Home Loan research & insights

Money.com.au conducts regular consumer surveys and in-depth data analysis to uncover how Australians buy property, finance their homes and manage their mortgages.

Research is compiled by our experienced PR & Editorial team. Updated 13 Jul 2026.

Below you’ll find the latest Money.com.au home lending research, ordered from most recent to least.

All surveys are independently commissioned and carried out by a third-party research agency. Each study is nationally representative by age, gender and location.

Our research is frequently featured across major news outlets and is designed to help Australians make more informed financial decisions, but also to support journalists and policymakers with data-driven insights.

If you use this information, please include a link to the page you’re currently on: https://www.money.com.au/home-loans/research-insights

Want to see more Money.com.au research and insights? Add us as a preferred source in Google Search.

2026 published research

Survey: 52% of Aussies expect Census 2026 to show they're financially worse off than 5 years ago

New research from Money.com.au reveals that 52% of Australians — equivalent to 11.5 million people — expect their Census 2026 responses to show their household is financially worse off than it was five years ago when the last national snapshot was conducted.

Meanwhile, a third of Australians (33%) say their financial situation hasn’t changed since the last Census was conducted in 2021. Only 16% say they’re financially better off today than five years ago.

The 2026 Australian Census will be held on Tuesday, 11 August and conducted by the Australian Bureau of Statistics (ABS).

Money.com.au’s Head of Insights, Sean Callery, says millions of Australians have worked hard over the past five years without seeing a meaningful improvement in their financial position or living standards.

"This year's Census won't be a positive report card for either the Government or the Reserve Bank. If most Australians feel they've gone backwards financially over the past five years, it's a sign many households don't feel the economy has worked in their favour," he says.

"However, we were living in a very different financial environment at the time of the 2021 Census. The country was emerging from the pandemic, the cash rate was sitting at a historic low of 0.10%, and there was far less pressure on household budgets from housing, fuel, insurance and other everyday essentials."

"Housing costs remain a sticking point nationally. Whether you're paying a mortgage or rent, a growing share of household income is being swallowed by the cost of keeping a roof over your head. That makes it harder to build savings, invest for retirement and feel financially secure, even as wages rise."

Housing costs emerge as the biggest driver of financial deterioration

The research found that housing costs have become the biggest financial pressure point for Australians, with 59% saying they expect Census 2026 to show their rent or mortgage costs have risen faster than anticipated since 2021.

Income or wages ranked as the second-most deteriorated area of household finances, with 52% of Aussies saying their income has not kept pace with living costs.

This was followed by hours worked or job security, with 23% of respondents citing reduced working hours or concerns about employment stability. Finally, 18% said their employment status had worsened since 2021, including becoming unemployed, underemployed or leaving the workforce altogether.

Older Australians most likely to feel financially worse off since the last Census

Gen X and Baby Boomers are the most likely to expect Census 2026 to show they’re financially worse off than five years ago, with 60% and 53% respectively saying their household finances have deteriorated since 2021. This was followed by Millennials (49%) and Gen Z (34%).

Gen X are the generation most likely to say their housing costs have increased more than expected since the last Census, at 67%. They’re followed by Millennials (61%), Gen Z (55%) and Baby Boomers (50%).

-- ENDS --

The divorce tax: Separation costing Australians their family home

New research from Money.com.au reveals the family home can become one of the biggest casualties when couples who jointly own property break up.

The nationally representative survey found more than one in four Australians (27%) have experienced a divorce or separation while co-owning a home with a partner.

Among this group, only 51% said one partner was able to retain the property. Nearly a third (31%) were forced to sell because neither person could afford to keep the family home or buy out the other party. A further 16% sold for other reasons, like relocating or downsizing, while just 2% kept the property as an investment.

Money.com.au’s Mortgage Expert, Nick Burgess, says many Australians underestimate how difficult it can be to keep a home after a separation.

"A separation reduces a household’s financial capacity. Going from two incomes supporting a mortgage on the family home to a single income can quickly create a financial shock that sets people back years. Many people either don’t have enough borrowing power to buy out their former partner, or they can't service the mortgage repayments on the family home on their own,” he says.

"For many couples, keeping the family home simply isn’t realistic. They’re forced to sell and split the equity, which often leaves both parties with smaller deposits for their next purchase and the challenge of buying back into a market where prices continue to rise and borrowing as a single applicant is significantly harder. In fact, many solo buyers don’t meet bank serviceability requirements at today’s property prices."

"That’s why many Australians end up renting for a period after a separation. While some eventually buy again on their own, others may need to rebuild their financial position first, and many ultimately return to the market with a new partner."

Rebuilding after separation: Many Australians rely on a new relationship to re-enter the market

The research found that while many Australians eventually return to homeownership after a separation, only 58% were able to purchase another home independently.

Meanwhile, 30% re-entered the property market with a new partner or spouse, while more than one in ten Australians (12%) said they had not been able to buy another home since separating.

Break-up penalty hits younger Australians harder

Younger Australians appear to face greater financial disruption after separation. Millennials and Gen Z were the most likely to be forced into selling their home (38% and 36% respectively), compared to 33% of Baby Boomers and 25% of Gen X.

Meanwhile, Gen X were the most likely to keep ownership within the family, with 60% saying one partner retained the property. This was followed by 52% of Millennials, 47% of Baby Boomers and 36% of Gen Z.

The research found that 73% of Australians have never experienced a divorce or separation while co-owning a home with a partner.

-- ENDS --

53% of Australians no longer believe they can pass on property to future generations

For generations, Australians have viewed property as the best way to build wealth and leave something behind for their children.

But as the Government overhauls property investment rules — including restrictions on negative gearing, replacing the 50% capital gains tax (CGT) discount, and banning SMSFs from borrowing to invest in residential property — new research from Money.com.au reveals Australians are losing faith that property will remain the pathway to generational wealth it once was.

The nationally representative survey of more than 1,000 Australians found the majority (53%) don't believe they'll be able to pass property on to future generations through homeownership or property investment as previous generations did. Just 47% believe they still can.

Money.com.au’s Property Expert, Nick Burgess, says Australians are questioning whether property can still deliver the same wealth-building opportunities it has for previous generations.

"Property has traditionally been seen as one of the most reliable ways to build wealth through capital growth and rental income, and to create some financial legacy for future generations. But now, more people believe that opportunity is slipping away and confidence in bricks and mortar is eroding," he says.

"Affordability remains the biggest obstacle, but it's notable that many Australians believe government policy is making property investment less rewarding. Changes to negative gearing, CGT concessions and SMSF borrowing are pouring cold water on the aspirations of millions of Australians, many of them mum-and-dad investors, to build wealth through property and pass it on to their children and grandchildren."

Older Australians are the least confident about property's future

Perhaps surprisingly, the survey found that older Australians don't believe they'll be able to pass property wealth on to their children, with 56% of both Gen X and Baby Boomers holding that view. That's compared to 47% of Millennials and 46% of Gen Z.

"Older Australians are the generation closest to passing on their wealth, so they're naturally more sceptical about how changing affordability and investment settings could affect what they'll actually be able to leave behind. If they're losing confidence that property will deliver the legacy they once expected, that's a significant shift," says Nick.

"On the other hand, younger Australians are likely more focused on the challenge of buying their first property than the practical realities of one day passing wealth on to their children."

Property prices remain the biggest barrier to building wealth

The research found that affordability remains the biggest reason Australians no longer see property as a pathway to generational wealth, with 51% saying high property prices and mortgage costs have made it too difficult to enter the market.

A further 27% say it’s because their wages haven't kept pace with housing costs, while 22% believe government taxes and policies have reduced the returns on investment properties.

-- ENDS --

Young Aussies call for mortgage shake-up as support grows for income-based home loans

Young Australians are leading calls for a mortgage shake-up, throwing their support behind income-based home loans that could offer cheaper rates to lower-income earners.

New research from Money.com.au reveals 51% of Australians would support income-based mortgage pricing — a model where lower-income earners could access discounted home loan rates, either directly through lenders or via government subsidies similar to existing housing affordability schemes.

Support for income-based mortgage pricing is being driven overwhelmingly by younger Australians, including 68% of Gen Z and 58% of Millennials. By comparison, support falls sharply among older Australians, with 47% of both Gen X and Baby Boomers supporting the idea.

When asked where the annual household income threshold for discounted loan rates should sit, the average figure suggested by homeowners was $115,000. However, younger Australians drew the line higher, with Gen Z and Millennials saying households earning up to $125,000 should remain eligible for cheaper home loans. Gen X and Baby Boomers each set the threshold at $115,000.

Money.com.au’s Mortgage Expert, Nick Burgess, says the findings raise questions about whether alternative lending models like income-tested mortgage pricing could emerge as another tool to address intergenerational inequality.

“Younger Australians, who are earlier in their careers and typically earning lower incomes, face higher property prices, larger deposit hurdles and tougher pathways into home ownership than previous generations. They’re also generally more likely to feel the squeeze from interest rate rises, so an income-tested model could potentially ease some of that pressure,” he says.

"One way to slice it could be that households earning under $115,000 could receive a subsidised home loan rate of 5%. From there, the rate could increase by 0.25 percentage points for every additional $10,000 in household income. Under this example, a household earning $125,000 could receive a rate of 5.25%, while households earning around $155,000 would move closer to the average rate of 6%."

"Something like this would only work through a government-supported model, where lower-income borrowers receive subsidised interest rates through targeted assistance. While it would differ from schemes like the First Home Guarantee, it could operate in a similar way by partnering with lenders and applying specific eligibility criteria to improve access to home ownership for those on lower incomes.”

“The difference with income-tested mortgages versus existing support measures is it would likely require banks to make more significant changes to their systems and it would be much more expensive for the Government to fund. In reality, a model like this would face significant pushback and would be unlikely to get off the ground unless something major changed."

Older Aussies more likely to push back on income-tested home loans

Older Australians were more likely to be opposed to the idea of income-tested mortgages, with the majority of both Baby Boomers (53%) and Gen X (53%) against the concept. Opposition was lower among Millennials (42%) and Gen Z (32%).

“Older Australians may see income-tested mortgage pricing as unfair because home loans are traditionally priced around factors like risk and serviceability rather than a borrower’s income level,” says Nick.

"They also entered the housing market under very different conditions and may see affordability challenges as something borrowers need to navigate individually rather than through changes to lending models or additional government support."

-- ENDS --

Bank of Mum and Dad: 64% of family-funded home purchases have no formal agreement

New research reveals that most Australians who receive financial support from their parents to buy their first home are doing so without formal paperwork, potentially exposing both generations to financial and legal disputes down the track.

The nationally representative survey by Money.com.au found that 64% of first-home buyers who received financial support from the Bank of Mum and Dad either had no formal agreement in place or relied on a verbal ‘handshake’ agreement.

In contrast, only 36% of first-home buyers had a legally binding written agreement.

Money.com.au’s Mortgage Expert, Nick Burgess, says family support can be invaluable, but it's important to document the arrangement clearly from the outset.

"Property prices have become so expensive that many first-home buyers can't buy a home without the Bank of Mum and Dad. But when tens or even hundreds of thousands of dollars are being lent, gifted or secured against the family home, relying on a verbal understanding can create problems later on," he says.

“For example, I've seen family disputes emerge years after a property purchase because there was never a clear agreement about whether the deposit was intended for their child alone or for the couple jointly. Things also get complicated when parents have guaranteed part of the loan and the relationship later breaks down. In some cases, lawyers need to get involved, and what started as a generous gesture can turn sour for everyone involved."

Gift and loan letters are not a formal agreement

Nick says one of the most common sources of family conflict is whether money provided by parents was intended as a gift or a loan.

"That's a distinction families should be clear on from the outset, because lenders will generally require a letter confirming whether parental financial support is being provided as a genuine gift or a loan when assessing a mortgage application,” he says.

"While this satisfies the lender, it doesn't protect the family because it doesn't address what happens if the property is sold, the owners separate, or if family dynamics change. Families should consider whether they also need a separate agreement that clearly sets out everyone's expectations and responsibilities.”

What families put in writing when helping first-home buyers

Among those who had an agreement in place, nearly half (46%) covered whether the parental contribution was a genuine cash gift or a loan that needs to be repaid.

Around 39% outlined what would happen to the family contribution in the event of a separation or relationship breakdown, while 23% addressed whether the Bank of Mum and Dad would need to be repaid if the property is sold.

Just 14% included details around ownership rights or equity share arrangements in the property, like whether parents who contributed funds would have any financial interest in the home.

Today’s young Aussies more reliant on parental support and cash gifts

The research found more than one in five Australians (21%) received financial support from parents or family to purchase their first home, including cash gifts, loans or guarantor support.

Gen Z homebuyers were by far the most likely to receive family assistance, with 76% receiving support from parents or family members. Cash gifts were the most common form of assistance, received by 39%.

Millennials were the next most likely to receive help from the Bank of Mum and Dad (38%), with cash gifts again the most common form of support (22%).

The rate fell sharply among older generations, with 18% of Gen X and just 8% of Baby Boomers receiving financial support to buy their first home.

-- ENDS --

‘Stop the Facebook and AI university’: 58% of homeowners lost in mortgage jargon

New research from Money.com.au reveals a major mortgage literacy gap among Australian homeowners, with a whopping 58% admitting they don’t fully understand crucial home loan concepts.

Loan-to-value ratio (LVR) was the most commonly misunderstood term, with 26% of homeowners saying they don’t understand it — despite it playing a major role in how lenders determine a borrower’s eligibility for a mortgage, what interest rate they qualify for, and whether they’ll have to pay Lender’s Mortgage Insurance (LMI).

Redraw facilities and offset accounts were the next biggest blind spots for homeowners, with 17% saying they’re unsure how they work, despite both being key interest-saving features. LMI followed closely, with 16% of respondents confused about what it means.

Comparison rates also remain unclear for 14% of borrowers, while one in ten homeowners (10%) don’t fully understand what equity is.

Money.com.au’s Mortgage Expert, Nick Burgess, says there's a growing mortgage knowledge gap particularly as more borrowers rely on social media or AI tools for unqualified or overly general advice.

“If you don’t have a firm grasp on basic mortgage terms and features, you’re likely not maximising your loan’s potential and could end up paying more interest over the loan’s life or dragging out your mortgage for longer than you need to,” he says.

“Too many borrowers are graduating from what I’d call the Facebook and AI university. They rely on generic online information to understand how a mortgage works, as well as social media opinions. Also, one in five Aussies say they trust AI tools like ChatGPT for home loan information, so the risk of misinformation is getting out of hand.”

“Your mortgage is likely the biggest debt you’ll ever take on, so it pays to understand key concepts like LVR, how the comparison rate differs from the advertised rate, and the difference between an offset account and a redraw facility. If you’re unsure about anything, don’t be afraid to ask your lender or broker to break it down for you.”

How mortgage confusion is playing out for real borrowers

“I had a first-home buyer who got into the market in Sydney with a 5% deposit try to refinance a year later without realising their LVR was still above 80%, which would have meant paying LMI all over again,” says Nick.

“I also had a middle-aged couple with kids that had $200,000 sitting in a regular savings account instead of their offset account because they assumed the offset was just another transaction account. No one had properly explained to them that every dollar sitting in an offset works dollar-for-dollar to reduce the amount of interest charged on their home loan.”

“I’ve also seen borrowers take out personal loans for major expenses like buying a car or renovating part of their home because they didn’t know they could use the equity they’d already built up in their property to finance those costs at a much lower interest rate.”

Mortgage confusion spans every generation

The research found Gen Z and Millennials were the most likely to admit they don’t fully understand important mortgage terms, with 61% of each cohort reporting confusion around loan concepts like LVR and offset account. Gen X followed closely behind at 58%, while Baby Boomers were not far off at 59%.

-- ENDS --

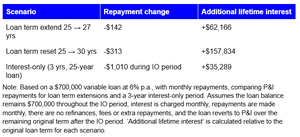

Cut repayments now, pay later: The hidden cost of mortgage reshuffles as interest rates rise

New research from Money.com.au reveals homeowners are pushing their mortgage debt further into the future as interest rate pressure builds, with another rate hike potentially on the horizon next week, on May 5.

The nationally representative survey found 30% of homeowners would extend their loan term by 1–3 years to cope with rising repayments if rates increase further. Worryingly, nearly one in five (19%) would reset their loan back to a full 30-year term, and effectively undo years of progress on their mortgage.

A further 13% would consider switching part or all of their loan to interest-only repayments if the RBA continues to lift rates.

Only 38% of borrowers say they wouldn’t take any of these measures to ease repayment pressure.

Money.com.au’s Mortgage Expert, Nick Burgess, says rising interest rates are pushing many borrowers to opt for short-term repayment relief without considering the long-term cost of their mortgage.

“A lot of borrowers default to extending their loan term in high-interest environments to reduce their monthly repayments, but they often underestimate how much more interest they’ll pay over the life of the loan,” he says.

“It’s a way of kicking the can down the road to ease pressure now while everyday costs like fuel, groceries, insurance and utilities continue to rise. A lot of households are feeling the squeeze from all sides, and for many, stretching out their mortgage feels like one of the few levers they can pull right now.”

“Extending your loan term or switching to interest-only repayments can offer immediate breathing room through lower monthly repayments, but it often comes at the expense of thousands of dollars in additional interest over time.”

“Switching to interest-only repayments fundamentally changes how the loan works because you stop paying down the debt altogether during the interest-only period. While it can deliver the biggest short-term reduction in repayments, it can lead to higher costs and a sharp jump in repayments later on.”

Borrowers chasing short-term relief face long-term interest bill

On a $700,000 variable loan at 6% p.a., resetting a 25-year mortgage to a 30-year term could save borrowers $313 a month, but add $157,834 to the total interest bill over the life of the loan. A more modest two-year extension from 25 to 27 years delivers $142 in monthly relief, though it still adds $62,166 in cumulative interest.

The deepest short-term reprieve comes from interest-only arrangements, which can cut monthly costs by $1,010. However, this strategy causes total interest costs to rise by $35,289, as the principal balance remains untouched during the interest-only period. Nick says once that period concludes, borrowers typically face a sharp ‘payment shock’ as the loan reverts to principal-and-interest repayments over the remaining term. In this example, it would jump by $1,282 once the IO period is over.

Younger Australians more likely to adjust loans Younger borrowers are far more likely to adjust their home loans to cope with rising rates, with Gen Z (44%) and Millennials (38%) the most likely to extend their loan term by 1–3 years. This is compared to 23% of Gen X and 17% of Baby Boomers who said the same.

Gen X (23%) are the most likely to reset their loan back to a 30-year term, followed by Gen Z (22%), Millennials (19%) and Baby Boomers (12%).

Millennials (15%) and Gen X (12%) are also more open to switching to interest-only repayments, compared to 11% of Boomers and just 6% of Gen Z.

-- ENDS --

Priced out of Australia: 30% of Aussies eye overseas property due to housing crisis

Australians are looking for a way out of the housing crisis — and many are now setting their sights offshore.

New research from Money.com.au reveals nearly one in three Australians (30%) want to buy property overseas as rising house prices and cost-of-living pressures push buyers to look beyond the domestic market.

Among them, 14% say they want to purchase an investment property overseas, but continue to live in Australia, while 8% want to buy overseas to live and work, and another 8% want to buy a property overseas for retirement.

Among the destinations Aussies would consider buying property in, Asia was the front-runner (36%), followed by Europe (29%) and New Zealand / Pacific Islands (19%). The US (13%) and Middle East (3%) ranked lower.

Money.com.au’s Property Expert, Nick Burgess, says more Australians are starting to question whether they’re getting value for money domestically.

“Younger Aussies in particular are starting to question whether they’re priced out of the local market and are increasingly comparing what their money can buy here versus overseas. In Australia, buyers often take on much higher debt relative to their income, whereas in parts of Europe and Southeast Asia, it’s possible to purchase property with significantly less debt — and in some cases, be nearly or completely debt-free,” he says.

“Social media is also fuelling the trend, with more Australians seeing people like them, often young couples or families, sell up and relocate overseas, which makes the idea feel more achievable.”

Nick says buying property overseas isn’t straightforward, particularly when it comes to financing.

“Getting a home loan for an overseas property is extremely difficult. Most lenders in Australia won’t finance international purchases, due to the difficulty of registering security against foreign assets. This means buyers typically need to rely on cash savings, sell up and relocate or cash out some equity from an existing Australian property to buy overseas,” he says.

“The risk is that you could end up overleveraged, especially if you’re increasing debt on your Australian property to fund an overseas investment. If things don’t go to plan, you’re still on the hook for that debt back home.”

“Australians buying overseas don’t have access to the same protections they’re used to at home. Legal systems, property rights, contract processes and buyer protections can vary depending on the country, so it’s critical to do your due diligence and not rely on advice from social media.”

The research found the majority of Australians (70%) wouldn’t consider buying a property overseas.

Young Aussies leading the ‘property escape’

The shift is being driven overwhelmingly by younger Australians, who are far more open to buying overseas than older generations.

More than half of Gen Z (58%) want to purchase property overseas in some form, including 31% who would buy an investment property while continuing to live in Australia, and 15% who would consider relocating to live and work overseas. Millennials are not far behind, with 46% open to buying overseas, led by investment-focused purchases (23%).

In contrast, interest drops sharply among older groups, with just 27% of Gen X and only 10% of Baby Boomers open to the idea. In fact, nine in ten Boomers (90%) say they wouldn’t consider buying property overseas at all.

State summaries

NSW — highest interest in buying overseas Nearly a third of people in New South Wales want to buy property overseas (32%) — the highest share nationally. That’s not too surprising given NSW has the largest average mortgage size in the country ($872,752), and borrowers, particularly in Sydney, tend to have higher housing debt-to-income ratios.

NSW residents are also the most likely to want to buy an investment property overseas while continuing to live in Australia (18%).

Nick says high debt levels are pushing NSW buyers to think differently, and for some, that means looking overseas where the entry price is lower and the financial pressure isn’t as intense.

NSW buyers are fairly evenly split across potential overseas destinations to buy property, although Asia remains the clear front-runner (36%).

VIC — second highest interest in buying overseas Victorians are the second most likely to consider buying property overseas, with 31% saying they would consider it. Victorians also have the second-highest interest in buying an investment property overseas while continuing to live in Australia (16%).

Victorian buyers show the strongest preference for Asia, with 41% selecting it as their top destination to buy property in — higher than all other states.

“More Victorians are chasing affordability and lifestyle, but many feel priced out of the domestic market. As a result, they’re looking to places like Southeast Asia, where the cost of entry is far lower,” says Nick.

QLD — interest in buying overseas on par with national average Queenslanders are in line with the national average for buying property overseas, with 30% considering the idea due to the rising cost of housing and living.

Interest is spread fairly evenly across different motivations, with 11% of Queenslanders saying they would buy overseas to live and work, 10% for retirement, and 9% planning to purchase an investment property abroad while continuing to live in Australia.

Queenslanders are far more drawn to nearby markets, with 26% considering New Zealand and the Pacific — one of the strongest regional preferences across the country.

WA — interest in buying overseas on par with national average While Western Australians are in line with the national average when it comes to wanting to buy property overseas (30%), they’re the most likely of any state to consider buying overseas to live and work abroad (14%).

Nick says the recent property boom in Western Australia is likely pushing some buyers to consider buying and living overseas, as rising prices leave many feeling priced out of the local market.

In terms of destinations, WA buyers are casting a wide net, with Asia the most popular choice (39%), followed by Europe (30%). They’re also the most likely of any state to consider buying property in the United States (18%).

**SA — lowest interest in buying overseas ** South Australians are the least likely to consider buying property overseas, with just 23% open to the idea, well below the national average. However, those who are interested tend to skew towards buying overseas for retirement, with 12% considering this option — the highest share nationally.

They’re also the most likely to choose Europe as the destination they’d consider buying property in (41%) — the highest share nationally.

-- ENDS --

Home deposit killers Aussies won’t quit’: Streaming, coffee & matcha top the list

Australians aren’t giving up the small luxuries — or the escapism — even to save for a house deposit.

New nationally representative research from Money.com.au reveals the everyday spending habits Australians refuse to cut back on, with streaming subscriptions topping the list (23%), followed by takeaway coffee or matcha (18%) and online shopping (16%).

Eating out ranks next at 14%, followed by food delivery and takeaway meals (13%). Further down the list are date nights (11%) and betting apps or gambling (5%).

Money.com.au’s Mortgage Expert, Nick Burgess, says there’s a growing disconnect between traditional saving advice and the reality of today’s housing market, particularly for first home buyers.

“Those ‘small luxuries’ have become a relatively low-cost escape from the doom and gloom of the cost-of-living crisis. For many Australians, cancelling Netflix or skipping their daily coffee or matcha doesn’t feel like it’s going to move the needle,” he says.

“The other side of the coin is that government schemes have made it possible to buy a home with a 5% deposit, so cutting back to save every last cent doesn’t feel necessary anymore.”

“However, when I speak to young buyers, a lot of the feedback I still get is that their parents were able to save for a deposit in a very different environment, when house prices were lower relative to incomes. Today, it can feel like no amount of cutting back on coffee will get them to their deposit target sooner.”

“The challenge is that too much discretionary spending is precisely what lenders scrutinise when you finally apply for a home loan. All those ‘little’ expenses, your Netflix, Uber Eats, daily coffee, are baked into what lenders realistically expect you to spend.”

“But if that discretionary spending runs higher than a lender’s benchmark, it can eat into how much you can borrow. In some rare cases, it can shave tens of thousands — sometimes $20,000 or more — off your borrowing capacity.”

Gen Z live up to the ‘avo on toast’ stereotype

The research found Gen Z are the most reluctant to give up eating out (21%), living up to the long-standing ‘avo on toast’ stereotype. Streaming subscriptions (19%) and takeaway coffee or matcha (18%) follow, along with social spending like date nights (14%). Food delivery (13%), online shopping (10%) and gambling (5%) trail behind.

Millennials least likely to give up their daily brew

Millennials are most reluctant to give up their takeaway coffee or matcha (22%), on par with streaming subscriptions (22%), followed by food delivery or takeaway meals (16%). Eating out (14%) and online shopping (12%) also rank highly, while date nights (10%) and gambling (4%) are less of a priority.

Streaming is non-negotiable for Gen X

Gen X are most reluctant to give up their streaming subscriptions (28%), followed by online shopping (16%) and takeaway coffee or matcha (15%). Food delivery or takeaway meals (14%) and eating out (12%) also rank among the harder habits to cut, while date nights (11%) and gambling (4%) are less of a priority.

-- ENDS --

Survey: 61% of property investors say CGT and negative gearing reforms would prompt them to pull back or sell

New research from Money.com.au reveals how property investors say they would respond if reforms to the Capital Gains Tax (CGT) discount and negative gearing rules were introduced.

The nationally representative survey found that 39% of property investors say reducing the 50% CGT discount on the sale of investment properties would prompt them to step back from investing in real estate or sell existing investments to cash in on current tax settings.

A further 22% said capping or limiting negative gearing concessions to one property would lead them to take similar action.

The Australian Government is weighing reforms to investment property tax settings ahead of the 2026–27 Federal Budget on May 12. Provisions would protect existing investors through ‘grandfathering’, meaning the changes would apply only to new property investments.

Money.com.au’s Mortgage Expert, Nick Burgess, says any tax policy changes risk having unintended consequences for Australia's property market, at a time when housing supply is low.

“If property investors pull back or consider selling, that has real implications for rental prices, as fewer investment properties means fewer homes available to rent, which can push rents higher. Some investors may also increase rents to offset the impact of these changes on their returns or delay selling or hold out for higher prices to maintain their after-tax returns,” he says.

“It also raises questions about whether these changes will genuinely improve housing affordability. Not every Australian renter is in a position to become a homeowner due to lending serviceability requirements and the ballooning costs of homeownership, including stamp duty, council rates, insurance and maintenance.”

“The research suggests some investors may scale back or shift away from property towards other asset classes, but it remains to be seen how material the impact would be in practice.”

The survey found that 39% of property investors say neither policy would impact their decision to continue investing in real estate.

Around 2.26 million Australians own an investment property, according to ATO data — including nearly 640,000 who own two or more properties.

Investor response to tax reforms varies by state, with SA and QLD most sensitive to CGT changes

Investor sensitivity to tax changes varies significantly by state, with South Australia and Queensland most responsive to CGT reforms, while reactions to negative gearing changes are more mixed across the country.

For example, South Australia (45%) and Queensland (42%) record the highest share of investors who say they would scale back their investment in real estate if the CGT discount was reduced — both above the national average. This compares to 38% in NSW and 39% in Victoria, while Western Australia trails at 33%.

Reactions to negative gearing changes are less uniform, with 33% of investors in Western Australia say capping concessions would prompt them to pull back or sell, followed by 25% in NSW and 22% in Victoria, with lower shares in Queensland (16%) and South Australia (11%).

-- ENDS --

Pay the bank or see the doctor? 44% of Aussies delay healthcare due to home loan pressure

Mortgage stress is forcing many Australians to make difficult trade-offs with their most important asset — their health.

New research from Money.com.au reveals that nearly one in two Australians (44%) have delayed or put off medical care in the past five years due to mortgage costs.

Among those who delayed care, 61% skipped or put off dental appointments, while 23% postponed specialist visits and 12% delayed mental health treatment. A further 4% put off surgery or other medical procedures.

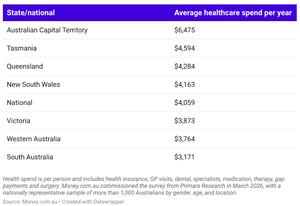

With Australians spending an average of $4,059 per year on healthcare, rising home loan costs are making it harder for many households to keep up with both essential expenses. *Health spend is per person and includes health insurance, GP visits, dental, specialists, medication, therapy, gap payments and surgery.

Healthcare costs vary significantly across the country, with Australians in the ACT spending the most at an average of $6,475 per year, followed by Tasmania ($4,594), Queensland ($4,284), New South Wales ($4,163) and Victoria ($3,873). Western Australians ($3,764) and South Australians ($3,171) recorded the lowest healthcare spending.

Money.com.au’s Mortgage Expert, Debbie Hays, says rising healthcare costs are also forcing Australians to tap into their home loans to pay for treatment.

“More borrowers are tapping into their offset or redraw accounts to pay for medical expenses or elective surgery when they need it sooner than the public system allows,” she says.

“In most cases, they’re doing a home loan top up for larger procedures or after-cancer care if they’ve drained their offset due to time off work for treatment. It means people are effectively putting healthcare on their mortgage and paying interest on it over time.”

“I had a client ask to increase their home loan by $60,000 for medically necessary dental implants and restoration after chemotherapy. In another case, a borrower with Motor Neurone Disease increased their loan by $100,000 to help cover the treatment costs.”

“We’re also seeing this trend of people increasing their loan balance to get medical care overseas, where costs can be as little as half those in Australia.”

The research found half of Australians (50%) have dipped into their redraw or offset account to cover medical expenses, while 24% have increased their loan amount to do the same.

How rising healthcare costs could lock Aussies out of homeownership

Most healthcare spending is captured within the standard Household Expenditure Measure (HEM) lenders use to assess borrowers, based on typical costs like housing, groceries, bills, healthcare and transport. The HEM is applied as a baseline to estimate living expenses when calculating borrowing capacity.

However, if your healthcare costs push your living expenses above the HEM benchmark, lenders will typically assess you using the higher, actual amount — which can reduce your borrowing capacity.

Some healthcare-related expenses also fall outside the HEM and are assessed separately, which can further limit your borrowing.

“For example, health and life insurance fall outside the HEM as they’re often treated as discretionary expenses because they can be reduced or cancelled if needed — even though, in reality, they’re essential for many households,” says Debbie.

Modelling shows that spending just $2,000 per year on healthcare outside the HEM can reduce borrowing capacity by around $20,000 for a single applicant, depending on the lender.

“At the same time, higher healthcare costs can make it harder to save for a deposit. It becomes a double hit. It reduces borrowing power and slows the pace of saving for a deposit, particularly for younger Aussies trying to buy before prices move further out of reach,” says Debbie.

The research found younger Australians have the highest healthcare spend nationally. Gen Z report average annual healthcare spending of $5,333, followed by Millennials at $4,843 — both well above Gen X ($3,435) and Baby Boomers ($3,647).

-- ENDS --

Money’s State-by-State Mortgage Insights: VIC closes in on NSW & QLD loses investor momentum

Money.com.au has released its latest State-by-State Mortgage Insights Report, outlining key trends in the housing loan market and providing 2026 projections across Australia.

Download the FREE report on our research & insights page.

Home lending to grow 7% in 2026 as investor demand continues momentum

Australia’s housing loan market is facing potential headwinds, particularly in the investor segment, amid speculation around changes to the Capital Gains Tax (CGT) discount for investors and a cap on negative gearing.

Home lending growth is forecast to hit 7% in 2026 (to 594,279 loans) — with the investor segment set to grow at nearly twice that rate (13%) to 246,598 loans, based on current growth rates.

However, with two 0.25 percentage point cash rate hikes already delivered this year and further increases expected, owner-occupier growth is forecast to ease slightly to 3% in 2026 as rate pressures build.

NSW still going strong as investor demand and land loans surge

Total lending in New South Wales is forecast to grow by around 9% in 2026, with investor demand doing most of the heavy lifting. Investor loans are expected to jump 16% to 77,470, compared with more modest 4% growth in owner-occupier lending, based on current growth trends.

In retrospect, the December 2025 quarter marked the state’s strongest result since December 2021, with 25,033 loans issued, up 13% year-on-year. However, NSW continues to trail Victoria in owner-occupier volumes, with 85,808 annual loans compared to Victoria’s 98,856 — a trend that has persisted since 2020.

Over the past year, investor lending in NSW rose 14%, while owner-occupier growth came in at 4%. The state is also leading the country in land loan growth across both segments — up 14% for owner-occupiers and 25% for investors — pointing to strong demand for new builds and development opportunities.

NSW now accounts for 31% of all new investor loans nationally — the biggest share since March 2022.

Victoria closes in on NSW as fastest-growing loan market

Victoria is on track to nearly match New South Wales as Australia’s largest lending market in 2026, with total loans forecast to reach 166,345 — which would put it just 300 loans behind NSW. Total lending is expected to rise by around 10%, based on current growth trends. This would make Victoria the fastest-growing major state this year.

The turnaround is being driven by a sharp rebound in investor activity. Investor lending rose 21% over the past year, more than five times the pace of owner-occupier growth at 4%.

This allowed Victoria to reclaim second place from Queensland in investor market share.

At the same time, Victoria continues to cement its position as the country’s largest owner-occupier market, with 98,856 loans issued in the 12 months to December 2025 — just shy of the 100,000 milestone.

Victoria recorded 13,048 more owner-occupier loans than NSW in 2025, but it still trails NSW by 14,712 loans in the investor segment.

Money.com.au’s Property Expert, Debbie Hays, says Victoria is regaining momentum as affordability draws buyers back into the market.

“Melbourne’s relative affordability compared to other capital cities is drawing investors back, while also generating renewed interest from owner-occupiers and first-home buyers,” she says.

“Victoria remains one of only two states yet to exceed its 2022 investor loan levels, which suggests there’s still significant room for growth as the market continues to recover.”

Queensland loses investor momentum as growth moderates

Queensland’s lending market is expected to grow more modestly in 2026, with total loans forecast to rise 4% to 128,034. This includes 2% growth in owner-occupier loans (to 74,856) and 6% growth in investor lending (to 53,178), based on current growth rates.

If current trends continue, Queensland could fall more than 10,000 loans behind Victoria in investor activity this year, despite starting ahead a year earlier. This shift highlights how demand is moving toward markets offering a mix of affordability and stronger rental yields, tempering Queensland’s previously strong position.

Over the past year, investor lending in Queensland grew 8%, but this still lags the stronger gains seen in NSW and Victoria. Owner-occupier lending rose 3%, with total volumes reaching their highest level since the year to December 2022.

“Queensland is losing some of its investor edge, with some buyers increasingly turning to other states offering better value and the potential for stronger returns. That said, the state will continue to draw strong interest from both lifestyle investors and homebuyers,” says Debbie.

South Australia stable, but rising loan sizes tell a different story

South Australia’s lending market is expected to remain relatively steady in 2026, with owner-occupier loan growth forecast at around 3% and investor lending at 6%, based on current growth trends.

This broadly mirrors performance over the past year, when owner-occupier lending rose 3% and investor lending increased 7% — both below national growth rates, pointing to stable but subdued market conditions.

However, loan sizes in South Australia tell a different story. The average loan has now pushed past $600,000 for both segments, with investor loan sizes rising 13% year-on-year — more than double the national average of 6%.

The average investor loan size ($603,838) is now more than $69,000 higher than a year ago. This suggests the state is being driven more by rising property values than an increase in transaction volumes.

Western Australia set for lending pullback after five-year boom

Projections based on current growth trends show Western Australia is expected to be the only state to see home lending decline in 2026, with total loan volumes forecast to fall by around 1%. This includes a 2% drop in owner-occupier lending and a 0.3% dip in investor loans — or roughly 1,000 fewer loans than in 2025.

The slowdown follows a strong five-year run, during which investor lending more than tripled, rising from 7,433 to 25,963 as buyers capitalised on the state’s booming property market. However, momentum began to ease toward the end of 2024 and has continued to soften.

Western Australia was also the only state to record a decline in lending in 2025, with total volumes down slightly year-on-year. The drop was driven by owner-occupier lending, which fell 1% from 41,316 to 40,870 loans, while investor activity remained largely flat at 0.4% from 25,860 to 25,963 loans.

The pullback suggests the market may be entering a consolidation phase following several years of rapid growth.

Tasmania leads the nation in investor growth — from a low base

Growth trends show Tasmania is forecast to surpass 10,000 annual loans in 2026, reaching 11,297, although this would still be below 2021 peak levels. Total lending is projected to grow by 18% annually, once again driven by investor demand, which could push the state’s investor market above both the ACT and Northern Territory. Investor lending has surged 30% over the past year, one of the highest growth rates nationally, as buyers move to capitalise on emerging opportunities in the state. Despite this surge, investor volumes remain relatively small, with 2,819 loans accounting for just 1.3% of all new investor loans nationally.

Owner-occupier lending has also been strong, rising 13% and accounting for 71% of all new loans in the state (6,785). Notably, investor lending is still yet to surpass historical peaks, suggesting further upside potential.

-- ENDS --

Green sells: The $22K premium homebuyers are willing to pay for lush lawns

Aussies aren’t just buying homes — they’re buying curb appeal, and they’re willing to pay tens of thousands more for it.

New research from Money.com.au reveals Australian homebuyers are willing to pay an extra $21,860 on average for a property with manicured lawns or high-quality landscaping.

To put the ‘green premium’ into perspective, it’s equivalent to about 10 weeks’ pay for the average full-time Australian worker, based on weekly earnings of $2,051, according to ABS figures.

Money.com.au’s Property Expert, Nick Burgess, says landscaping can have an outsized impact on perceived property value.

“There’s been a surge in ‘lawn porn’ content online, where perfectly manicured lawns rack up millions of views. That’s feeding into buyer expectations around what the Aussie backyard should look like,” he says.

“Lush, well-maintained lawns and gardens can translate into real dollars for property sellers. Homebuyers often form an emotional connection with outdoor spaces. They picture their kids or pets playing there, hosting barbecues or even a game of backyard cricket on the grass.”

“Lawns are becoming a bit of a status symbol, particularly in a competitive market where street appeal can shape how buyers feel about a property from the outset. For owner-occupiers especially, a finished outdoor space with a neat lawn means less work when they move in, which can make them more willing to stretch their budget.”

“On the lending side, we’re seeing more homeowners tapping into their equity to fund landscaping upgrades, often as a final step after completing renovations.”

Boomers willing to pay the most for curb appeal

The research found that Baby Boomers are willing to pay the steepest ‘lawn premium’, at $23,580, followed by Millennials ($22,870), Gen Z ($20,800) and Gen X ($18,950).

Nick says older homebuyers are often in a better cash or equity position to pay more for move-in-ready homes that require little to no yard maintenance.

How much extra Aussies would pay for lush lawns, by state

According to the nationally representative survey, Tasmanians are willing to pay the most for pristine lawns or landscaping, at $24,890, followed by homebuyers in New South Wales ($22,980), Western Australia ($22,440) and South Australia ($21,920).

Homebuyers in the ACT ($21,050), Victoria ($20,900) and Queensland ($20,850) were willing to pay the least for manicured lawns.

-- ENDS --

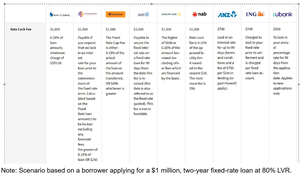

Borrowers caught off guard by ‘rate lock’ fees adding thousands to fixed rate loans

With another rate hike potentially on the cards for May, borrowers are rushing to fix their mortgages, but many don’t realise the upfront cost of locking in certainty.

A ‘rate lock’ allows borrowers to secure a lender’s advertised fixed rate on the day of their application. It acts like insurance against the lender lifting its fixed rates before the loan is finalised, so your rate remains locked in while the loan is being approved. But that protection comes at a price.

While some lenders charge a flat $500–$750 to lock in a fixed rate, others calculate the rate lock fee as a percentage of the loan amount, usually between 0.10% and 0.20%. On larger mortgages, that can quickly run into the thousands.

In one borrower scenario provided by Money.com.au, a 0.20% rate lock fee on a $1 million mortgage would cost $2,000. At 0.15%, the fee would be $1,500, while at 0.10% it would still amount to $1,000. That’s in addition to discharge fees from the existing lender, as well as the application and settlement costs on the new loan, which can also run into the thousands.

In this example, the lowest flat fee among the lenders compared is $500 from Ubank.

Borrowers rushing to fix risk rate lock fee shock

Money.com.au’s Mortgage Expert, Nick Burgess, says borrowers racing to lock in fixed rates are being caught off guard by the added cost of rate lock fees.

“Market uncertainty and expectations of more rate pain this year are driving a rush into fixed rates, but some borrowers are being caught out because they’re trying to move quickly to ‘beat the banks’ and then panic when their rate lock fee is calculated. They don’t realise these fees are structured differently depending on the lender,” he says.

“In cases where a percentage-based rate lock fee is greater than a flat fee, it should be weighed against your new fixed rate and monthly repayments, as well as any expected savings compared with staying variable, to decide whether paying a lock rate fee is genuinely worthwhile.”

“We know rate lock fees can frustrate borrowers. In some cases, brokers can negotiate with lenders to reduce the cost to the customer and help get the deal across the line. It’s never guaranteed, but it’s worth asking the question.”

What you need to know about ‘rate lock’

Lenders charge for rate certainty Most banks charge a fee to secure a fixed rate at its current level, either as a flat amount or a percentage of the loan size. However, some lenders like Bendigo Bank and Macquarie, don’t apply a rate lock fee.

Rate locks typically expire after 90 days Most lenders only guarantee a fixed rate for up to 90 days from the date the rate lock is approved. If settlement is delayed beyond that period, you can usually request an extension before the rate lock expires, typically at an additional cost. If the lock expires, you’ll need to reapply at the current rate and pay another rate lock fee.

A rate lock fee is non-refundable Rate lock fees are non-refundable (unless your loan application is declined). The fee is typically payable either when the loan is approved or at settlement. In some cases, it can be capitalised into the loan, but that means paying interest on it over the loan’s life.

A rate lock is optional You can apply for a fixed rate loan without a rate lock, and many borrowers do. That means accepting the risk that the lender could lift its fixed rates (and therefore your loan rate) before your mortgage application is finalised.

You’ll receive a lower fixed rate if rates fall

If the lender’s fixed rate drops below your locked-in rate by the time your loan settles, you’ll receive the lower rate instead. A rate lock protects you against rate increases during processing, but it doesn’t prevent you from benefiting if fixed rates move down before settlement.

-- ENDS --

Renters fork out $4,700 in ‘moving tax’

It’s not just rising rents Aussies are grappling with — new data shows moving costs are also taking a growing toll.

New research from Money.com.au reveals renters moved home roughly every three years on average and spent about $4,700 on moving costs over the past decade. That’s equivalent to $1,567 per move.

One in five renters (20%) reported spending between $5,000 and $10,000 on moving costs over the same period.

Money.com.au’s Property Expert, Nick Burgess, says the cost of moving is adding another layer of financial pressure for renters.

“Moving costs like removalists, bond payments and overlapping rent creates a serious financial burden for renters. It compounds the pressure from rising weekly rents and tight rental supply in recent years,” he says.

“If you’re a renter who has to move at the end of every lease to avoid a rent hike, or you’re moving interstate or relocating across major cities, moving costs can quickly become prohibitive. I’ve seen cases where a couple spent $7,000 to move from Brisbane to the Gold Coast, and another family spent $5,000 relocating from Geelong to Melbourne for work.”

“If rent money is considered ‘dead money’, then the moving tax can be a silent killer because it’s thousands of dollars renters spend every time they relocate, and over the years those costs really snowball.”

“When you put it in perspective, the average rental moving cost of $4,700 is roughly one-tenth of a 5% deposit on the median combined house and unit price of $883,000. You could argue that’s another barrier to homeownership for some renters.”

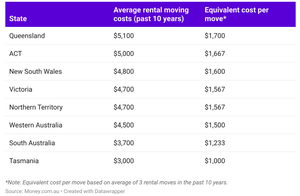

Where it costs the most to move rentals in Australia

Queensland renters paid the most to relocate, averaging $5,100 over the past decade (about $1,700 per move). The ACT followed at $5,000 ($1,667 per move), ahead of New South Wales ($4,800 / $1,600 per move) and Victoria ($4,700 / $1,567 per move), with the Northern Territory on par ($4,700 / $1,567 per move).

Queensland renters paid the most to relocate, averaging $5,100 over the past decade (about $1,700 per move). The ACT followed at $5,000 ($1,667 per move), ahead of New South Wales ($4,800 / $1,600 per move) and Victoria ($4,700 / $1,567 per move), with the Northern Territory on par ($4,700 / $1,567 per move).

Western Australia ($4,500 / $1,500 per move) and South Australia ($3,700 / $1,233 per move) were lower, while Tasmania was the cheapest at $3,000 over the decade (about $1,000 per move).

Removalists and bonds top renters’ financial pain points

Nearly half of renters said removalist fees (45%) and having to pay a new bond before the old one is returned (44%) are the biggest financial pain points when moving.

Other common pressures include paying rent on two properties at once (27%) and end-of-lease cleaning costs (24%), while fewer renters pointed to time off work (9%) and utility reconnection fees (7%) as major stressors.

Millennials hit hardest by moving costs

Millennials paid the highest ‘moving tax’, averaging $5,300 over the past decade — well above Gen X ($4,600), Gen Z ($4,300) and Baby Boomers ($4,200).

-- ENDS --

| State | Average rental moving costs (past 10 years) | Equivalent cost per move* |

|---|---|---|

Queensland | $5,100 | $1,700 |

ACT | $5,000 | $1,667 |

New South Wales | $4,800 | $1,600 |

Victoria | $4,700 | $1,567 |

Northern Territory | $4,700 | $1,567 |

Western Australia | $4,500 | $1,500 |

South Australia | $3,700 | $1,233 |

Tasmania | $3,000 | $1,000 |

49% of borrowers pulled plug on mortgage switch after current lender's last-ditch offer

New research from Money.com.au reveals nearly half of mortgage holders (49%) u-turned on their plans to switch lenders after being offered a lower interest rate by their bank’s retention team.

The nationally representative survey found just 23% of mortgage holders proceeded to switch banks despite receiving a competitive counter-offer from their current lender during their most recent refinance.

Meanwhile, only 28% of Australians said they were not offered a better rate by their lender.

Money.com.au’s Mortgage Expert, Debbie Hays, says lenders often sharpen their pricing when a borrower signals they’re ready to walk.

“Retention teams often have limited pricing authority and a ‘floor rate’ they can offer based on your loan size and loan-to-value ratio. If you stick to your guns, your file can be escalated to a supervisor with discretion to apply a bigger discount,” she says.

“I recently had a borrower who was offered a lower rate and cashback from a new lender. Once their bank chimed in with a retention rate on par, they chose to stay. They’d been with that bank for more than 10 years. In this case, it was in their interest to stay and avoid refinancing costs like discharge and government fees.”

“In most cases, the best you can hope for is your bank matching the competitor’s rate, they rarely beat it. However, big-bank customers may find their lender’s retention rate still sits above what’s available elsewhere in the market or from a second-tier lender.”

Mortgage Broker, Nick Burgess, says some retention rates are genuinely competitive.

“I had a borrower who wanted to refinance out of Bankwest, but the retention team came back with a 0.35% discount on their existing rate. On a $892,000 loan, that saved them about $200 a month. It was a ‘stay’ deal that couldn’t be beaten elsewhere. These are the kinds of retention discounts some banks can offer but will never advertise,” he says.

Broker reveals sneaky retention tactics to watch out for

While retention deals can deliver real savings, there are a few sneaky bank tactics borrowers should watch out for.

- They offer you a fixed-rate alternative Some retention teams won’t match a competitor’s variable rate but will offer you a sharper fixed rate instead. This comes with strings attached like locking you in for another year or more and capping extra repayments. Nick says that from a lender’s perspective, it’s a double win. “They lock you in, so you can’t switch without hefty break costs, and they protect their revenue,” he says.

- Final-stage pricing offer Some lenders don’t come to the table until they see genuine ‘exit signals’. Banks’ retention teams only sharpen their pricing after you lodge a formal discharge request. Nick says some lenders even hold back their most competitive rates until the refinance is already progressing through solicitors or visible in the PEXA online settlement system.

- Internal product switch offers Rather than dangle a lower rate to keep your business, some banks may steer you toward a ‘special internal offer’ or cashback retention deal instead. In some cases, they may suggest switching between package and basic loan products instead.

- The ‘review later’ delay Some lenders may promise to review your rate in a few months rather than offer their sharpest retention rate immediately. In some cases, you may receive a small upfront discount with the promise of further reductions later.

Most borrowers say banks aren’t reviewing their rates

The research found the majority of Australian homeowners (62%) report their lender has never offered them a rate review outside of a refinance, compared with 38% who say they have.

-- ENDS --

7 in 10 Aussies have red flag habits that can hurt their lender ‘character’ check

New Money.com.au research reveals a whopping 70% of Australians have at least one spending habit that could hurt their ‘character’ check with a lender.

Among this group, nearly half (47%) recently spent money on lottery tickets or scratchies, while 30% reported buying alcohol more than twice a week. Nearly one in four Australians spent money on gambling or betting services (23%), or on smoking or vaping products (23%). A smaller share (5%) reported spending on adult content services, including platforms like OnlyFans.

The nationally representative survey of more than 1,000 Australians found just 30% reported none of those spending behaviours.

The five Cs of credit and where ‘character’ fits

Lenders assess every mortgage application based on the five Cs of credit: Collateral (the property securing the loan), Capacity (whether you earn enough to repay it), Capital (the value of your assets), Conditions (any factors that may affect the loan), and Character — how responsibly you manage your money and debts.

While the character assessment is mainly based on your credit history, it also considers spending habits that may flag ‘addictive’ or ‘risky’ behaviour.

Money.com.au’s Mortgage Expert, Debbie Hays, says lenders don’t just look at income and credit scores, they also analyse how borrowers actually spend their money.

“Banks will comb through three months’ worth of bank statements and pay close attention to any spending red flags. They will generally question recurring or excessive purchases, particularly gambling and smoking, but in some rare cases booze too," she says.

“I had a client who had declared living expenses at around $3,500 per month, but his actual living expenses were well over $6,000 per month, with the majority spent at BWS and Smokemart. He was shocked. His actual living expenses blew out his servicing position and his application would have been declined by the selected lender.”

“Lenders scrutinise these behaviours, but they won’t automatically reject an application, unless they see a pattern that could derail your ability to make repayments. Remember that banks must operate under strict responsible lending obligations. If they do reject a loan for failing the character assessment, they will generally tell you that the decision is based on spending patterns and serviceability concerns, not a single transaction.”

The research found that only half of Australians (50%) are aware that lenders assess a borrower’s ‘character’ as part of a home loan application.

How spending habits differ by generation

According to the survey, Gen X are the most likely to have at least one spending habit that could hurt their ‘character’ check with a lender, led by spending on lottery tickets and scratchies (57%), the highest of any age group.

Millennials lead alcohol purchases, with 38% spending on booze more than twice a week, and also top spending on adult subscription services (9%).

Gen Z stands out for higher-risk habits, with 30% reporting gambling or betting activity and an equal share spending on smoking or vaping products (30%).

By contrast, Baby Boomers recorded the lowest rates across all spending categories.

-- ENDS --

46% of homebuyers roll stamp duty and upfront fees into their mortgage, survey finds

For many Australians, it’s not just the deposit that’s hard to save — it’s the stamp duty and buying fees too.

New research from Money.com.au reveals half of Australian homebuyers (46%) increased their mortgage to help fund government charges like stamp duty and other buying fees.

Among this group, 28% increased their home loan to cover all upfront costs, including stamp duty, conveyancing and settlement-related fees, while 18% increased their loan to cover stamp duty only, which is often a five-figure sum.

The remaining 54% of Aussie homebuyers paid all government fees and buying costs separately.

Stamp duty is often the single biggest upfront cost outside the deposit

Money.com.au’s Mortgage Expert, Debbie Hays, says bundling stamp duty and fees into a home loan can help buyers get into the market sooner, but it comes with a long-term trade-off.

“If you’re a first home buyer who doesn’t qualify for an exemption, stamp duty and buying fees can feel like paying a second deposit. Many of those young buyers then roll those taxes and fees into their mortgage and take on a bigger debt than they originally planned,” she says.

“The real sting in the tail is you’ll pay interest on that extra amount over a 30-year term, because stamp duty and fees become part of your loan balance.”

“Sometimes financing those upfront costs is the only way people can buy a home, but buyers should have a plan to reduce the interest, like using an offset account or redraw. When the property grows in value, the equity can put them in a better position to refinance or restructure their loan down the track to pay less interest.”

For investors, Debbie says rolling upfront buying costs into the loan is often viewed differently.

“For investors, rolling stamp duty and upfront costs into the loan is a strategic play. In most cases, the extra interest on the loan is tax-deductible.”

Younger homebuyers most likely to borrow for upfront costs

The survey found that rolling upfront buying costs into a mortgage was most common among younger Australians. Nearly two-thirds of Gen Z homebuyers (64%) borrowed extra to cover costs like stamp duty and other purchasing fees, followed by 54% of Millennials.

“First home buyer exemption thresholds haven’t kept pace with rising house prices, which means many younger buyers miss out on stamp duty relief and end up adding stamp duty and other fees into their loan.”

The share was much lower among older homebuyers, with 39% of Gen X and 27% of Baby Boomers saying they did the same.

-- ENDS --

More than 1 in 3 homeowners plan to lock in fixed rates ahead of more 2026 hikes

New research from Money.com.au reveals more than one in three mortgage holders (35%) plan to lock in a fixed rate in 2026, ahead of more rate hikes.

Among those planning to fix, 23% intend to lock in their rate for two years or longer, while 12% plan to fix for at least one year.

In contrast, most mortgage holders (56%) say they’ll stay on a variable rate and ride out any rate uncertainty, while a smaller share (9%) plan to split their loan between fixed and variable as a hedge.

Money.com.au’s Mortgage Expert, Nick Burgess, says rate uncertainty is pushing mortgage holders towards fixed loans.

“Banks have already been quietly lifting fixed rates, which suggests they’re pricing in multiple rate hikes in 2026. While there are still some fixed rates lingering in the low fives, those sharper deals won’t be around for much longer.”

“Traditionally, borrowers rush to fix when rates are at rock-bottom. But the other moment people tend to lock in is when uncertainty peaks, and right now, a lot of homeowners are choosing certainty over their monthly outgoings above anything else.”

Younger borrowers lead the rush to fix

The research found that Gen Z is the most likely generation to fix their mortgage, with 61% planning to lock in a rate ahead of more 2026 hikes. Millennials followed at 45%, compared with 28% of Gen X borrowers and just 10% of Baby Boomers.

-- ENDS --

2025 published research

Survey: 1 in 5 homeowners underestimate living expenses on their mortgage application

New research from Money.com.au reveals that one in five homeowners (20%) underestimated their living expenses when they applied for a mortgage, and for some it was enough to cost them the loan.

Within this group, 12% said they unintentionally underestimated their expenses but a broker or lender flagged it and the loan still proceeded. A smaller portion (8%) had their home loan application rejected outright as a result of the error.

Some homeowners underestimated their monthly spending by more than $1,000 — a shortfall large enough to push borrowers below the serviceability threshold.

Money.com.au’s Mortgage Expert, Debbie Hays, says many borrowers aren’t keeping close enough track of what they earn and spend, and even small inaccuracies can jeopardise a mortgage application.

“Most people don’t know how much they spend each month. More often than not, mortgage applicants will have an estimate of their living expenses, and when you go through their bank statements, you find glaring inconsistencies. You want to find those errors before you submit your loan application,” she says.

“Lenders will scrutinise every line of your bank statements, so if the figures don’t match what you’ve declared, whether the mistake is accidental or intentional, it can derail your application or even lead to a rejection. This applies just as much to refinancing as it does to new loan applications, because they re-run the same serviceability checks every time.”

The survey found the majority of mortgage holders (69%) estimated their living expenses accurately on their loan application, while 11% admitted they actually overstated their living expenses.

Young Aussies most at risk of loan rejection due to living expenses blunders

Among those who underestimated their living expenses on their mortgage application, younger Australians were by far the most likely to get their figures wrong. Nearly two-thirds of Gen Z borrowers (62%) admitted to underestimating their costs, compared with one-third of Millennials (33%), 19% of Gen X, and just 8% of Baby Boomers.

Younger borrowers paid the highest price for their budget errors: 32% of Gen Z who underestimated their expenses had their home loan rejected, compared with 13% of Millennials.

How do banks assess living expenses on a mortgage application?

Lenders assess living expenses using the Household Expenditure Measure (HEM), which estimates your basic living costs based on income, relationship status and dependents. They compare this benchmark to the expenses you declare on your mortgage application and cross-check it against your bank statements for a period of three months.

If your bank statements show that you spend more than what you declared, lenders will use your actual spending. In some cases your real spending will still sit within the HEM benchmark. However, if it exceeds the HEM, it reduces your borrowing capacity and can even push you below the serviceability threshold, which may lead to the lender rejecting your application.

Debbie says low declared living expenses may be acceptable if:

- You’re self-employed and legitimately run some personal costs through the business

- You have high savings or a high income that clearly supports your lifestyle

- Your property has a strong equity position, which reduces the lender’s risk.

-- ENDS --

Survey: 52% of homeowners will struggle to afford Christmas and their mortgage

New research from Money.com.au reveals that more than half of Australia’s homeowners (52%) will struggle to afford both their mortgage repayments and Christmas spending this year.

Within this group, 37% will cut back on Christmas spending to keep up with their repayments, while 10% expect to rely on credit cards or BNPL services to make ends meet during the silly season. A smaller portion (4%) fear they may fall behind on their mortgage, and 1% say they’ll need to take a repayment holiday or seek hardship support from their lender.

Money.com.au’s Mortgage Expert, Debbie Hays, says many households are entering the festive season with rising costs and mortgage pressures hanging over their heads.

“Christmas is generally a great time for families, but for mortgage holders it’s equally a financial stress test. Even with the RBA cutting rates this year, many homeowners will have to make a trade-off between keeping up with their mortgage and maintaining their usual level of festive spending. Christmas is often difficult to cut back on when kids, family traditions and social pressures are involved,” she says.

“Some mortgage holders will simply scale back their Christmas spending, while others will rely on credit cards or BNPL services, or in some cases seek support from their bank. Lenders can receive more hardship requests during the Christmas season due to increased spending pressures.”

The survey found that only 49% of homeowners can comfortably afford both Christmas and their mortgage repayments this year.

Youngest and oldest homeowners feeling the Christmas mortgage crunch

Borrowers at both ends of the generational ladder are under pressure. Gen Z (61%) and Baby Boomers (57%) are more likely to struggle to afford both Christmas spending and their mortgage. This is followed by 52% of Millennials and 46% of Gen X who report the same.

5 tips on how to juggle your mortgage and Christmas spending

- Prioritise your mortgage repayments Make sure you can cover your mortgage repayments in December and January 2026 before you consider how much to spend at Christmas. Defaulting on your home loan — even once — can trigger fees and damage your credit score, and it may make refinancing much harder down the track.

- Review your home loan rate If it’s been more than a year since your last rate review, it’s worth speaking to a broker. Getting a lower rate on your mortgage could bring your repayments down and free up extra cash flow. Debbie says brokers often have direct relationships with lending teams, which can help them negotiate sharper rates and faster approvals before Christmas on your behalf.

- Be cautious with credit cards and BNPL Using credit cards or BNPL to get through Christmas can create longer-term financial stress. If you do rely on them, set clear repayment limits and avoid stacking multiple BNPL services at once. BNPL services are now treated as credit products, which means any missed payments may affect your credit score.

- Talk to your lender early if you’re struggling Banks have hardship teams that can temporarily adjust your repayments or offer alternative arrangements. Speak to your lender as soon as you think you won’t be able to meet your repayments, even for a short period. The earlier you reach out, the more options you’ll have. This may include deferring your repayments or making reduced payments for a short time. A temporary hardship arrangement will not affect your credit score.