

The nationally representative survey found that 46% of Australians — equivalent to 10.2 million people — included saving for a holiday among their savings goals for 2026. It's the second year in a row holidays have topped the list of savings priorities, after a similar result last year (49%).

Building an emergency fund was the next most frequently cited goal (42%), followed by saving for retirement (35%) and saving to buy a home (26%). Fewer Australians nominated investing (23%), paying off their mortgage sooner (13%), home renovations (10%) or saving for children (5%). Respondents were asked to nominate their top two savings goals.

Money.com.au’s Finance Expert, Sean Callery, says travel is one of the few financial goals that still feels achievable and emotionally rewarding for many Australians.

“Most people can realistically plan for, budget toward and genuinely look forward to an overseas trip within a year, so it’s no wonder it remains a strong priority for Australians, even as cost-of-living pressures continue,” he says.

“Our research shows that it takes Aussies, on average, about eight months to save for a holiday, which shows travel is something people are prepared to invest time and planning into. Asia remains a popular destination because that’s where you can enjoy premium experiences without the premium price tag.”

Sean says travel experiences are increasingly being valued in the same way traditional milestones once were, particularly among younger Australians.

“Holidays, cruises and even backpacking have become a new kind of life currency. Experiencing new places and cultures can hold similar value to traditional assets for Aussies in their 20s and 30s who often feel locked out of milestones like home ownership or starting a family.”

The survey found that Baby Boomers were the most likely to include saving for a holiday among their top savings goals this year (53%), followed by Gen Z (50%), Gen X (45%) and Millennials (34%).

Travel demand holds firm as overseas trips climb

ABS data shows the number of short-term overseas trips taken by Australians rose by 9.2% in the year to October 2025, compared with the previous year.

Figures show January, July and October tend to be the busiest months for Australians returning from overseas trips, which aligns with school holidays and peak travel seasons in popular destinations like the US, Europe and Japan.

“Australians can generally stretch their travel budget further by planning trips outside peak holiday periods, when demand, and often prices, tend to be lower,” says Sean.

-- ENDS --

‘Silent tax’: 47% of Australians don’t know if their savings are going backwards

Inflation doesn’t just influence RBA cash rate decisions — it also affects how much Australians’ savings are worth in real terms.

New research from Money.com.au reveals almost half of Australians (47%) don’t know whether the interest rate on their savings account is keeping up with inflation.

Among those who do keep track, 26% say their savings rate is below inflation, meaning their money is going backwards in real terms, while 16% say it’s roughly keeping pace.

Just 12% of Australians say their savings are outperforming inflation.

Savings need to keep pace with inflation to hold their value. With annual inflation running at 3.8%, any savings rate below that means your balance might grow on paper, but it actually buys less over time.

Money.com.au’s Finance Expert, Sean Callery, says many Australians underestimate how quickly inflation can erode cash savings.

“Currently, just under a third of savings accounts on the market offer an interest rate above inflation, which means the odds aren’t in people’s favour unless they’re actively seeking out a competitive rate,�” he says.

“Inflation is a silent tax on cash savings. If prices are rising faster than the interest you’re earning, your money buys less over time. When almost half of Australians have no clue whether their savings are going forwards or backwards, it makes it much harder to make informed decisions about where to park their cash.”

“In times of economic uncertainty, people naturally prefer to keep their money in savings accounts because that’s where it feels safest. That’s fine, but it’s still important to regularly check whether your interest rate is keeping up with the cost of living, particularly for retirees and pensioners who rely on their cash savings to fund day-to-day spending.”

How inflation quietly strips $500 a year from savers

Someone with $30,000 in savings earning a relatively low rate of 3% p.a., and adding $1,000 a month, would finish the year with $43,079 in their account. Once the 3.8% annual inflation rate is taken into account, that balance would be worth around $41,500 in today’s dollars. Despite regular saving and interest earnings, their purchasing power has fallen by about $500 before tax.

By contrast, a saver earning a top ongoing rate of 4.75% p.a. would finish the year with around $43,721. Adjusted for inflation, that’s worth about $42,120. They would be roughly $120 better off in real terms before tax.

Note: Modelling assumes an initial savings balance of $30,000 held for 12 months, with $1,000 added monthly and interest calculated and paid monthly. Savings rates of 3% p.a. (average deposit rate) and 4.75% p.a. (top ongoing savings rate) are quoted before tax. Headline inflation is 3.8% for the 12 months to December 2025. ‘Real’ gains or losses reflect the change in purchasing power after adjusting the savings balance for inflation over the same period.

Savings confusion spans every generation

Confusion about whether savings are keeping up with inflation is common across every age group. Half of Gen X (50%) say they don’t know how their savings rate compares with inflation, followed by Gen Z (48%), Baby Boomers (45%), and Millennials (44%).

Older Australians were slightly more likely to say their savings are outperforming inflation, with 15% of Baby Boomers saying they’re ahead, compared with 13% of Gen X. That compares with 10% of Millennials and just 8% of Gen Z.

-- ENDS --

Survey: 56% of Aussies fail to earn bonus savings interest every month

New research from Money.com.au reveals the majority of Australians (56%) fail to earn the bonus interest on their savings account every month, costing them hundreds of dollars a year.

Among them, 29% earn their bonus rate in most months of the year but not all (7–11 months), while 13% only qualify for less than half the year (fewer than six months). A further 14% admit they don’t know the bonus rate eligibility criteria for their savings account.

The survey found that only 44% of Australians consistently earn their bonus interest every month of the year (12 months).

A bonus interest rate is the extra interest you can earn on your savings account when you meet certain conditions each month, like making regular deposits or growing your balance.

Money.com.au’s Finance Expert, Sean Callery, says it’s often the fine print that stands between savers and their full bonus rate.

“Bonus interest rates are attractive, but they nearly always come with hoops to jump through, like not being allowed to make withdrawals, needing to grow your balance every month, or even making a set number of card purchases.

These conditions can be tricky to keep track of, and many savers lose out because they miss one small step. People often don’t realise they’ve forfeited the bonus rate until it’s too late,” he says.

“The key is understanding exactly what your bank expects each month. Automatic deposits can help you meet the minimum deposit requirements without thinking about it. It’s also worth reviewing your account regularly, because banks are constantly adjusting their bonus rules and rates.”

Gen Z most likely to miss out on bonus interest

Younger Australians are the most likely to lose out on bonus interest, with 67% of Gen Z failing to qualify every month. This compares to 59% of Gen X, 53% of Millennials and 49% of Baby Boomers.

There is also a clear knowledge gap: 20% of Gen Z say they don’t know the conditions required to earn their bonus interest, compared with 6% of Millennials, 15% of Gen X and 15% of Baby Boomers.

Useful background information:

In 2023, the ACCC conducted an inquiry into retail deposit products and found that a large proportion of savers were missing out on bonus interest because the conditions were too complex or difficult to meet. The regulator noted that many customers didn’t realise they had forfeited the bonus rate until after the fact, and recommended that banks alert customers when they are at risk of losing their bonus interest and introduce simpler rules to help Australians earn the full interest available to them.

-- ENDS --

Survey: More than half of Australians don’t know their savings rate, survey finds

New research from Money.com.au reveals that millions of Australians may be earning less on their savings simply because they don’t know the interest rate their bank is paying.

The nationally representative survey found that 57% of Australians — equivalent to 12 million people — don’t know their current savings rate. Of those, 32% said they only have a rough idea, while 25% have no clue because they don’t track it at all.

Only 35% of Aussies know their current savings rate, while 8% don’t have a savings account.

Money.com.au’s Finance Expert, Sean Callery, says too many Aussies are leaving free money on the table.

“If you’re not checking your savings rate, chances are you’re not getting the best return on your money. In this rate environment, not paying attention could cost you hundreds or thousands a year. Banks adjust their rates regularly, and even more often now that we’re in a rate-cutting cycle, so you should be checking your savings rate every few months,” he says.

“With some savings accounts, you’ll only earn the top rate if you’re meeting certain conditions and if you’re not paying attention, the default base rate could be zero or close to it.”

“Savers got unexpected good news this month with the RBA leaving the cash rate on hold. Now is a good time to review your current rate and account conditions, and consider switching to a more competitive option, so you can be in a better position to weather any future rate cuts.”

Gen Z and Millennials just as unaware as Boomers

The research found that the lack of savings rate awareness spans all generations, with younger Australians no more switched on than their older counterparts.

In fact, 58% of Gen Z and Millennials said they don’t know their current savings rate, almost identical to 57% of Gen X and 56% of Baby Boomers who reported the same.

-- ENDS --

Survey: RBA rate cuts leave most Australians worried about their savings

New research from Money.com.au reveals that a whopping 58% of Australians are worried about the shrinking interest they’re earning on savings accounts since the RBA began cutting rates this year.

Among them, 47% are concerned the reduced interest income will derail their savings goals, while 30% plan to switch to a higher-rate savings account. Meanwhile, 19% say they’ll move their cash elsewhere, such as into shares, and 4% are even considering high-risk options like crypto.

Only 42% of Australians say they’re not worried about RBA rate cuts impacting savings rates.

Money.com.au’s Finance Expert, Sean Callery, says a huge pool of household wealth is at risk of shrinking every time rates are cut.

“Rate cuts are a slow bleed for savers. They lower the interest paid on savings accounts and term deposits, so savers earn less on their money while prices for everyday goods and services keep rising. Over time, that gap steadily erodes the real value of their savings,” he says.

“Make sure to shop around so your savings earn the best market rate available. There are usually no fees to close a savings account and open a new one with another bank, so it costs nothing to move your money for a better rate.”

“For savers who have a home loan, parking your savings in an offset account can make more financial sense. It effectively earns you the same return as your mortgage rate by reducing the interest you pay. So instead of earning money on your savings, which may be taxable, you’re paying less in interest on your home loan. This may result in a better overall position, as mortgage rates tend to be higher than savings rates.”

The biggest losers of the RBA’s rate cuts

Self-funded retirees

Self-funded retirees, who receive no government income support, rely on the returns from their accumulated savings and investments like super, shares and property. Lower savings rates directly cut the earnings they receive from money kept in savings accounts and term deposits.

Pensioners

Rate cuts can also impact older Australians on the Age Pension because their payments are partly based on government ‘deeming rates’, which estimate what their savings should earn. These deeming rates are reviewed only occasionally, so when banks cut the actual interest paid on savings accounts and term deposits (the market rates), the deeming rates can stay higher for some time. This lag means some pensioners may get smaller pension payments than they should, because their lower real interest income isn’t immediately reflected in the rate they are ‘deemed’ to be earning.

Mortgage Expert, Debbie Hays, says some pensioners also still carry a mortgage, and earning less on their savings can create anxiety, even if lower interest rates reduce their loan repayments slightly.

First-home buyers

Debbie says rate cuts typically help first-home buyers who are ready to purchase by boosting borrowing power, but they work against those still saving for a home deposit.

“If those still saving are getting lower returns on their money in the bank, it takes them longer to reach their deposit target, all while property prices continue to climb. Parental help is also affected; when parents’ savings earn less, they have less capacity to give cash to their children to buy a home,” she says.

Small business owners with cash reserves

Many small business operators keep working capital in business savings accounts to cover payroll and tax obligations. Lower deposit rates erode that capital’s earning power and can squeeze cash flow.

-- ENDS --

Survey: 68% of Aussies say all businesses should accept cash despite rise of digital payments

New research from Money.com.au reveals that despite the rise of digital payments, Australians overwhelmingly want the right to pay with cash.

The nationally representative survey of 1,000 Australians found that the majority (68%) — equivalent to 14.8 million people — believe all businesses should be required to accept cash as a payment option.

A further 14% say essential services like supermarkets, pharmacies, and petrol stations should at least continue accepting cash.

However, a similar portion of Australians (13%) say businesses should be free to choose whether to accept cash, while just 5% support a no-cash policy.

Money.com.au’s Finance Expert, Sean Callery, says while digital payments are rising, cash still plays an essential role for millions of Australians.

“Australians are using less cash overall, but they still believe businesses should be required to accept it. Cash remains the most reliable payment method — when the internet is down, the power is out, or there’s a tech glitch, it’s often the only way to pay,“ he says.

“It’s also the only way to dodge debit and credit card surcharges — the most hated fee among Aussies, with 39% ranking it above even ATM withdrawal charges (14%).”

Boomers want cash protected, but Gen Z less so

The survey found the support for cash is highest among older generations. Boomers are the most likely to say all businesses should accept cash (83%), followed by Gen X (71%). Millennials (57%), and Gen Z (49%) are the least likely to say cash should be mandatory.

On the other hand, younger Australians are more likely to say businesses should have the choice to accept or reject cash. Gen Z are the most likely to support this (25%), followed by Millennials (15%), Gen X (12%), and Boomers (7%).

Sean says digital payment systems might be more common, but they don’t suit everyone.

“Digital payments might be the norm these days, but that doesn’t mean they work for everyone. Whether it’s due to age, accessibility, or just personal preference, cash still plays an essential role in the way many Australians pay for goods and services. Keeping cash may be more about ensuring fairness by preserving payment freedom for everyone,” he says.

Federal government moves on cash mandate

The Government has announced plans to mandate cash acceptance for essential purchases, like groceries, fuel and medicines. Some small businesses will be exempt from the mandate. A consultation paper has been released to gather consumer feedback on the proposed changes, with the mandate expected to commence in 2026.

-- ENDS --

Survey: 56% of Aussies don’t oppose higher prices under RBA card fee reforms

New research from Money.com.au reveals that most Australians don’t oppose businesses raising everyday prices to cover lost revenue from card surcharges if the RBA goes ahead with its plan to ban customer surcharges on card payments.

The nationally representative survey of more than 1,000 Australians found that 56% say it would be reasonable for businesses to raise prices to offset card-processing costs, since those would no longer be directly paid by customers under the proposed reforms.

Among them, 35% say price increases are only fair if businesses are transparent about the extra cost, while 21% say any rise should be reasonable and not cross into price gouging.

In contrast, 44% of Australians say businesses shouldn’t raise prices to cover card-payment costs and should absorb those expenses instead.

Money.com.au’s Finance Expert, Sean Callery, says consumers will tolerate some price increases, but only on fair terms.

“Whatever form the RBA’s changes take, businesses will still have to pay banks for payment services. The big question is whether they will wear those costs or build them into higher prices for consumers in place of a card surcharge at checkout. It’s hard to think that restaurants, cafés, pubs, and small shops and businesses would simply absorb those costs when their margins are already so tight,” he says.

“Consumers aren’t against businesses clawing back costs, but they want fairness and transparency. They’re prepared to accept a small, reasonable price increase to their morning coffee or weekend dinner, but they don’t want to be taken by surprise or stung with price hikes that go beyond a business’s operating costs, which would go against the spirit of the RBA’s reforms.”

RBA card fee reforms could save households $1.2 billion a year — but businesses still face merchant fees

Under the RBA’s proposed changes, consumers would no longer pay debit or credit card surcharges at checkouts. It would save Australians an estimated $1.2 billion a year.

However, businesses will still have to pay merchant fees to accept card payments. While the RBA is proposing to reduce interchange fees, these are only one part of that cost, alongside scheme fees and the provider’s margin. Cutting interchange fees won’t necessarily lower merchant fees unless banks pass the savings on to businesses.

For businesses that currently add a card surcharge, a 1.5% fee that is passed on to customers would become a 1.5% fee they have to absorb or bake into everyday prices to recoup their costs.

The RBA will issue its final decision on the reforms by the end of the year.

Younger Australians less opposed to businesses passing on card costs to customers

The survey found that younger Australians are less opposed to businesses passing on card-payment costs. Some 68% of Millennials and 65% of Gen Z say it’s fair provided it’s transparent and reasonable, compared with 53% of Gen X and just 45% of Baby Boomers.

At the other end of the spectrum, older Australians are the most likely to reject higher prices. The research shows 55% of Baby Boomers and 46% of Gen X say it’s not fair for businesses to pass on card-payment costs, compared with 35% of Gen Z and 32% of Millennials.

-- ENDS --

Survey: 73% of Australians cling to physical cards as mobile wallet use surges

New research from Money.com.au reveals that the majority of Australians (73%) don’t want to let go of their physical debit or credit cards, despite the growing popularity of mobile wallets like Apple Pay and Google Pay.

Of those who prefer to keep using physical cards, 39% say they like using them at checkouts, while 34% say they might go fully digital, but still want a physical card as backup.

In comparison, the nationally representative survey found that nearly a quarter of Australians (24%) use a mobile wallet for all their purchases. Only 3% still pay for goods and services with cash.

Money.com.au’s Finance Expert, Sean Callery, says the convenience of mobile wallets doesn’t outweigh the comfort of having a physical card in reserve for most people.

“Despite all the hype, Aussies aren’t ready to give up their cards just yet. It’s partly habit and trust, but also about having a backup when your phone dies or the tap doesn’t work at checkout,” he says.

“People know how physical cards work, and what to do if one is lost or stolen. But with mobile wallets, there’s still uncertainty around things like fraud or data breaches, and how to fix it if something goes wrong.”

“Mobile wallets are super convenient, but they still feel a bit intangible, especially for older Australians who are more hesitant to trust digital payments over traditional methods. Even younger Aussies prefer to carry a card just in case. That shows there’s still a trust gap when it comes to going fully digital.”

Older Aussies less likely to break up with their physical cards

When it comes to holding on to physical cards, older generations are leading the charge. The survey found that 84% of Baby Boomers and 75% of Gen X won’t give up their debit or credit cards, despite mobile wallets becoming more widespread.

Even among younger Australians, many are still hesitant — 66% of Millennials and 55% of Gen Z say they’re not ready to go fully digital either.

However, 43% of Gen Z and 32% of Millennials say they use a mobile wallet for all their purchases — compared to just 23% of Gen X and only 10% of Baby Boomers.

Mobile wallet transactions make up 45% of all card payments in Australia

According to RBA retail payments data, Australians have made 2.59 billion mobile wallet transactions so far in 2025, worth a total $110.06 billion. Mobile wallet use now accounts for around 45% of all card transactions in Australia — up from 39% in 2024.

Based on current growth trends, mobile wallets could account for all retail card payments by 2032 at the earliest, according to Money.com.au analysis.

-- ENDS --

Analysis: Mobile wallets could replace bank cards within 7 years

Australia could do away with bank cards within seven years — and rely solely on mobile wallets if their current trend of growth continues, according to new estimates compiled by Money.com.au.

Reserve Bank of Australia (RBA) data shows the share of mobile wallet transactions rose from 11% to 35% in just three years from 2020 to 2023. Projections indicate that at this rate, mobile wallets could account for all retail card payments by 2032 at the earliest.

Money.com.au's research and data expert, Peter Drennan, says Australians are embracing mobile wallets at an unprecedented rate.

“We’re seeing a glimpse into a future where your phone is your entire wallet and all transactions are made via a mobile phone, smartwatch or other device. Unlike physical cards, which can be forgotten, lost, or stolen, e-wallets provide a more convenient alternative for everyday payments,” he says.

According to new RBA data, there were over 500 million transactions on mobile wallets in the month of October 2024 alone, totalling just over $20 billion. It shows mobile wallet usage at 37% which indicates the rate of adoption is slowing.

Peter says mobile wallet providers like Apple Pay and Google Pay will need to come up with strategies to keep adoption speed on track.

“Otherwise, they will struggle to convert new users, particularly older generations who may be less tech-savvy or hesitant to trust digital payment systems over traditional cards. Getting past hurdles like familiarity, security worries, and making mobile wallets easy for older generations to use will be key to keeping the momentum going,” he says.

Mobile wallet use growing 43 times faster than debit cards

Over the same three-year period, debit card use also grew by 11%. In comparison, mobile wallet usage surged by a staggering 475%, growing roughly 43 times faster. The number of transactions made using physical cards increased from 563 million to 625 million, while mobile wallet transactions jumped from 70 million to 400 million.

Money.com.au’s finance expert, Sean Callery, says there’s a growing preference for mobile wallets, even as overall debit card transactions continue to rise.

“Mobile wallets aren’t just about convenience anymore, they’re quickly becoming the go-to way to pay. Plus, with features like biometric authentication, they give people a real sense of control and safety, which is so important with data theft being such a constant worry," he says.

“Physical cards aren’t obsolete yet, but it’s clear they're losing ground as more people turn to the convenience and security of mobile wallets for everyday transactions.”

Aussies spend less on mobile wallets

There's a noticeable difference in the size of transactions made via mobile wallets and physical cards. The average transaction value for mobile wallets currently stands at $40, significantly lower than the $84 average for non-mobile wallet transactions.

Peter says this discrepancy may hinder broader adoption, as consumers still use physical cards for transactions at smaller merchants, for large purchases or financing, and for booking travel or accommodation where a card is needed for verification.

“Younger generations are more inclined to set up e-wallets and use them for small transactions, which likely results in a smaller average spend. I’d also assume that people still tend to reach for a physical card when making larger transactions,” says Peter.

-- ENDS --

Analysis: Australians could pay $123 million in public holiday surcharges in April

Australians could be hit with $123.2 million in public holiday surcharges in April 2025 while dining or drinking out, according to new analysis by Money.com.au.

That’s roughly $24.6 million in surcharges per public holiday across Good Friday, Easter Saturday (in some states), Easter Sunday, Easter Monday, and Anzac Day.

Generally, April is one of the most expensive months of the year for eating out because it has the most public holidays. Turnover for cafés, restaurants, and takeaway food services is estimated to hit $5.3 billion this April.

Money.com.au’s Finance Expert, Sean Callery, says public holiday surcharges can feel like an extra tax on dining out during holidays.

“Consumers should factor public holiday surcharges into their budget because they add up quickly. They usually range from 10% to 15%, but some venues charge as much as 20%. That means a $100 meal could end up costing you an extra $10 to $20, depending on where you go,” he says.

“Public holiday surcharges can lead to bill shock, so it’s up to you to check the fees, which should be clearly displayed on the menu or elsewhere, before you order.”

In April 2023 (when Easter fell early in the month), Australians paid an estimated $120.8 million in public holiday surcharges, and $104.9 million in April 2022.

Public holiday surcharge estimates are based on ABS Retail Trade data for cafés, restaurants, and takeaway food services — the industries where surcharges are most common. The fees are assumed to account for around 15% of turnover on public holidays.

Why the surcharge on public holidays?

Businesses charge public holiday surcharges to cover higher operating costs, like penalty rates for staff working on those days. The surcharge typically ranges from 10% to 15% of the total bill (but could be more) and must be clearly displayed on menus. If the menu does not list prices, information about these surcharges must be displayed in some other prominent way, according to the ACCC.

There’s no cap on what businesses can charge. Venues are free to set their own rates.

Public holiday surcharge hated most by Boomers, Gen Z and Victorians

Money.com.au’s research shows that 15% of Australians — equivalent to 3.2 million people — rank public holiday surcharges as their most hated fee.

Among generations, Boomers (19%) were the most likely to say they dread public holiday surcharges, followed by Gen Z (18%). Gen X were the least bothered at 12%, followed by Millennials (14%).

Across states, Victorians (18%) and Western Australians (15%) were the most likely to list public holiday surcharges as their most hated fee, followed by South Australians (14%), and Queenslanders and New South Wales residents (both 13%).

-- ENDS --

Survey: 1 in 5 Aussies say debit card surcharges are their most hated fee

One in five Aussies (21%) say debit card surcharges are their most hated fee, according to a new survey by Money.com.au. This refers to the surcharge consumers pay on card payments in-store or online.

It comes amidst the federal government’s plan to ban surcharges on debit transactions by 2026.

It’s Gen Z — despite being more familiar with cashless payments — who are most frustrated by card surcharges, with a quarter (25%) listing them as the fee they resent most. Following closely are Gen X (22%), Millennials (20%), and Boomers (19%).

“Younger generations use debit cards more than any other payment method, so it makes sense that the fees associated with them would be a bigger issue for what they use most,” according to Peter Drennan, Money.com.au's Research & Data Expert.

“At last count, the RBA found that 7.5% of payments had a surcharge, but it has grown significantly since then. It’s likely much higher now as more and more retailers adopt surcharging. So, surcharges are more present and more of a concern than ever before,” he says.

Credit card fees second biggest ‘grudge fees’

Second on the list of ‘grudge fees’ are credit card fees (18%), including annual fees and foreign transaction fees, according to Money.com.au’s survey. Boomers were the most likely to list credit card fees as their top annoyance, followed by Gen X (18%), Millennials (18%), and Gen Z (12%).

“Boomers tend to use credit cards more than debit cards, which is potentially why credit card fees are a bigger issue for them compared to younger generations, even though they may be more experienced in using credit cards to stack rewards and get their money’s worth,” says Peter.

Other commonly disliked fees include public holiday surcharges (15%), ATM withdrawal fees (14%), delivery fees for online shopping (11%) and booking fees (9%), like those charged for events or flights.

Banning debit card fees: A win for consumers or a blow to businesses?

The Australian government’s plan to ban debit and credit card surcharges is still pending a review by the RBA. It would save Australians an estimated $1.2 billion a year.

Money.com.au’s Finance Expert, Sean Callery, says Aussies don’t want to be charged extra fees for the privilege of using their money.

“At a time when every dollar counts, it’s no surprise that card surcharges are pretty unpopular with consumers. With more businesses moving away from accepting cash, it’s becoming harder and harder to avoid these card surcharges altogether,” he says.

-- ENDS --

Media/journalist enquiries:

Need a data breakdown by state, age or income — or have an idea for a consumer question? Contact our Head of PR: Megan Birot at megan@money.com.au.

Our expert banking commentator

Sean Callery, Editor

Sean Callery is Money.com.au's Editor. He's an experienced author and editor with expertise in finance, insurance, and investment topics. He leads Money.com.au’s editorial team and manages content on site across all verticals. Sean is also a spokesperson for all things personal finance and is regularly quoted as a finance expert by Australia's leading media outlets. He is qualified with a Certificate IV in Finance and Mortgage Broking.