Health Insurance research & insights

Money.com.au conducts regular consumer surveys and in-depth data analysis to uncover how Australians purchase, manage and value their health insurance.

Research is compiled by our experienced PR & Editorial team. Updated 7 Jul 2026.

Below, you’ll find our latest Money.com.au health insurance research, ordered from most recent to least. It uncovers Australians' attitudes towards private health insurance, how they use and manage their cover, what they value most in a policy, and where the biggest gaps in understanding lie.

All surveys are independently commissioned and carried out by a third-party research agency. Each study is nationally representative by age, gender and location.

Our research is frequently featured across major news outlets and aims to empower Australians to make informed decisions about their health cover – and to provide journalists and policymakers with clear, data-driven insights.

If you use this information, please include a link to the page you’re currently on: https://www.money.com.au/health-insurance/research-insights

Want to see more Money.com.au research and insights? Add us as a preferred source in Google Search.

2026 published research

“It feels un-Australian": 1 in 3 retirees could downgrade or ditch private health cover if rebates are cuts

New Money.com.au research reveals legislation to reduce private health insurance rebates for older Australians could trigger a significant retreat from private cover among retirees — 34% of Australians aged over 65 say they will either cancel their policy or downgrade to a lower level of cover.

Specifically, 18% said they would be forced to cancel their private health insurance altogether if rebates were reduced. Meanwhile, 16% would switch to a lower-tier policy with fewer benefits.

From 1 April 2027, Australians aged 65–69 earning less than $101,000 as a single or $202,000 as a family would see their private health insurance rebate reduced from 28% to 24%. Australians aged 70 and over in the same income brackets would see a larger cut, with their rebate falling from 32% to 24%.

This would bring the rebate for older Australians into line with the rate available to younger Australians on the same income.

The proposed changes require amendments to the Private Health Insurance Act 2007 and must pass Parliament before they can take effect. If approved, around 3 million Australians aged 65 and over would be impacted. Despite the proposed rebate cuts, the majority of Australians aged 65 and over (57%) said they would keep their current level of cover and absorb the higher premium costs, and 9% will increase the excess on their existing cover to reduce premiums.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says reducing private health insurance rebates risks pricing older Australians out of cover at a time when healthcare affordability is already under pressure.

"Slashing private health insurance rebates for older Australians who have worked, contributed to the health system through their taxes their whole lives and done the right thing by maintaining private cover feels like a step in the wrong direction," he says.

"It's also undoing decades of policy designed to keep older Australians in the private health system, and doing so at a time when many retirees on fixed incomes are already being forced to make difficult choices about everyday essentials. For many seniors, there simply isn't any more room in the budget to absorb higher premiums, meaning some will be forced to reduce their cover or cancel it all altogether. Frankly, it feels un-Australian."

"The Government says reducing the rebates is about improving intergenerational equity in the private health system, but all it's really doing is shifting costs onto taxpayers. If more older Australians are forced into the public system, we'll all end up paying for it through higher taxes and greater pressure on public hospitals."

How much more could older Australians pay for private health insurance if rebates are cut?

Any changes to private health insurance rebates for seniors would coincide with the annual 2027 premium rise.

Money.com.au’s analysis shows a single policyholder aged 65–69 earning under $101,000 and holding a silver hospital policy could pay around $179 more per year if their rebate is reduced from 28% to 24%.

A single policyholder aged 70 and over in the same income bracket and holding the same silver hospital policy could pay around $358 more per year as their rebate falls from 32% to 24%.

Note: These estimates are based on the average annual premium on silver hospital policies in Money.com.au's database ($4,469) and assume a 3-4% premium increase in 2027. Actual costs will vary depending on the policy, insurer and premium increase approved for that year.

-- ENDS --

‘Dead money’: Aussies warned to act before July 1 or face Medicare Levy Surcharge sting

Experts are warning Australians earning above the Medicare Levy Surcharge (MLS) income threshold to get eligible private hospital cover in place before July 1 if they want to avoid the surcharge next financial year.

New research from Money.com.au reveals 31% of Australians who received a pay rise in the last 12 months had their income pushed above the MLS income threshold — currently $101,001 for singles and $202,001 for couples and families.

Those who didn’t have eligible private hospital cover for the full financial year will face an additional tax charge of between 1% and 1.5% on at least a portion of their income when they lodge their 2025–26 tax return after June 30. That’s on top of the 2% Medicare Levy.

The minimum surcharge is $1,010 for singles and $2,020 for couples and families who didn’t hold eligible private hospital cover for the full financial year. Those who held cover for part of the year may pay less, as the MLS is applied pro-rata.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says Australians who’ve recently moved above the threshold should weigh up the cost of cover against the cost of the surcharge.

"For many Australians, it's already too late to avoid the MLS for this financial year if they didn't have eligible hospital cover in place. The opportunity now is to get cover before July 1 and maintain it throughout the next financial year, so you don't get caught out again at tax time," he says.

"At a minimum, you need to take out a basic hospital policy to avoid paying the MLS. In many cases, the cost of cover is similar to — or even less than — what you'd otherwise pay in additional tax. The difference is that with health insurance, you’re paying towards cover and services you may actually use, whereas the MLS is essentially dead money.”

"For example, some of the cheapest eligible basic hospital policies start from around $1,000 a year for singles — less than the $1,066 Medicare Levy Surcharge payable by someone earning the average annual wage of $106,657 who doesn't have eligible cover. It’s definitely worth comparing your cover options before July 1 and running the numbers.”

“The big caveat is that entry-level hospital policies often provide limited benefits, so it’s generally worth considering at least a Bronze policy combined with extras. This gives you access to services you're more likely to use throughout the year, like dental, optical and physiotherapy.”

The cost of paying the MLS versus taking out eligible hospital cover

For someone earning the average wage, the cost of eligible hospital cover can be lower than the surcharge itself.

To completely avoid paying the Medicare Levy Surcharge, you must take out eligible private hospital cover with a registered health fund before July 1 and maintain it for the full financial year. For singles, the policy excess must be $750 or less, while couples and families must have an excess of $1,500 or less. Extras-only or ambulance-only cover doesn’t qualify for an MLS exemption.

The MLS thresholds will increase to $105,001 for singles and $210,001 for couples from 1 July 2026. The thresholds are adjusted annually to reflect inflation and wage growth.

Millennials most likely to be caught by MLS threshold creep

The research found that younger working Australians are disproportionately feeling the impact of threshold creep, with Millennials (49%) and Gen Z (39%) the most likely to report crossing the MLS income threshold after receiving a pay rise in the last 12 months. Gen X followed at 27% and Baby Boomers at just 7%.

-- ENDS --

3.37 million Australians use BNPL or payment plans to cover medical gap fees

New research from Money.com.au reveals millions of Australians with private health cover are financing out-of-pocket medical costs through Buy Now, Pay Later (BNPL) services and provider payment plans.

The nationally representative survey found that 22% of Australians with private health insurance — equivalent to 3.37 million people — have used BNPL or a provider payment plan to cover healthcare gap fees for services like dental work, physio, specialist appointments or surgery.

Among this group, nearly two-thirds (63%) used a BNPL provider like Afterpay, Zip Pay or Humm to spread out healthcare gap fees, while 50% used a payment plan offered directly by their medical or service provider.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says rising premiums and healthcare costs are making out-of-pocket expenses harder for many Australians to absorb.

“With health insurance premiums continuing to rise, many households simply have less spare cash to cover out-of-pocket medical expenses, which are also becoming more expensive. As a result, more people are turning to payment plans or BNPL services to manage some gap fees they can’t comfortably afford upfront,” he says.

Health insurance premiums rose by an average of 4.41% last month — the steepest increase in a decade. For families with a combined hospital and extras policy, that equates to roughly $216 more per year in premiums.

Whitelaw says insurers and healthcare providers are aware of the affordability pressures Australians are facing.

“That’s why we’re seeing more payment plan options emerge across the sector. More insurers and medical service providers are offering financing solutions or structured payment plans to help patients spread the cost of gap payments over time,” he says.

“However, it doesn’t detract from the fact that when people are financing dental treatment, physio or medical procedures, it’s a sign the system isn’t adequately catering to the financial realities many Australians face when they access healthcare.”

“One way Australians can reduce out-of-pocket costs is by choosing specialists and providers who participate in their health fund’s GapCover or known-gap scheme. This essentially caps known-gap fees at $500 per doctor or eliminates them entirely for eligible treatments.”

The survey found that the majority of Australians with private health insurance (74%) have covered their medical gap fees upfront, while 4% say they’ve never paid gap fees or made any claims on their health policy.

Paying later for healthcare: How younger Australians are driving medical BNPL use

Younger Australians with health insurance are more likely to rely on financing options to manage out-of-pocket healthcare expenses, with Gen Z driving the strongest uptake.

More than one in three Gen Z respondents (38%) say they’ve used instalment payment plans for healthcare gap fees, followed by Millennials at 28%. This compares to 22% of Gen X and just 7% of Baby Boomers.

The survey found that Gen Z (67%) and Millennials (65%) were the most frequent users of BNPL services like Afterpay to cover medical gap fees, followed by Gen X at 50%.

Provider-direct payment plans were more commonly used by Millennials (57%) and Gen X (55%), followed by Gen Z (45%), while Baby Boomers were least likely to use this option (20%).

-- ENDS --

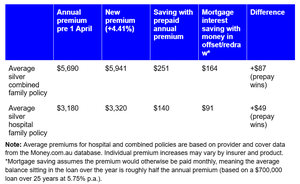

Health insurance vs your mortgage offset/redraw: where your money works harder in 2026

Silver combined family policy

If you prepay your health insurance for the year ahead, you’re saving $251, compared to the $164 you’d save in mortgage interest over the same period by keeping the money in your offset account or redraw. So you’re about $87 better off by prepaying your health insurance for 12 months. That’s because, in reality, you’d be drawing down the money from your mortgage gradually over the year to pay the monthly premiums, so the interest saving gradually decreases.

Silver hospital family policy

Same story here. Prepaying your health insurance for 12 months saves $140, compared to $91 in mortgage interest over the same period, leaving you $49 better off.

Whether you can prepay or not, it’s worth shopping around first. There are some strong offers in the market right now, especially with funds offering weeks free ahead of the April 1 increase.

Top 10 best switch and save offers (as of March 2026)

Full calculations below:

Silver combined family policy

- Annual premium cost: $5,690

- New cost with 4.41% increase: $5,941

- Prepaying health insurance: +$251 benefit

- Average amount sitting in the loan over the year: $5,690 ÷ 2 = $2,845 × 5.75% = $164

- Year 1 mortgage interest saving (under this gradual‑spend setup): +$164 benefit

Silver hospital family policy

- Annual premium cost: $3,180

- New cost with 4.41% increase: $3,320

- Prepaying health insurance: +$140 benefit

- Average amount sitting in the loan over the year: $3,180 ÷ 2 = $1,590 × 5.75% = $91

- Year 1 mortgage interest saving (under this gradual‑spend setup): +$91 benefit

*Note: To compare apples with apples, we should assume your offset balance drops each month as insurance payments are made. That means, on average, only about half of the annual premium sits in the mortgage over the year, so the interest saving is based on roughly half the amount. Under this more realistic cash‑flow assumption, prepaying the combined policy ‘wins’ over the mortgage for the next 12 months.

-- ENDS --

2.7 million Aussies miss their health insurance premium hike notices

Millions of Australians with private health insurance are missing the notice warning them their premiums are about to rise.

New research from Money.com.au reveals 18% of Australians — equivalent to 2.7 million people — admit they always miss their health fund’s premium increase notice, either because they don’t read the message or mistake it for a marketing email.

Most health funds send their premium increase notices this month ahead of the April 1 price changes, when premiums will rise by an average of 4.41% — the steepest increase since 2017.

While health insurers are required to notify members in writing of annual premium increases, there’s no legislated timeframe for when these notices must be sent, only that policyholders are given ‘sufficient time’ to review their cover or consider switching.

However, under the Private Health Insurance Code of Conduct, most health funds commit to giving their members at least 30 days’ notice of any policy price changes.

When do Aussies get their health insurance increase notices?

The nationally representative survey found 38% of Australians receive their premium increase notice more than a month before the change takes effect each April. Meanwhile, 36% receive between two and four weeks’ notice, while 8% say they receive less than two weeks’ warning before their premiums rise.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says Australians rarely know when their premium increase notice will arrive.

“It’s important to keep an eye out for your individual notice, as this will show exactly how much your policy premium will increase in dollar terms. From there, you can see how your increase compares with the industry-wide average rise of 4.41%. These notices are usually sent by email and SMS,” he says.

“Some funds send their notices early, while others may only give a few weeks’ warning. If you’re still waiting for your premium hike letter, it’s worth contacting your health fund now to find out when it will be issued and how much your premium will increase.”

“The more time you have to prepare and shop around, the better off you’ll be. It’s also worth keeping in mind that most health funds have a March 31 deadline for locking in last year’s premium for another 12 months.”

Young Aussies most likely to miss health insurance price rise alerts

Younger Australians are the most likely to miss notifications about their private health insurance premium increases.

The survey found 25% of Gen Z policyholders say they always miss their fund’s premium increase letter, the highest of any generation. This compares with 20% of Gen X, 17% of Millennials and 13% of Baby Boomers.

Estimated annual premium increases after 4.41% rise

For families on a combined hospital and extras policy, the 4.41% increase will add around $216 per year to premiums, based on the current average annual cost of $4,908. Single policyholders will see premiums rise by roughly $144 per year, based on the average annual premium of $3,264 for a combined policy.

-- ENDS --

Health cover shake-up: 46% plan to cut or switch ahead of premium hike

New research from Money.com.au reveals nearly half of Australians (46%) plan to downgrade, switch or cancel their health insurance when premium increases take effect on April 1.

Health insurance premiums will rise by an average of 4.41% — the steepest increase since 2017. However, some health funds will lift premiums by more than the industry average, depending on the product.

The nationally representative survey found 19% of policyholders — equivalent to around 2.9 million Australians — plan to cancel their extras cover, hospital cover, or both, while 18% say they intend to switch to a different health fund this year.

Meanwhile, 13% plan to increase their policy excess, and a further 12% are considering downgrading their cover tier, like moving from Gold to Silver. Respondents could select multiple actions they plan to take in response to the premium hike.

By contrast, the majority of Australians (54%) say they plan to stay on their current policy.

For families on a combined hospital and extras policy, the 4.41% increase will add around $216 per year to premiums, based on the current average annual cost of $4,908. Single policyholders will see premiums rise by roughly $144 per year, based on the average annual premium of $3,264 for a combined policy.

“The real danger is that people cancel their cover”

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says the increase is prompting many households to reassess their cover.

“People are looking at ways to cut costs on their health cover because this premium increase could be the straw that breaks the camel’s back. Some of the largest health funds are implementing increases above the 4.41% industry average, meaning many households will be hit with rises well above what they might expect,” he says.

“Increasing your excess is one of the easiest ways to reduce your premium. Another option is to pay your policy annually before April 1, which can delay the premium increase for another year. Some funds are also offering the option to lock in your current premium for up to 24 months. Not everyone can do this, but it’s worth considering.”

“If you’re downgrading your cover, make sure you understand there’s a trade-off. People often get caught out when they move from Gold to Silver policies and realise they’re no longer covered for common treatments like cataracts or joint replacements.”

“The real danger is that people cancel their cover — particularly hospital insurance — and are left uninsured for major medical expenses, while also facing longer wait times in the public hospital system.”

Younger Australians lead health cover exodus

Younger Australians are the most likely to ditch their health insurance in response to the premium hike. The survey found 30% of Gen Z policyholders plan to cancel their cover, closely followed by Millennials (29%). In contrast, far fewer Gen X (11%) and Baby Boomers (8%) say they intend to cancel.

Switching behaviour is also skewed toward younger cohorts. Almost a quarter of Gen Z policyholders (23%) say they plan to switch health funds this year, compared with 20% of Gen X, 18% of Millennials and 15% of Baby Boomers.

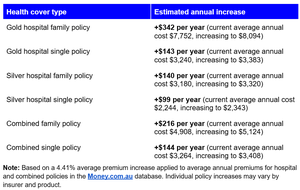

Estimated annual premium increases after 4.41% rise

- Gold hospital family policy +$342 per year (current average annual cost $7,752, increasing to $8,094)

- Gold hospital single policy +$143 per year (current average annual cost $3,240, increasing to $3,383)

- Silver hospital family policy +$140 per year (current average annual cost $3,180, increasing to $3,320)

- Silver hospital single policy +$99 per year (current average annual cost $2,244, increasing to $2,343)

- Combined family policy +$216 per year (current average annual cost $4,908, increasing to $5,124)

- Combined single policy +$144 per year (current average annual cost $3,264, increasing to $3,408)

Note: Based on a 4.41% average premium increase applied to average annual premiums for hospital and combined policies in the Money.com.au database. Individual policy increases may vary by insurer and product. -- ENDS --

Survey: 80% of Australians support private hospital funding reform

New research from Money.com.au reveals eight in 10 Australians with private health insurance (80%) support reforms to private hospital funding.

More than half (53%) favour any model that reduces patient out-of-pocket costs, while 27% support the Federal Government’s proposed Activity-Based Funding (ABF) model, which would pay private hospitals a standard price for treatments based on the type and volume of care provided.

Just 20% say the current system should remain, where private hospitals are funded through a mix of insurer contracts, patient fees and Medicare benefits.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says policyholders support reform in principle but are wary of complex models that fail to deliver clear savings.

“Australians want sustainable funding for private hospital care, but they expect any new funding model to make healthcare more affordable, or at the very least not increase costs for patients. People don’t want reforms that shift Australia closer to a US-style system where private hospital patients pay excessive gap fees,” he says.

Mr Whitelaw warns that without the right safeguards, patients could end up footing a larger hospital bill.

“Most private hospitals are for-profit enterprises, so reform has to balance commercial reality with patient outcomes. If price caps are introduced under an activity-based model, there’s a real risk private hospitals simply recoup costs through higher gap fees or charges elsewhere.”

It comes as health insurance premiums remain under pressure, with modelling of health inflation and historical premium increases suggesting the industry-average rise will be closer to 4% this year.

Generational splits reveal clear differences in attitudes to reform

The research found that Gen X were the strongest backers of the Government’s ABF proposal, with 27% supporting the model.

Baby Boomers were the most supportive of reform in principle, with 64% saying they would back any funding model that reduces gap fees.

By contrast, Gen Z were the strongest supporters of keeping the current system unchanged (46%), followed by Millennials (34%).

What are the Government’s proposed reforms to private hospital funding?

The Federal Government has proposed draft reforms to how private hospitals are paid, using an Activity-Based Funding (ABF) model similar to the system used in public hospitals.

Central to the proposal is the introduction of a Private National Efficient Price (PNEP) — a national benchmark intended to inform pricing and contract negotiations between private hospital operators and insurers.

The framework remains in draft and consultation, with any changes proposed to roll out from July 2026.

-- ENDS --

2025 published research

Survey: Millions of Aussies face December 31 deadline for thousands in unclaimed health insurance extras

Millions of Australians with health insurance risk losing thousands of dollars in unused extras benefits when annual limits expire on December 31.

Most health funds reset their extras benefit limits at the start of the New Year (on January 1), meaning the 15 million Australians with extras or combined health insurance have only weeks left to use their annual allowances for dental, optical, physio and other treatments.

The latest research from Money.com.au reveals two in five Aussies with health insurance (40%) don’t know if they have any unused extras left on their policy.

Meanwhile, 31% used some extras but still have benefits left before they expire, and 15% admit they’ve used none or very little of their annual limits. Only 14% of Australians have used their full entitlements this year.

All extras policies have annual limits — the maximum amount you can claim on a specific service or treatment each year — and once that limit resets, any unused portion is lost. For example, if your dental limit is $1,800 and you’ve only claimed $800 this year, the remaining $1,000 disappears when your policy resets.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says Australians underestimate how much value they lose by not keeping track of their extras annual limits.

“Australians are effectively walking away from thousands of dollars in value every year. Depending on your policy, extras limits can range from $200 to $1,800 for services like general dental. Many people don’t realise those benefits vanish overnight on December 31. It’s a classic ‘use it or lose it’ scenario,” he says.

“If you're due for a visit, use the next few weeks to book a dental clean, renew your glasses or lock in that one last physio appointment before your extras reset. Appointment books fill up quickly in December, so securing those final bookings now can make a big difference.”

“You can check your claims history through your insurer’s app or online member portal. If you’re still unsure, contact your fund directly and they’ll be able to provide your full claims history for the calendar year. Ideally, you want to use as much of the extras benefits you pay for all year through your premiums. And if you consistently underuse your benefits, it may be worth switching to a policy with lower annual limits.”

Older Aussies most unsure about their health insurance extras, but younger Aussies underuse them the most

The survey found that uncertainty is more prevalent among older Australians, with 45% of Baby Boomers unsure whether they have unused extras remaining. The same is true of 41% of Gen X and 27% of Millennials.

“What we see is that older generations tend to claim when something breaks or hurts, not to maximise their extras value. This means they’re less aware of their annual limits,” says Chris.

However, younger Australians are the most likely to have used none or very little of their extras this year, with 19% of Millennials reporting minimal use, compared with 13% of Gen X and 11% of Baby Boomers.

When do health funds reset extras benefits?

The majority of Australian health funds have extras benefits that expire on December 31 and reset on January 1. This includes the ‘Big Five’ of Medibank, Bupa, HCF, HBF and NIB.

Some insurers instead reset their annual limits at the end of the financial year (June 30), with benefits renewing on July 1. A smaller number of health funds offer policies where extras limits reset on the policy anniversary date.

Select funds do offer rollover features, but they’re the exception, not the rule, and only apply to specific services like general dental or optical. Most Australians won’t be able to carry their benefits into the New Year.

-- ENDS --

Analysis: Health insurance premiums to climb back toward 4% in 2026 — adding up to $196 a year for families

New analysis from Money.com.au shows next year’s private health insurance premium increase could sit between 3.9% and 4.4%. (See chart below).

Data shows that although premium increases have sat below health inflation since 2021, the gap has been steadily closing. If health inflation stays near the 4% mark this year, the 2026 premium hike could fall in line with, or even surpass health price inflation.

A 3.9%–4.4% premium rise would see singles on a combined hospital and extras policy pay an extra $127–$144 a year, while families would face an additional $191–$216 annually. These estimates are based on the average combined single policy costing $3,264 a year and the average combined family policy costing $4,908 a year.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says the return of stronger premium increases will be felt by millions of policyholders.

“What we’re seeing is a reset. Premium increases stayed unusually low for years, and 2026 may be the year they return to a more ‘normal’, but still painful, growth cycle. There’s no doubt that a premium increase of around 4% would be a shock for many policyholders, especially after a few years of softer rises,” he says.

“If you’re a policyholder, now’s the time to look at your policy and inclusions, and reassess whether you’re getting value for money as premiums rise. In my experience, there’s almost always a cheaper or better policy available when you take the time to shop around.”

The Minister has the final say on the industry-average premium increase, which is announced ahead of the 1 April adjustment each year.

While the Government approves a single industry-wide average, individual insurers can apply higher or lower increases, meaning some Australians may see rises well above the headline figure, while others may face smaller adjustments.

-- ENDS --

Survey: Australians hold their health cover for a decade, with 46% never switching funds

New research from Money.com.au reveals that Australians with private health insurance have held their cover for an average of 10 years, yet almost half (46%) have never switched health funds.

The research found a third of policyholders (33%) have switched health insurance only once since first taking out their cover, while 16% have switched two or three times. Just 5% say they’ve switched four or more times since being insured.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says Australians aren’t shopping around regularly enough to get better value from their health cover.

�“Premiums rise annually, yet many Australians continue with the same fund or cover tier year after year. As a result, they’re often paying too much for their policy or for cover that no longer suits their lifestage, and in many cases, both. For example, we’ve seen instances where policyholders were still paying for pregnancy benefits well after they’d finished having children,” he says.

“In many ways, your health is your biggest asset, so you should treat health insurance like any other financial product. You should be comparing policies every 12 months to make sure you’re still getting a competitive deal on your current cover or switch to a health fund that will give you one.”

Younger Australians the least likely to switch health funds

Gen Z are the most likely to have never switched health funds, with 58% saying they’ve stayed with the same provider since taking out their policy, though they’ve only held cover for an average of six years. In comparison, 48% of Millennials haven’t switched funds after an average of seven years of cover, while 44% of Gen X remain with the same fund after around 11 years. Baby Boomers are the most seasoned policyholders, holding cover for an average of 13 years, with 42% saying they’ve never switched.

“It’s expected that older Australians have held their health cover for longer, but what’s concerning is how few review or switch their policy as their circumstances change. Your cover should evolve with your life — whether that’s starting a family, retiring, or managing new health needs,” says Chris.

-- ENDS --

Survey: 45% of Australians who use mental health services have private health insurance

New research from Money.com.au reveals the types of insurance Australians use most frequently — and surprisingly, it’s not the ones protecting their biggest assets.

Gen X (51%) and Millennials (48%) were the most likely to rely on private health cover for mental health care, compared with 44% of Baby Boomers and just 32% of Gen Z.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says there is rising demand for mental health care and growing interest in how insurance can help meet it.

“We’re seeing a rise in inquiries, particularly about which levels of extras cover offer benefits for mental health services like psychology, counselling and other therapies. It’s a sign that Australians increasingly see mental health as part of everyday wellbeing, not just something to address in a crisis,” he says.

“Younger Australians are often on basic extras or hospital policies to keep premiums affordable, but these policies typically don’t include benefits for mental health services. Yet, they’re the group most likely to need flexible mental health support while juggling study, work and life changes.”

“The research also found that 55% of Australians who used a mental health service in the past 12 months didn’t have private health insurance, which could be putting pressure on public mental health services and further extending wait times for patients.”

According to APRA data, the number of psychology and group-therapy services provided outside hospitals to Australians with private health insurance has nearly doubled since 2020.

One in five Australians avoid mental health care due to cost

Among Australians who didn’t access mental health services at all in the past year, one in five (20%) said cost was the main barrier, while 80% said they didn’t need care.

Gen Z were the most likely to say cost kept them from seeking mental health services, with 35% citing it as a barrier, well above Millennials (24%), Gen X (29%) and Baby Boomers (13%).

-- ENDS --

Survey reveals most Australians rely on customer reviews when choosing a health insurer

New research by Money.com.au reveals more than half of Australians with private health insurance (59%) check customer reviews before choosing or switching to a health fund.

Among them, a quarter of policyholders (25%) say they always check customer reviews before signing up with any new health insurer, while a third (34%) only research customer feedback if they haven’t heard of the fund before.

How important is customer feedback when choosing a health fund?

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says customer reviews give real insight into members’ experiences with claims, service and value for money.

“On paper, two health funds can look almost identical in price and cover. Customer reviews give you a glimpse of how a fund performs when it comes time to make a claim. Do they pay claims quickly, treat members fairly, or leave you stuck in red tape, as we know happens with some health funds,” he says.

“These are areas that can make a big difference when you actually need to use your cover, which is on average twice a year for hospital cover and five times for extras. We’ve seen customers choose a health fund with slightly higher premiums because reviews showed claims were processed faster and service was more reliable than other funds.”

“This trend is catching on. Over the years, we’ve seen health insurers like AIA Health Insurance, RT Health and Phoenix Health Fund promote their high customer ratings in advertising because they know Australians are paying attention. Positive reviews and strong satisfaction scores have become a competitive edge in the health insurance space.”

The survey found that one in four Australians with private health insurance (25%) stick with their fund out of habit, while 17% rely on comparison sites or word of mouth when choosing a fund.

Young Aussies lead the way in checking health fund reviews

When it comes to choosing a health fund, younger Australians are far more likely to do their homework. The survey found that three-quarters of Millennials (75%) and 70% of Gen Z check customer reviews before signing up or switching health cover. By contrast, review-checking drops to 62% for Gen X and just 37% for Baby Boomers.

In contrast, older Australians are more likely to turn to word of mouth or comparison sites rather than real customer feedback. The survey found that one in five Gen X (20%) and 19% of Baby Boomers rely on these sources when choosing a health fund, compared with just 14% of Millennials and 11% of Gen Z.

-- ENDS --

Survey: 17% of Australians have increased their health insurance excess for cheaper cover

New research from Money.com.au reveals that 17% of Australians with private health insurance — equivalent to 2.4 million people — have increased their excess in the past year to reduce their premiums.

In comparison, the nationally representative survey found that the majority of health insurance policyholders (72%) have kept their excess the same. Meanwhile, 10% of Aussies with private health cover didn’t know they could request to change their excess.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says Australians need to weigh up the trade-off between premium savings and potential out-of-pocket costs when deciding whether to raise their excess.

“If you’re looking to reduce your health insurance costs, the first port of call is to increase your excess. It’s the quickest way to bring down your monthly premium without downgrading or bumping off your cover altogether,” he says.

“Run a cost benefit analysis before changing your excess. Consider how much you use your cover, how many people are on the policy, and the types of benefits you’re likely to claim. For young singles who rarely go to hospital, a higher excess can be a no-brainer. For families with children who may be in and out of hospital or the dentist more often, a higher excess could mean paying more out of pocket when you claim. The savings on premiums may not stack up.”

How much can you save on premiums by increasing your health cover excess?

For a single policy, the average monthly premium with a $250 excess is $350. Lifting the excess to $500 reduces the monthly premium to $290 — saving $60 a month ($720 a year). A $750 excess brings it down further to $262, saving $88 a month ($1,056 a year) compared with a $250 excess.

For a family policy, the average monthly premium with a $250 excess is $438. Increasing the excess to $500 reduces the monthly premium to $384 — saving $54 a month ($648 a year). With a $750 excess, premiums drop to $371, saving $67 a month ($804 a year) compared with a $250 excess.

Gen Z lead the way in cutting health insurance costs by raising their excess

The survey found that Gen Z (30%) were the most likely of any generation to increase their health insurance excess to reduce premiums. They were followed by Millennials (21%), Gen X (14%), and Baby Boomers (9%).

Meanwhile, Gen X were the most likely to have kept their excess the same (79%), closely followed by Baby Boomers (78%), Millennials (70%), and Gen Z (57%).

-- ENDS --

Survey: Bank of Mum and Dad expands into insurance: 48% of parents pay adult children’s private health cover

New research by Money.com.au reveals that 48% of parents with adult children on their family health insurance pay the full premium without asking for a contribution.

Meanwhile, 30% of parents say their adult children chip in some money toward the family policy. Only 22% say their adult dependants cover the entire cost of their portion of the family policy.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says there’s a trend of young Australians staying on their parents’ private health cover well into their twenties.

"The Bank of Mum and Dad is paying to keep them insured, which can save young adults money in the short term. The alternative is that they would forfeit cover entirely, as it can be cost-prohibitive for them to take out their own policy if they’re on a low income or just starting their career,” he says.

“But, once those adult children have a steady income, it’s time to have the conversation about contributing, even partially, to the family policy. They should also consider taking out their own cover if they earn above the Medicare Levy Surcharge threshold of $101,000 for singles, otherwise they’ll pay the surcharge through their tax.”

Most health funds allow adult dependants aged 21 to 31 to be added to a family policy, although this typically increases premiums. Adult dependants who are studying may be covered for free if they’re not married, living with a partner, or in a de facto relationship.

Adult dependants drive up health insurance costs by 25%

The average cost of a family policy with child dependants (under 21) is $4,808 per year (before any government discounts or rebates), based on Money.com.au’s analysis of extras-only, hospital-only and combined policies.

With an adult dependant (over 21 and not studying), the average cost of a family policy jumps to $6,016 — around 25% higher.

Gen Z most likely to let parents pay full health cover bill

The survey found that Gen Z were the most likely to let their parents pay the full cost of the family cover without contributing to their share (29%), followed by Millennials at 26%.

Among Gen Z, 45% contribute partially to the cost of being on their parents’ family cover, while 27% pay their full share. For Millennials, 32% contribute partially to the cost of being on their parents’ family cover, while 42% cover their share in full.

-- ENDS --

Survey: Half of Aussies miss out on health insurance benefits by staying with current dentist

New research from Money.com.au reveals that nearly half of Australians with extras cover (49%) stay loyal to their dentist — even if it means missing out on no-gap dental benefits available to them.

The nationally representative survey found that only a quarter of extras insurance policyholders (25%) have switched to a no-gap dentist to avoid out-of-pocket fees. Meanwhile, 13% of Aussies said their policy doesn’t include no-gap dental, and 12% don’t know whether their policy includes it.

No-gap dental is a feature of many extras policies that allows policyholders to access fully covered preventative dental treatments — like check-ups, scale and cleans — at select providers with no out-of-pocket costs.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says Australians are paying more for dental treatment than they need to.

“Dental is the most-used extras benefit, but it also has the highest out-of-pocket costs of any general treatment, with patients collectively paying around $800 million in gap fees so far this year. It’s surprising that so many Australians still choose to pay out of pocket, whether out of loyalty to their dentist or simple complacency,” he says.

“No-gap dental is becoming standard on many mid-tier and comprehensive extras policies, but it usually means going to a participating provider. Some of these policies even include two free check-ups per financial year, so if your extras cover doesn’t include no-gap dental, you could be leaving money on the table.”

How much you could save with no-gap dental

According to the latest APRA statistics, the average fee for a dental service for patients with private health insurance is $132.74, but health funds only cover $70.35 on average — leaving insured patients to pay a gap of $62.39 per visit.

So, if you visit the dentist twice a year, you could potentially save $124.78 annually by using a no-gap dental provider.

For a family of four, that adds up to $499.12 in potential yearly savings.

Which generation is missing out on no-gap dental savings?

The survey found that Baby Boomers were the most likely to stick with their usual dentist despite potential out-of-pocket costs (56%), followed by Gen Z (49%) and Gen X (47%). Millennials were the least likely to do so, at just 45%.

Gen Z were the most likely generation to be unsure whether their extras policy includes no-gap dental (17%), while Baby Boomers were the most likely to say their policy doesn’t include it (also 17%).

-- ENDS --

Survey: Health insurance delivers the most savings overall, survey reveals

New research from Money.com.au reveals Australians rank health insurance as the type of cover that saves them the most money overall — more than any other form of insurance.

The nationally representative survey found that one in five Aussies (20%) ranked extras cover as offering the best return on investment of all insurance types, followed by hospital insurance at 19%.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says there’s a shift in how Australians view the practicality of their health cover.

“Australians are placing increasing value on the day-to-day savings extras policies offer because you’re generally more likely to claim on dental, physio, optical and other allied health services than you are on hospital treatments,” he says.

“On average, extras policyholders make around five claims per year, while those with hospital cover average two claims annually. It highlights the importance of choosing a policy that matches your actual usage. Many Australians could be saving more by reviewing what benefits they’re eligible for and whether they’re making full use of them.”

Meanwhile, only 10% of Australians surveyed said car insurance and life/income protection insurance saved them the most money, while 7% said the same about travel insurance. Home and contents insurance ranked lowest, with just 4% of Aussies saying it’s saved them the most money.

Which insurance offers Aussies the most peace of mind?

When Australians were asked which types of insurance give them the most peace of mind, home and contents (88%), life insurance (80%), and travel insurance (79%) ranked highest.

Money.com.au’s Finance Expert, Sean Callery, says some Australians view value through usage, while others see it through peace of mind.

“With insurance types like car, home, life or travel, the goal is to have them and never need to use them. They may not feel useful day-to-day, but they’re crucial in high-risk or emergency situations,” he says.

“It shows that while these policies might not deliver a financial return through regular use — like extras cover does — they offer reassurance and the potential for critical support when it really matters.”

-- ENDS --

Survey: 1 in 4 families avoid using hospital insurance due to gap fees, survey finds

New research from Money.com.au reveals families are the most likely to avoid using their private hospital insurance due to high out-of-pocket costs and the least likely to use it when they need care.

The survey found that nearly one in four families on a hospital policy (23%) have avoided using their cover because gap fees were too expensive — the highest of any policy type. This compares to 17% of couples and 15% of singles who did the same.

Family policyholders were also the least likely to use their cover when needed. Just 43% follow through with a claim when they need treatment, compared to 44% of singles and 64% of couples.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says families are often disproportionately affected by rising gap fees.

“Families typically have more people on their policy and as a result, more opportunities for hospital claims, whether it’s childbirth, tonsil removals, or sporting injuries. That means more exposure to gap fees, and higher out-of-pocket costs over time compared to singles or couples with cover,” he says.

“There’s a real risk that families will delay or avoid essential treatment just to dodge bill shock, which completely defeats the purpose of having hospital insurance in the first place. But there are ways to reduce gap fees if you understand how the system works, including taking advantage of no-gap schemes and providers.”

Singles most likely to avoid hospital claims due to confusion

The survey found that singles (20%) were the most likely to avoid claiming on their hospital insurance because they weren’t sure what was covered and didn’t want to be hit with unexpected costs. That’s compared to just 12% of family policyholders and 9% of couples.

Meanwhile, 22% of both singles and families said they’ve never needed to make a hospital claim, compared to just 10% of couples.

How to reduce out-of-pocket costs for families with hospital cover

- Choose no-gap or known-gap doctors and hospitals Ask your insurer for a list of participating hospitals and doctors that charge no-gap or known-gap fees. Sticking to these providers can help you limit or avoid out-of-pocket costs for common procedures your family may need as it grows and changes. For example, dental surgery under general anaesthetic, grommet insertion, or tonsil removal.

- Use your fund’s agreement hospitals Each health fund has a list of hospitals it has negotiated rates with. Booking into these hospitals helps reduce or cap hospital-related out-of-pocket expenses for your family. You can find out which hospitals your insurer has agreements with by visiting the PrivateHealth.gov.au website.

- Call your insurer before booking any procedure A quick call to your insurer can clarify what’s covered. This is especially helpful when your child needs surgery or you're planning for maternity care. They can flag any gaps in your coverage and suggest alternative cover options.

- Get a full written estimate before treatment Always ask for a written breakdown of fees from every provider involved, including the surgeon, anaesthetist, and specialist. With multiple appointments and family members on the same policy, knowing the full cost upfront helps you plan ahead — especially if your family makes several hospital claims each year.

- Understand your annual limits and excess Make sure you know how your family excess works. Some funds charge per person, others per policy. Some health insurers waive the excess for children under 18. Also check your annual benefit limits to avoid unexpected charges if you go over.

-- ENDS --

Survey: ‘Using that lifeline’: Australians average two claims a year on their hospital cover

New research from Money.com.au reveals that the majority of Australians with hospital insurance are using it at least once a year — with an average of two claims annually.

The nationally representative survey of more than 1,000 Australians found that half of hospital cover policyholders (51%) make 1–2 claims per year, 10% make 3–5 claims, and 7% claim six or more times annually.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says Australians aren’t just paying premiums, they’re putting their cover to use.

“Hospital insurance is a lifeline when health issues arise and thankfully, the numbers show Australians are using that lifeline. The fact that the average policyholder claims twice a year proves it’s far from a wasted expense, especially considering some surgeries and hospital treatments cost thousands of dollars,” he says.

“The most common services people claim for are elective surgeries and overnight hospital stays. Even if they originally took out a policy just to avoid the Medicare Levy Surcharge, they’re relying on it when it really counts and that’s exactly what it’s there for.”

The survey also found that one in five Australians (21%) rank hospital cover as their most essential form of insurance — and of those, 19% said it’s because it has saved them the most money.

However, nearly a third of policyholders (31%) said they’ve never claimed on their hospital cover.

Older Aussies more likely to use their hospital insurance regularly — and least likely to let it go unused

The survey found older generations are more likely to use their hospital cover regularly. For example, 68% of Baby Boomers and 47% of Gen X claim on their policy 1–2 times per year, compared to just 43% of Millennials and 39% of Gen Z.

Baby Boomers are also the least likely to leave their hospital cover unused, with only 20% saying they’ve never made a claim — compared to 40% of Gen X, 36% of Millennials, and 30% of Gen Z.

Whitelaw says older Australians are more likely to use hospital cover for actual healthcare needs, while younger Aussies may be holding policies for peace of mind or tax reasons — but not necessarily relying on them as often.

-- ENDS --

Survey: ‘Singles cover trap’: 2 in 5 Aussies on single policies underuse their health insurance extras

Singles are leaving hundreds of dollars on the table by underusing their health insurance extras cover, compared to couples and families, new research from Money.com.au reveals.

The survey found that a higher proportion of Aussies on a single policy claim only 1–2 times per year on their extras cover (40%) — meaning two in five singles are paying for benefits they rarely use. In contrast, just 20% of those on a couples policy and 31% on a family policy claim only 1–2 times per year.

Money.com.au’s General Manager of Health Insurance, Chris Whitelaw, says there’s a growing gap between singles and those on couples or family policies when it comes to getting value from their extras cover.

“It’s natural for couples and families to claim more frequently on their extras cover — more people on a policy means more people needing general or ancillary treatments, whether that’s dental visits, physio appointments or optical check-ups. Someone on a single policy may naturally claim less, but if they’re only claiming once or twice a year, hypothetically for their bi-annual dental check-up, it means they’re still paying for dozens of benefits they’re not using,” he says.

“When it’s just you on a policy, there are fewer opportunities to claim — but you’re still paying for a full suite of extras. That’s where the singles cover trap kicks in: many singles are forking out for benefits they barely use, leaving hundreds of dollars on the table every year.”

How often should singles claim on their health insurance extras?

Whitelaw says single policyholders claim on average three times a year on their extras cover, typically for common services like an annual dental check-up, optical needs, or occasional physio.

The survey found that more than a quarter of single policyholders (26%) claim on their extras 3–5 times per year, while 16% claim 6–10 times per year, and only 9% claim more than 10 times per year. A small percentage (9%) say they never claim on their health insurance extras.

Couples squeeze the most value out of their health insurance extras

The research reveals that families have the highest proportion claiming 3–5 times per year (33%), followed closely by couples (31%).

However, couples are more likely to claim at higher frequencies, with 26% claiming 6–10 times annually compared to 19% of families. Couples also lead in the highest usage bracket, with 17% claiming more than 10 times per year, versus just 9% of families.

Additionally, couples have fewer non-claimers — only 6% say they haven’t made a claim at all, compared to 8% of families.

-- ENDS --

Media/journalist enquiries:

Need a data breakdown by state, age or income — or have an idea for a consumer question? Contact our Head of PR: Megan Birot at megan@money.com.au.

Our expert health insurance commentators

Chris Whitelaw, General Manager – Health Insurance

Chris Whitelaw is Money.com.au’s General Manager – Health Insurance. He leads our strategy and delivery in what is a key and often misunderstood product for Australian consumers. Chris has more than decade of experience working in the health and wellbeing industry, as a Director of Operations APAC for a major multinational. He has a combined 20 years of contact centre management experience and is passionate about helping our customers find the right health insurance product for them at a fair price. He’s currently studying for an MBA at the Australian Institute of Business.

Sean Callery, Editor

Sean Callery is Money.com.au's Editor. He's an experienced author and editor with expertise in finance, insurance, and investment topics. He leads Money.com.au’s editorial team and manages content on site across all verticals. Sean is also a spokesperson for all things personal finance and is regularly quoted as a finance expert by Australia's leading media outlets. He is qualified with a Certificate IV in Finance and Mortgage Broking.